Skip to content

Skip to content You open the mail, find a statement for an account no one mentioned, and your stomach drops. You already filed probate paperwork. You thought the hardest part was behind you. Now you're wondering whether one missed asset can cause legal trouble, family conflict, or both.

That moment is more common than most executors expect. In Texas, finding property after the original inventory doesn't automatically mean you've done something wrong. It does mean you need to respond the right way. The tool for that job is the supplemental inventory.

When people search for supplemental inventory texas probate, they usually want one of three things: a plain-English explanation, a practical filing path, and reassurance that they can fix the problem without making it worse. That's what this guide is built to provide. It speaks to the executor who is grieving, busy, and worried about making a costly mistake.

Introduction to Supplemental Inventory in Texas Probate

A supplemental inventory is a follow-up filing used when assets turn up after the original Inventory, Appraisement, and List of Claims has already been filed in a Texas probate case. Think of the first inventory as your original map of the estate. The supplemental inventory updates that map when you discover a road that wasn't on it.

That can happen for ordinary reasons. A bank sends a late year-end statement. A family member finds a safe deposit box key. An online account surfaces when you sort through a phone or laptop. None of that is unusual. What matters is how quickly and carefully you act once the new information becomes clear.

What a supplemental inventory actually covers

A supplemental inventory is meant to list newly discovered probate assets or claims that were not included in the original filing. It is not the same thing as changing an entry because the court rejected your first inventory. That kind of correction is handled differently.

In plain language:

- Supplemental inventory means you found something new.

- Amended inventory usually means you're correcting something already filed.

- Non-probate property still doesn't belong on the probate inventory just because you found it late.

That last point confuses many executors. Not every asset connected to the deceased belongs in probate. Some assets pass by beneficiary designation, survivorship, or trust ownership. A careful executor separates probate property from non-probate property before filing anything.

Why this filing matters so much

The supplemental inventory protects everyone involved.

It protects heirs and beneficiaries by showing that estate property is being fully disclosed. It protects creditors by keeping the estate record accurate. It also protects you, because a documented correction is far better than silence.

Practical rule: If you discover an asset after filing, don't “wait and see” whether anyone notices. Put the estate record in order promptly.

Executors often worry that filing a supplement will make them look careless. Usually, the opposite is true. Prompt disclosure shows diligence. Hiding the issue, delaying it, or guessing about ownership creates risk.

A simple example

Suppose Maria is appointed executor of her father's estate. She files the original inventory, then later finds an unopened statement from a brokerage account in a desk drawer. The account was solely in her father's name and has no payable-on-death beneficiary. That account likely needs to be added through a supplemental inventory because it appears to be probate property discovered after the original filing.

That kind of clean, timely update helps keep the administration moving instead of letting uncertainty grow.

Statutory Basis and Filing Deadlines

Texas probate law doesn't treat inventories as optional paperwork. The filing duty comes from the Texas Estates Code, and the rules matter because probate courts rely on inventories to supervise administration and protect the people involved.

Under Texas Estates Code § 309.101, personal representatives in Texas probate proceedings must file a Supplemental Inventory when additional assets are discovered after the initial inventory, and the initial inventory must be filed within 90 days of receiving Letters Testamentary or Letters of Administration under § 309.051. Missing that 90-day requirement can lead to personal liability, removal, or damages, as described in this discussion of the Texas probate inventory deadline.

The two statutes that usually matter most

The first statute to know is § 309.051. That's the rule for the initial inventory. It requires the personal representative to file the Inventory, Appraisement, and List of Claims within the deadline after qualification.

The second is § 309.101. That's the rule that comes into play when additional property is discovered after the initial filing.

Read together, they create a practical timeline:

- You qualify as executor or administrator.

- You prepare and file the initial inventory.

- If new estate property is later found, you file a supplemental inventory.

When the clock starts

Executors often calculate from the date of death. That's not the right starting point for the inventory deadline.

The key date is when you qualify and receive your Letters Testamentary or Letters of Administration. That is the event that starts the inventory clock under the statute governing the initial filing.

A good habit is to put three dates on one page as soon as you're appointed:

- Date of qualification

- Date Letters were issued

- Inventory due date

If you're using a paper calendar, circle it. If you're using a phone, set reminders well in advance.

What happens if you're late

Texas probate judges take inventory deadlines seriously because the inventory is a core estate record. When a representative doesn't file on time, the problem isn't just technical. The delay can interfere with debt handling, beneficiary communication, and estate distribution.

Possible consequences can include:

- Removal from the role if the court decides the representative isn't performing required duties

- Personal exposure if the failure causes harm to the estate or interested parties

- Delays in administration that can increase tension among heirs

A deadline in probate is rarely just a filing date. It often affects your credibility with the court.

Extensions and caution

In practice, some courts may consider requests for additional time through counsel. But an executor should never assume an extension will be granted automatically. If valuations, account records, or ownership documents are still missing, that issue should be addressed early and formally.

The safest mindset is simple. Treat the inventory deadline as fixed unless the court gives relief. That's the approach that keeps a difficult estate from becoming a dangerous one.

Understanding When and Why to File Supplemental Inventory

The most stressful part of this process is usually not the form. It's the moment you realize the original inventory may no longer be complete.

A supplemental inventory becomes necessary when you discover additional property or claims that belong to the estate after the first filing. In Texas probate under Estates Code Section 256, independent executors must file a supplemental inventory or supplemental affidavit in lieu of inventory upon discovery of additional property or claims after the initial filing. That update helps maintain complete estate accounting and reduce disputes, as discussed in this overview of Texas probate supplemental inventory requirements.

Common triggers that surprise executors

Many late discoveries are ordinary, not dramatic.

One executor finds a forgotten savings account after forwarding the mail. Another uncovers a refund claim owed to the deceased. Another gains access to a phone and discovers a digital wallet or online financial platform.

Several situations regularly create trouble:

- Forgotten financial accounts connected to old jobs, old addresses, or smaller institutions

- Safe deposit box contents that weren't reviewed before the first inventory

- Digital assets such as online payment accounts, cryptocurrency, or stored value

- Claims owed to the estate like unpaid loans, refunds, or pending receivables

Why prompt filing matters

A supplemental inventory isn't just a legal update. It's a trust-building document.

Beneficiaries often become suspicious when they learn about an asset from a stray letter, a tax form, or a relative instead of from the executor. Filing the supplement promptly shows that you're handling the estate openly and carefully.

A complete estate record can also affect other issues outside probate procedure. For families sorting through long-term care costs and questions about Medicaid estate recovery, understanding exactly what belongs to the estate can be important before assumptions harden into conflict.

A realistic scenario

James is serving as independent executor for his aunt's estate. He files the original inventory based on the house, car, checking account, and household property he knew about. A month later, the aunt's tax preparer sends prior returns showing dividend income from an account no one had mentioned.

James now has a decision to make. He can ignore it and hope it is a non-probate account, or he can investigate ownership, get the date-of-death value, and file the proper supplement if it belongs to the estate.

The second path is almost always the safer one. Delay creates questions that are harder to answer later.

Requirements for Supplemental Inventory Forms

A supplemental inventory form isn't just a note to the court saying, “We found more stuff.” It needs enough detail to identify the property, support the value, and fit into the estate record in a way the court can rely on.

Texas Estates Code Chapter 309 requires the initial probate inventory to be filed within 90 days of qualification and to include a sworn appraisement and list of claims under § 309.051, with Supplemental Inventories under § 309.101 required for assets discovered later, as explained in this guide to Texas supplemental inventory preparation.

Core information the form should include

Even though local practice can vary, a solid supplemental inventory usually includes the same kinds of details that made the original inventory reliable.

Property description

Describe the newly discovered asset clearly enough that a stranger reading the file could understand what it is.

Good examples include:

- Bank name and account type

- Last digits of an account number if appropriate

- Street address for real property in Texas

- Vehicle year, make, and model

- Nature of a claim owed to the estate

“Miscellaneous account” is too vague. “Checking account at a named bank ending in specific digits” is much safer.

Ownership status

Say how the decedent owned the asset, if known. Was it solely owned, jointly owned, or subject to some other arrangement? Ownership affects whether the item belongs in probate at all.

Many executors get stuck with unclear title. If title is unclear, gather the statements, signature cards, deeds, or beneficiary records before filing.

Date-of-death value

The value should reflect fair market value as of the date of death, not today's value. That applies even if the market changed after death.

Supporting documents often include:

- Account statements

- Appraisals

- County tax records used as part of valuation review

- Title records

- Business records for estate claims

The list of claims still matters

People hear “claims” and often think only of debts the estate owes. In inventory practice, claims can also include amounts owed to the estate. If the newly discovered item is a receivable, refund, or similar claim, it should be described with enough detail to show what the estate may collect.

Formalities that are easy to overlook

A supplemental inventory typically needs the same level of care as the original filing.

Use this checklist before signing:

- Accuracy first because the filing is sworn

- Notarization if required by local practice and form

- Consistent labels so the supplement fits the case record cleanly

- Attachments organized in case the court or counsel needs backup

Filing a supplement is often straightforward. Proving why each line belongs there is the part that requires discipline.

If you're unsure whether an item belongs in probate, pause before filing. A wrong supplement can create as much confusion as a missing one.

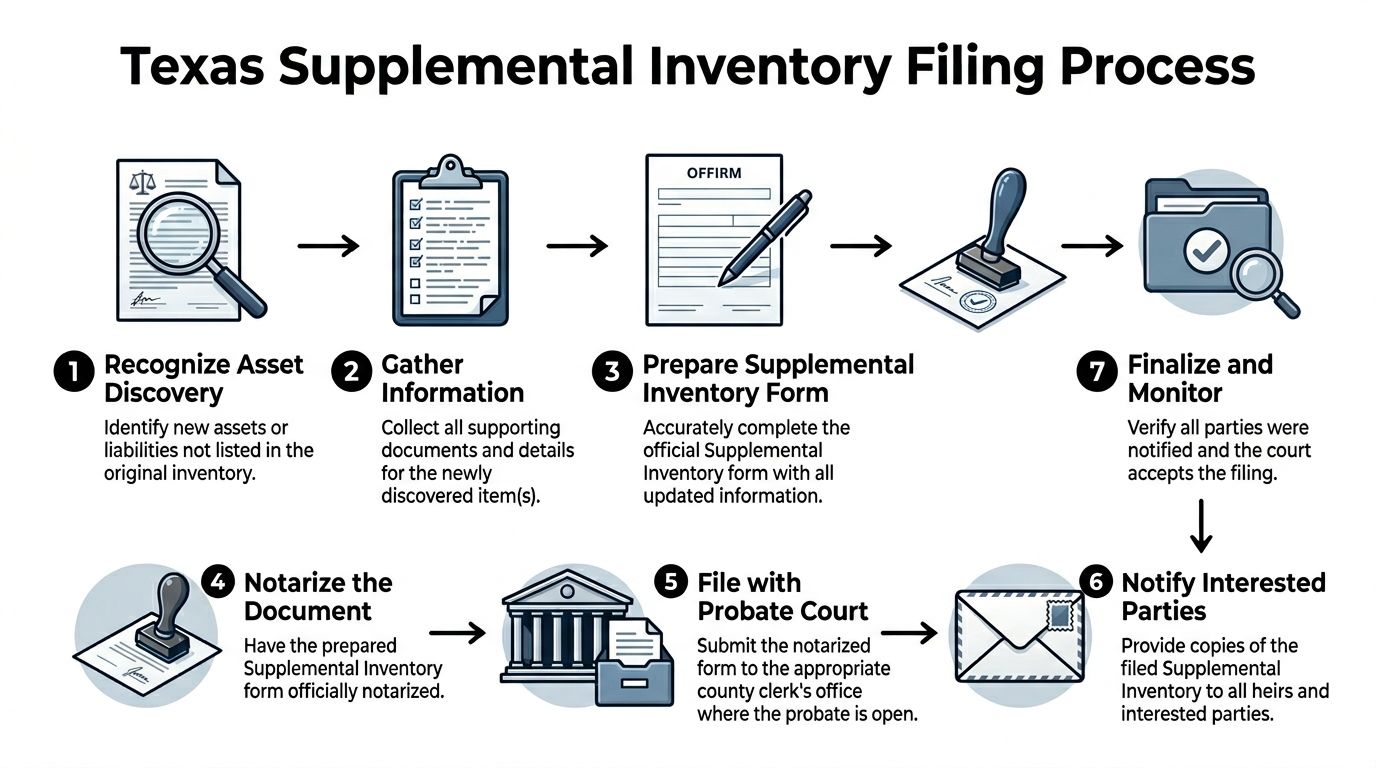

Step-by-Step Filing Process

The filing process is easier when you treat it like a sequence, not a scramble. Executors get into trouble when they jump from discovery straight to filing without confirming ownership, valuation, and court procedure.

The visual below shows the flow in a simple format.

A helpful companion is this resource on the inventory and appraisement filing process in Texas probate, especially if you're comparing the supplement to your original filing duties.

Step one through three

Recognize the discovery

Start by asking one question. Is this new property or a claim that should have been included originally?

If the answer is yes, don't rely on memory or family assumptions. Open a file for that item and gather proof.

Gather records

The best evidence depends on the asset type.

For example:

- A bank account needs statements or bank confirmation

- Texas real estate may require deed records and valuation support

- A receivable may need a contract, invoice, or lawsuit papers

- A digital account may require platform statements and access records

This is also where you sort probate assets from non-probate assets.

Confirm value and ownership

Before anything goes on a sworn filing, confirm two points:

- Did the decedent own it in a way that makes it part of the probate estate?

- What was its fair market value on the date of death?

If either answer is uncertain, stop and clarify it first.

Step four through six

Prepare the supplemental inventory

Use the correct case caption, court, and estate information. Then list the newly discovered property with a clear description and value. If there is a related claim owed to the estate, include that as well.

Keep the wording clean and factual. Don't add guesses, family commentary, or explanations that belong in attorney correspondence rather than the filed form.

Sign and notarize

Because this is a sworn probate filing, review every line before signing. If the local court or form requires notarization, complete that step before filing.

Small errors matter here. A wrong account number, wrong ownership label, or unsupported value can create avoidable objections.

File with the correct probate court

File the supplement in the same county court where the estate is pending. Keep stamped copies or e-filing confirmations in your estate file.

After filing, make note of:

- Filing date

- Method of filing

- Any court response or deficiency notice

- Any parties who must receive notice or copies

Office habit that helps: Keep one running probate log with every filing date, every notice sent, and every document received.

What if you need more time

If records are delayed or an appraisal is still pending, don't disappear. Raise the issue early through counsel and request the appropriate relief if needed. Courts are far more receptive to a representative who acts before the problem becomes a violation.

A simple flow table

| Filing stage | What you do |

|---|---|

| Discovery | Identify the newly found property or claim |

| Review | Confirm probate status and ownership |

| Valuation | Gather date-of-death value support |

| Drafting | Prepare the supplemental inventory form |

| Execution | Sign and notarize if required |

| Filing | Submit to the probate court handling the estate |

| Follow-up | Keep proof of filing and provide required notice |

This process isn't glamorous, but it keeps the estate stable. Maintaining stability is the goal.

Impact on Independent vs Dependent Administration

The same newly discovered asset can lead to a different filing experience depending on whether the estate is under independent administration or dependent administration. That distinction matters because court involvement, privacy, and procedure are not the same.

Texas law requires the initial Inventory, Appraisement, and List of Claims to be filed within 90 days of receiving Letters Testamentary, and supplemental inventories are required when additional assets are found. If they are omitted, courts may impose consequences such as removal or personal liability, and some missed digital assets have delayed estate closure by 6–12 months, as noted in this discussion of itemized probate inventory practice in Texas.

The practical difference

In plain English, independent administration usually gives the executor more room to act without asking the court for permission at every turn. Dependent administration involves more direct court oversight.

If you need background on the broader structure, this overview of independent administration in Texas is useful context.

Independent vs Dependent Administration Comparison

| Aspect | Independent Administration | Dependent Administration |

|---|---|---|

| Court involvement | Less day-to-day supervision | Ongoing court oversight |

| Supplemental filing approach | May involve a supplemental inventory or, in some cases, a supplemental affidavit in lieu if permitted | Usually requires stricter formal filing and review |

| Privacy | More opportunity to reduce public detail in qualifying situations | Less privacy because court filings play a larger role |

| Speed | Often more flexible when records are clear | Can move more slowly because approvals may be required |

| Risk if asset is missed | Still serious, especially if heirs believe information was withheld | Serious, with added concern because the court expects close compliance |

Where executors get tripped up

Many people assume independent administration means “less paperwork.” That's only partly true. It really means less routine court supervision, not fewer legal duties.

Dependent administrations often leave less room for informal fixes. Independent administrations can feel easier, but they still require accurate estate reporting when new property is discovered.

A useful question is not, “Which one is easier?” It's, “Which one demands more formal court involvement if something goes wrong?” In most cases, dependent administration does.

Real-World Examples and Sample Language

Seeing sample wording helps because many executors know what happened but don't know how to say it on paper. A supplemental inventory should be factual, plain, and specific.

The examples below are simplified teaching models. They are not one-size-fits-all forms, but they show the level of detail that usually helps.

Example one with a late-discovered bank account

Sandra is executor for her brother's estate. After filing the original inventory, she receives a statement for a savings account at a bank the family rarely used. The account was only in the decedent's name and had no payable-on-death designation.

A clean entry might read like this:

“After the filing of the original Inventory, Appraisement, and List of Claims, the Personal Representative discovered an additional probate asset not previously included. Savings account at Lone Star Bank, account ending in 4421, titled solely in decedent's name. Fair market value as of decedent's date of death: $8,250.00. Documentation supporting ownership and date-of-death balance is maintained by the estate.”

Why this works:

- It says the asset was discovered after the original filing.

- It identifies the property clearly.

- It states sole ownership.

- It gives a date-of-death value.

- It notes that support exists.

A weaker version would say only “bank account discovered later,” which leaves too much unanswered.

Example two with a digital asset

Digital assets create anxiety because they don't come with a deed or a paper title. But they still need the same disciplined treatment. The executor must confirm access, ownership, and valuation method.

A teaching example could look like this:

“After the original inventory was filed, the Personal Representative identified a digital financial asset associated with the decedent. Digital asset account maintained in decedent's individual name through an online platform, with supporting account records retained by the estate. Fair market value listed is the value as of the decedent's date of death based on the platform's account statement and available valuation records.”

That wording avoids overpromising. It doesn't guess about ownership. It ties the value to records. It also leaves room for supporting documentation.

Sample language for a short introductory paragraph

Some courts or lawyers prefer a brief lead-in before listing the added assets. A practical model is:

- “The following property was not included in the original Inventory, Appraisement, and List of Claims and was discovered after that filing.”

- “The Personal Representative submits this Supplemental Inventory to identify additional probate property and claims belonging to the estate.”

- “All values stated are intended to reflect fair market value as of the decedent's date of death.”

What not to do in your wording

Avoid these common drafting mistakes:

- Don't speculate by writing “believed to be worth” when records can be obtained

- Don't use family shorthand like “Mom's extra account”

- Don't bury ownership issues if title is uncertain

- Don't mix probate and non-probate assets in the same line without clarifying why the asset belongs in the estate

The best probate language is usually the least dramatic. Clear facts beat long explanations.

If you feel tempted to add a paragraph defending why the asset was missed, that's usually a sign you need legal review before filing.

Common Pitfalls Best Practices and Key Takeaways

Most supplemental inventory problems come from three sources. Executors move too fast, assume too much, or wait too long.

The good news is that these mistakes are preventable when you use a repeatable process.

Hidden pitfalls that cause trouble

Guessing about ownership

An account with the decedent's name on a statement doesn't always mean it's a probate asset. Joint ownership, beneficiary designations, and trust ownership can change the answer.

Using the wrong value

The right number is the fair market value at death. Not the balance today. Not what a relative thinks it was worth. Not what the decedent paid years ago.

Forgetting claims owed to the estate

Some executors focus only on property you can touch or see. But the estate may also own a right to collect money, and that may need to be included.

Treating the supplement like a casual correction

This is still a sworn probate filing. Courts and beneficiaries may rely on it. It deserves the same care as the original inventory.

Best practices that make the process smoother

A strong executor usually does the following:

- Creates an asset audit list after the original filing so late-arriving mail, tax forms, and account notices can be reviewed in one place

- Keeps backup documents organized by asset so every line on the supplement can be explained quickly

- Communicates carefully with heirs when a significant asset is discovered, especially if the new property could affect timing or distribution

- Gets help early if title, valuation, or probate status is unclear

Takeaway

Keep these points in front of you if you're handling a supplemental inventory texas probate issue:

- A supplemental inventory adds newly discovered probate assets or claims

- It is different from an amended inventory used to correct a rejected or defective filing

- Ownership comes before filing because not every late-discovered asset belongs in probate

- Date-of-death valuation matters because probate inventories are not based on current value

- Independent and dependent administrations handle the process differently

- Plain, factual language is safer than defensive explanations

- Prompt action protects both the estate and the executor

If you're grieving and trying to manage a loved one's estate, this part of probate can feel personal. That's normal. The law, though, treats it as a recordkeeping duty. When you approach it that way, with calm documentation and timely action, the path usually becomes much clearer.

If you’re facing probate in Texas, our team can help guide you through every step, from filing to final distribution. Law Office of Bryan Fagan, PLLC assists Texas families with probate administration, Texas Probate Process, Guardianship, Wills & Trusts, and Probate Litigation. Schedule your free consultation today.