Skip to content

Skip to content If you've just been named executor after the death of a parent, spouse, or sibling, you're probably holding a mix of paperwork and worry at the same time. One paper says you're in charge. The next question is immediate and uncomfortable. What exactly did your loved one own, and what is it worth?

That question sits at the heart of probate. In Texas, valuing estate assets isn't just paperwork for the court. It's how you create a fair record of what belongs in the estate, what may pass to heirs, and what needs closer review before anything is distributed.

Most families don't walk into probate already knowing how to price a home, a truck, a bank account, jewelry, or a family business. That's normal. The process becomes manageable when you break it into pieces and focus on accuracy, timing, and documentation.

Your First Duty as Executor Understanding Estate Valuation

You may get pulled in three directions on the same day. A brother wants to know when distributions will happen. A bank asks for Letters Testamentary. A relative looks at the family home and announces a number that sounds confident but has nothing behind it.

At that point, valuation becomes one of your first real jobs as executor. The numbers you assign affect court filings, shape whether inheritances are divided fairly, and give you a record you can stand behind if someone later questions your decisions. Getting the value right is not just about math. It is about peace of mind and legal protection.

Why this task matters so early

Texas probate works on accountability. Under the Texas Estates Code, the personal representative is expected to gather estate property, sort out what belongs in the estate, and prepare a record that can be supported with documents. A careful valuation helps you show that you acted reasonably, not casually.

That distinction matters in families under stress.

If your mother owned a home, two bank accounts, a vehicle, and jewelry, each item needs a supportable value. If your father owned mineral interests, a rental house, or part of a business, the risk of disagreement rises because those assets are harder to price and easier for family members to see differently.

Practical rule: A good valuation does two jobs at once. It helps heirs receive a fair share, and it helps the executor show the court and the family that nothing was hidden, overlooked, or priced carelessly.

A simple way to understand this is to compare valuation to making a map before a long trip. If the map is wrong at the start, every later decision gets harder. You may pay the wrong debts, distribute property too soon, or create suspicion where none existed before.

A familiar Texas probate moment

A daughter in Houston is named executor in her father's will. She finds a house, an older pickup, a savings account, and paperwork for a vacant tract in another county. Her brother says the land has little value. Her aunt says the county tax number should be good enough. Neither opinion gives her much protection if an heir objects or the court expects better support.

For property in Texas, it helps to collect deeds, account statements, titles, prior appraisals, tax records, and business documents early. That gives you a starting file for each asset instead of forcing you to reconstruct everything after questions arise.

Families often feel pressure to settle these questions fast. Slow and documented is usually safer than fast and assumed. As executor, your first duty is not to please the loudest relative. It is to create a reliable picture of what the estate owned and what those assets were worth at the right time.

The Two Pillars of Texas Estate Valuation

The most important concepts are simple once you strip away the legal wording. Probate valuation usually turns on market value and date-of-death value.

Market value means real-world value

For Texas real property, Tax Code Section 23.01 uses market value as the foundation for appraisal, meaning the price a property would transfer for cash under prevailing market conditions as of January 1. That same market-based thinking is central to probate inventories because the court wants a realistic value, not a convenient one.

Think of it this way. If a willing buyer and a willing seller met in an ordinary transaction, with neither side being forced, what would the property sell for? That's the number you're trying to reach.

That doesn't always match what a family member hopes the asset is worth. It also may not match a county tax figure.

Why tax values often create confusion

A tax appraisal can be useful background information, but it usually isn't the final answer for probate. Texas probate courts often prefer market-based appraisals instead of tax-assessed values, because tax numbers can lag behind what buyers are paying in the market.

If your uncle's home tax record shows one value, but nearby homes sold for more around the date of death, the estate may need a comparative market analysis or a professional appraisal to support the inventory.

That difference becomes especially important for executors who want to avoid later objections from heirs.

A short video can help if you want another plain-English explanation of probate basics and property issues:

Date-of-death value fixes the timeline

Assets don't get valued based on when the family finally sorts through the garage. They don't get valued based on when the judge signs a later order. The critical point is usually the date of death.

That matters because values move. A stock account may rise or fall. A house may sit on the market for months. A vehicle may lose value. Probate needs a value tied to the proper moment in time.

The cleanest inventories are built around one question for each asset: what was this worth when the owner died?

Common mistakes families make

- Using today's value instead of the correct historical value: This often happens with brokerage accounts and real estate.

- Relying on informal family opinions: A brother's guess about a gun collection or a cousin's opinion about antiques usually won't resolve a dispute.

- Treating sentimental value as legal value: A wedding ring may feel priceless. The inventory still needs a supportable dollar value.

When you understand these two pillars, the probate paperwork starts to make more sense. You're not trying to create a perfect number in the abstract. You're trying to create a fair, defensible number tied to a specific date.

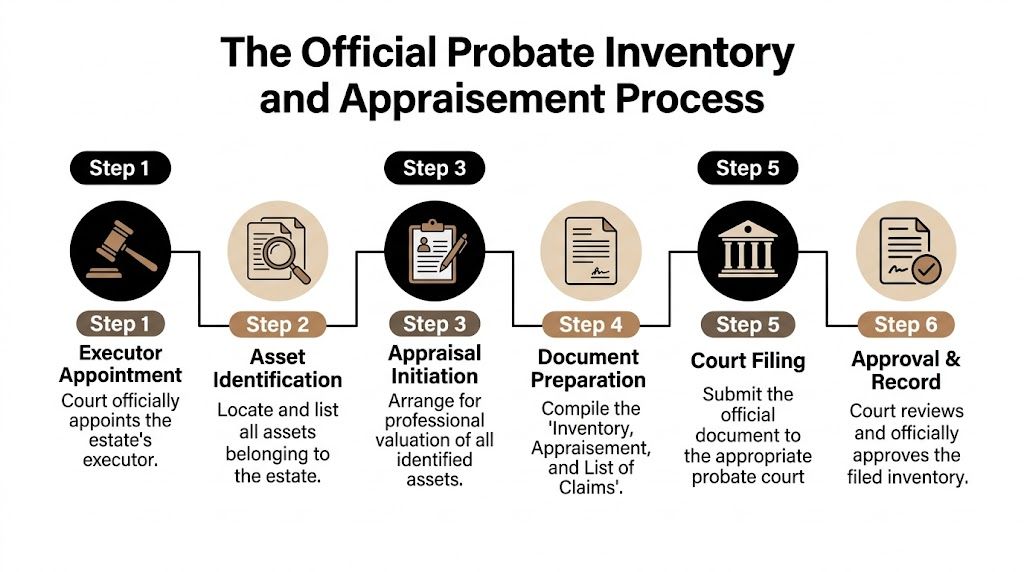

The Official Probate Inventory and Appraisement

Two weeks after the funeral, an executor often finds herself at the dining room table with a stack of mail, a set of car keys, and three family members who each remember the estate a little differently. One says the jewelry was valuable. Another says the house is worth whatever the county says. A third asks whether a small business interest even belongs in probate. The Inventory, Appraisement, and List of Claims is the document that brings order to that moment.

What this document does

This filing is the estate's formal snapshot for the court. It identifies probate assets, assigns supportable values, and lists known claims or debts. For an executor, it also serves another purpose. It shows that you handled the estate carefully, used a consistent process, and did not guess when a better source of value was available.

That matters for peace of mind as much as paperwork.

Under the Texas Estates Code, a full inventory is usually required unless the estate qualifies for an alternative filing. Courts and beneficiaries may look to this document later if questions come up about what existed, what it was worth, or whether something was left out. The Texas Comptroller's property valuation guidance helps explain why tax values and market values are not always the same: https://comptroller.texas.gov/taxes/property-tax/valuing-property.php

A practical six-step approach

A good inventory is built the same way you would build a careful household ledger. Start with proof, match each asset to the correct value date, and write descriptions clear enough that a stranger could identify the property.

Confirm your authority

Act only after the court has appointed you and issued the documents that let you act for the estate.Identify probate assets

Gather deeds, account statements, vehicle titles, business records, insurance papers, and any lists the decedent kept.Separate probate from non-probate property

Some assets pass by beneficiary designation, survivorship, or trust. Those assets may matter to the family, but they may not belong on the probate inventory.Obtain defensible values

Use the right source for the right asset. A bank account usually needs a date-of-death statement. Real estate may call for an appraisal or a well-supported market analysis. A closely held business may need a more specialized review. If you are dealing with business interests, this business property valuation guide gives a helpful overview of the factors professionals often examine.List claims and debts

Include mortgages, credit card balances, and other obligations as required by the administration.File accurately and on time

The court expects enough detail to identify each item without confusion. Vague labels such as "personal items" or "bank account" invite questions that are easy to avoid with better descriptions.

If you want a clearer model for organizing the document, this guide on how to make an itemized inventory for probate in Texas is useful.

What a modest estate might look like

Suppose Maria is executor for her late mother's estate in Fort Bend County. Her mother owned a homestead, one checking account, a sedan, household furniture, a small jewelry collection, and had credit card debt.

Maria's inventory should do more than list broad categories. She would identify the house by legal description and street address, obtain a reliable value tied to the date of death, request the bank's balance for that same date, include the vehicle identification details, and decide whether the jewelry needs a professional appraisal. If one sibling later questions the numbers, Maria can point to records instead of memory.

That is how an inventory protects an executor. It creates a paper trail that shows fairness.

When an affidavit in lieu of inventory may apply

Some independent executors can file an affidavit in lieu of a full inventory if the estate qualifies and eligible debts have been handled. Whether that option is available depends on the facts, the type of administration, and the court's requirements.

Families often assume the shortcut applies whenever the estate seems simple. It may not. Unresolved debts, unusual property, or tension among heirs can make a full inventory the safer course because it leaves less room for later accusations.

Executor warning: If heirs later claim an asset was omitted or undervalued, the inventory often becomes the first document everyone studies. Inaccurate filings can grow into larger conflicts and, in some estates, court challenges over the executor's handling of the estate.

How to Value Different Types of Estate Assets

Not every asset should be valued the same way. A house isn't valued like a savings account, and a family business isn't valued like a pickup truck.

Real estate

For most Texas estates, real estate is the asset that causes the most anxiety. Families often look first at the county appraisal district value, but probate usually calls for a market-based number.

Texas Tax Code §23.23(a) caps annual appraised value increases on residence homesteads at 10%, and for non-homestead properties up to $5.32 million in 2026, the circuit breaker limitation caps increases at 20% annually. Zillow reports a typical Texas home value of $300,957 as of 2026, which shows why executors need to understand the difference between appraisal caps and actual market value when preparing a defensible probate valuation: https://www.zillow.com/home-values/54/tx/

A few practical options exist:

- Certified real estate appraisal: Best for disputed homes, high-value properties, unusual land, or cases likely to draw objections.

- Comparative Market Analysis from a realtor: Often useful for ordinary residential property when done carefully with comparable sales near the date of death.

- Specialized review for ranches, rentals, or rural acreage: These can involve issues beyond a neighborhood sales comparison.

If you're deciding whether a formal appraiser is needed, this discussion of the role of real estate appraisers in Texas probate can help: https://txprobatelawyer.net/the-role-of-real-estate-appraisers-in-texas-probate/

Bank accounts and investments

These are often easier to document if you ask the institution the right question. Don't ask for the current balance. Ask for the date-of-death balance or historical statement.

For brokerage accounts, the estate may need values for each holding as of the date of death. Many institutions can produce a death valuation packet or equivalent statement.

A clear paper trail matters here. When heirs question the numbers, bank records usually answer the dispute quickly.

Vehicles

Cars, trucks, boats, and motorcycles are common estate items. The title tells you ownership. The harder part is value.

For an ordinary vehicle, many executors begin with market guides such as Kelley Blue Book and compare condition, mileage, and trim. If the vehicle is collectible, heavily modified, damaged, or part of a business, an ordinary pricing tool may not be enough.

Household items and personal property

This category includes furniture, clothing, tools, appliances, and décor. Most families worry they'll need an expensive appraisal for every lamp and end table. Usually they don't.

Items with ordinary resale value can often be grouped and valued reasonably. The exceptions are the items that tend to trigger disputes:

- Jewelry

- Artwork

- Antiques

- Coins

- Firearms

- Collectibles

If one item is especially valuable, unusual, or emotionally charged, a professional appraisal is often cheaper than a later family fight.

For personal property, the question isn't whether the item mattered to your loved one. The question is whether the number on the inventory can be defended if someone challenges it.

Closely held businesses

A business interest deserves careful handling. Even a small family company can involve ownership percentages, debts, equipment, goodwill, receivables, and operating agreements.

This isn't the place for rough estimates. A business valuation expert, often working with a CPA and probate attorney, can help determine a supportable value. If you want a plain-language overview of how analysts think about company value, a business property valuation guide can be a useful starting point.

This is also one situation where many executors choose coordinated help from counsel, the company's accountant, and a valuation professional. Probate counsel, including firms such as Law Office of Bryan Fagan, PLLC, can coordinate those moving parts when the estate includes operating businesses or disputed ownership records.

Quick Guide to Valuing Common Estate Assets

| Asset Type | Recommended Valuation Method | Key Consideration |

|---|---|---|

| Real estate | Certified appraisal or realtor CMA | Use a market-based value tied to the correct date |

| Bank accounts | Date-of-death statement from the bank | Confirm ownership and beneficiary status |

| Brokerage accounts | Historical statement showing date-of-death values | Look at each holding, not just the later balance |

| Vehicles | Market guide plus condition review | Collectible or damaged vehicles may need more support |

| Household goods | Reasonable grouped estimate for ordinary items | Single high-value items may need separate appraisal |

| Jewelry or art | Specialist appraisal | These items often trigger family disagreement |

| Business interests | Business valuation expert | Ownership documents and debts matter |

| Land, ranches, or mineral interests | Specialized appraisal | These assets often require niche expertise |

A realistic example

Suppose an executor is valuing an estate with a suburban home, one IRA, a pickup, and a gun safe collection. The home may justify a CMA or formal appraisal. The IRA custodian can provide a date-of-death statement. The pickup may be valued with a recognized pricing guide adjusted for condition. The firearms may need an expert if they're collectible or if family members disagree on value.

That kind of item-by-item method is slower than guessing. It's also much safer.

Navigating Complex Valuations and Common Disputes

The hardest probate cases usually aren't about the obvious assets. They involve the property no one can value quickly and the family history no one wants to revisit.

When an asset doesn't fit the usual box

Mineral interests, royalty streams, intellectual property, collections, and partial business ownership can all create valuation trouble. These assets may have value on paper but no easy public market.

A family may also disagree about whether an item belongs to the estate at all. Was the tractor owned personally or by the company? Did Dad give the gun collection to one child before death? Was that bank account joint, or was someone merely helping with bill pay?

Those questions often become legal questions before they become valuation questions.

Heirs' property creates a different level of difficulty

One of the most overlooked issues in Texas probate is heirs' property. This usually means multiple family members inherited undivided interests in property without a clean transfer plan, often after generations of informal ownership.

In Tarrant and Dallas Counties alone, there are over 10,000 heirs' properties valued at over $2.2 billion, according to the Asset Funders Network report on North Texas heirs' property at https://assetfunders.org/wp-content/uploads/AFN_Impacts_HeirsProperty_Homeowners_NTx_vFinal.pdf.

That matters because tangled title often leads to undervaluation, tax trouble, and disputes about who has authority to sell, occupy, or improve the property.

A common family conflict pattern

A grandmother dies owning a house that passed informally through earlier generations. No one updated the deed properly. One grandson has lived there for years and paid some bills. Other relatives live out of state. One person wants to sell. Another wants to keep it. No one agrees on the home's value because no one agrees on the ownership picture.

In that setting, even a good appraisal doesn't solve everything. The family may first need heirship work, title correction, or partition-related advice.

How to reduce valuation disputes before they start

- Use a neutral appraiser: If tension already exists, a jointly accepted professional can reduce suspicion.

- Share documents early: Heirs often react badly when they think information is being withheld.

- Describe assets carefully: Vague labels such as "miscellaneous items" invite mistrust.

- Address title problems fast: Property with unclear ownership can derail the whole estate.

- Check the estate plan: Some disputes could have been avoided with updated Wills & Trusts, especially where blended families or inherited land are involved.

A valuation dispute rarely starts with math alone. It usually starts when one family member thinks the process wasn't open or fair.

When conflict escalates, it may require formal court involvement. That's where experienced probate litigation counsel can help sort out ownership, valuation method, and fiduciary conduct.

How Valuation Affects Taxes and Inheritance Basis

Most heirs focus first on who gets what. The next question should be what the valuation means for future taxes.

Why basis matters

In simple terms, basis is the tax starting point for an asset. When heirs inherit property, that starting point is often adjusted to the asset's value at death. People often call this a stepped-up basis.

Why does that matter? Because if an heir later sells the asset, taxes on gain may depend heavily on that valuation.

Here's the plain-English version. If your father bought stock years ago for a low amount, but the stock was worth much more when he died, the inherited basis is often tied to the later value rather than the original purchase amount. That can reduce the taxable gain if the heir sells soon after inheriting.

Real estate and later sale decisions

The same concept matters for homes, rental property, and land. If an executor uses a weak or poorly documented valuation, heirs may face confusion later when they try to sell and determine gain.

This is one reason an accurate inventory isn't just a court form. It becomes part of the tax story attached to the inherited asset.

Families dealing with broader planning questions may also want to review estate planning tax considerations here: https://txprobatelawyer.net/estate-planning-tax-implications-guide/

A special issue for out-of-state heirs

If the estate includes a Texas rental home, second home, or other non-homestead property, recent Texas appraisal rules can affect how the property is viewed for tax purposes during administration.

Recent Texas legislation includes the Circuit Breaker Limitation, which caps annual appraisal increases on qualifying non-homestead properties at 20% plus improvements. For out-of-state executors, missing that issue can contribute to inflated valuations and unnecessary tax burdens for heirs, as discussed in this overview of Texas county appraisal districts and the circuit breaker limitation: https://ray-tax.com/blog/spotlight-on-texas-county-appraisal-districts-how-they-determine-property-values/

What families often misunderstand

- Probate value and sale price aren't always identical: The proper probate value is tied to the legally relevant date, not automatically the later closing price.

- Good records help later tax reporting: Your CPA or tax preparer will need reliable estate valuation records.

- A rushed estimate can echo for years: Heirs may rely on these numbers long after the estate closes.

Bottom line: Careful valuation doesn't just help you satisfy the probate court. It helps heirs make cleaner decisions when they keep, refinance, or sell inherited property later.

Key Insight Your Executor's Valuation Checklist

If you're feeling overloaded, reduce the job to a checklist. Executors usually do better when they handle valuation in a fixed order instead of trying to solve every issue at once.

Your working checklist

Locate the will and confirm your authority

The court order and your Letters Testamentary or Letters of Administration define when you can act for the estate.Identify what belongs to the probate estate

Some assets pass outside probate, so separate those from estate property before you start assigning values.Use market value, not family opinion

Sentimental beliefs and quick guesses don't create a defensible inventory.Anchor each value to the correct date

Historical statements, appraisals, and comparable sales should tie back to the legally relevant valuation date.Mark the inventory deadline immediately

Missing deadlines can create avoidable pressure and expose the executor to criticism.Flag assets that need specialists

Real estate, businesses, collectibles, mineral interests, and disputed items often deserve expert help.Keep copies of everything

Save appraisals, statements, photos, emails, and notes showing how each number was reached.Communicate with heirs early and calmly

Silence often creates suspicion. Clear updates reduce conflict.

Where added legal help can matter

Some estates need more than routine probate filing. If the case involves a minor beneficiary, an incapacitated heir, or property management concerns, related areas such as Guardianship may become relevant.

Other families realize, after one difficult estate, that they want to avoid the same strain in the future. That's often the moment to revisit planning tools like updated wills, trusts, beneficiary designations, and cleaner title records.

The checklist isn't about making probate feel mechanical. It's about giving you a stable path through a hard season.

Guiding Your Family Through the Texas Probate Process

Accurate valuation is one of the most important ways an executor honors a loved one and protects the family. It creates a fair record, supports the probate filings, and lowers the chance that confusion turns into conflict.

You don't have to know every appraisal method or Estates Code provision on day one. You do need a careful process, reliable documents, and the willingness to pause when an asset needs closer review. That's how executors protect themselves and the people depending on them.

If you're facing uncertainty about real estate, personal property, a family business, heirs' property, or an inventory deadline, legal guidance can make the process much more manageable.

If you’re facing probate in Texas, our team can help guide you through every step, from filing to final distribution. Schedule your free consultation today with Law Office of Bryan Fagan, PLLC.