If you've just been appointed executor for a parent, spouse, or sibling, you're probably staring at a pile of papers while also trying to process a loss. One envelope has court paperwork. Another has a deed. Someone mentions a bank account. Someone else asks about the car title. Before long, it feels like everyone wants answers you don't have yet.

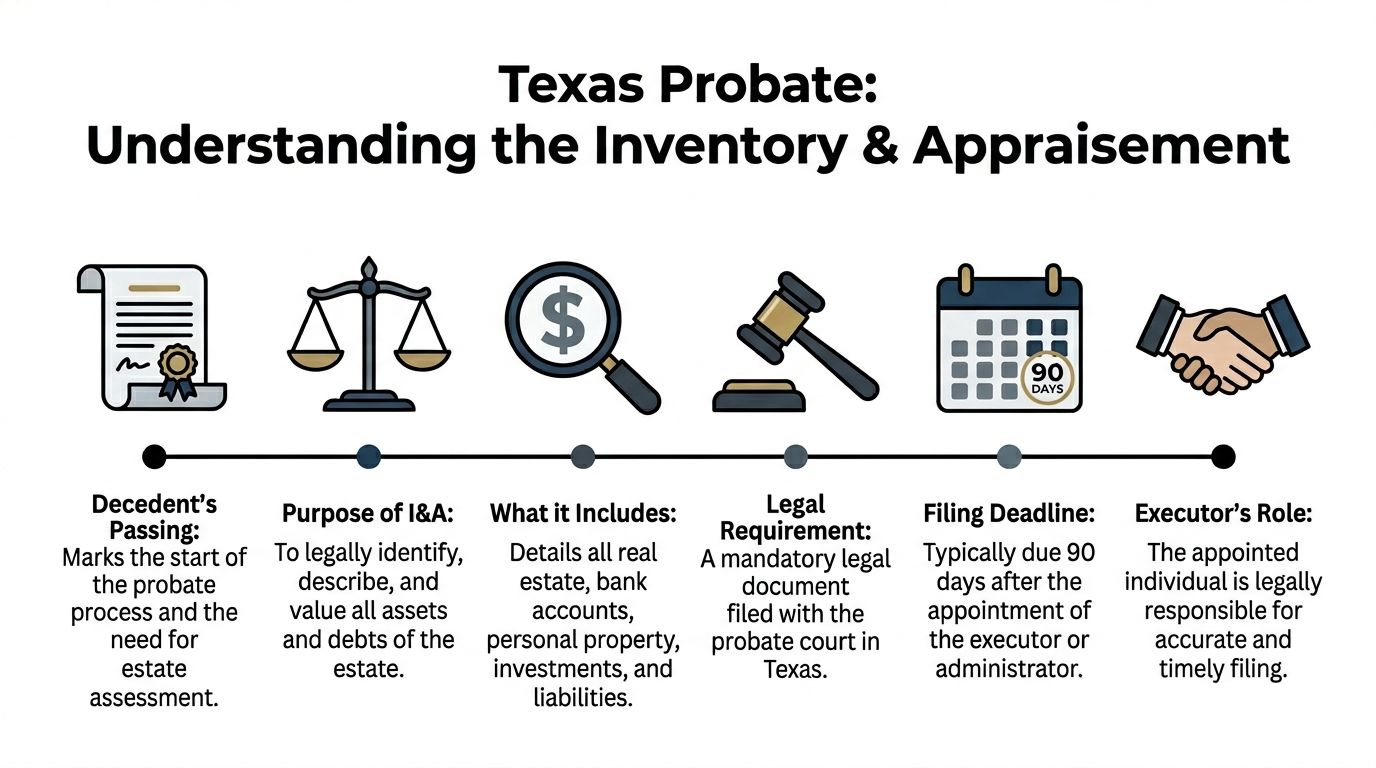

In Texas probate, one document brings that confusion into focus. It's the Inventory, Appraisement, and List of Claims. In plain English, it's the formal record of what the person owned, what those assets were worth at death, and what claims were owed to the estate.

Handled correctly, this isn't just paperwork. It's your map. It helps you organize the estate, answer beneficiary questions with confidence, and reduce the risk that someone later accuses you of hiding assets, undervaluing property, or favoring one heir over another. For many families, the inventory and appraisement filing texas probate process is the moment the estate stops feeling like a mystery and starts becoming manageable.

Your Role as Executor and The First Big Task

Most executors don't step into this role at an easy moment. They step in while arranging a funeral, cleaning out a house, and fielding calls from relatives who all have different memories of what the deceased owned.

A common situation looks like this. A daughter is appointed executor under her mother's will. She has the Letters Testamentary, but she still doesn't know whether the lake house was separate property or community property, whether the brokerage account had a beneficiary designation, or whether her mother's pending claim against a contractor belongs on the probate paperwork. She worries that one mistake could create family conflict.

That's why the first big task matters so much. The inventory gives structure to the job. Instead of trying to solve every probate issue at once, you start by identifying the estate, asset by asset, and valuing it carefully.

The executor's duties go well beyond collecting papers, and it helps to understand that role early. This guide on executor of will responsibilities gives a broader picture of what Texas law expects from the person serving the estate.

The inventory is often the first document that shows whether an executor is approaching the estate with accuracy, transparency, and care.

Families sometimes think conflict starts at distribution. In practice, conflict often starts much earlier, when heirs suspect that no one has a reliable list of what exists. A careful inventory lowers that temperature. It shows that decisions will be based on records, not guesses.

Understanding the Inventory and Appraisement Requirement

The Inventory, Appraisement, and List of Claims is a sworn filing used in Texas probate. It identifies probate assets, assigns a reasonable value to those assets, and lists claims owed to the estate.

That sounds technical, but the basic idea is simple. Texas wants a clear snapshot of the estate so the administration can move forward in an orderly way.

Who has to file it

The legal duty falls on the personal representative, which usually means the executor named in the will or the administrator appointed by the court. Under Texas Estates Code, Chapter 309, the representative must file the inventory within 90 days after receiving letters testamentary or letters of administration, and amendments effective September 1, 2011 created an affidavit-in-lieu option for some independent administrations under specific conditions, as explained in this discussion of the Texas probate inventory deadline and affidavit option.

That deadline gets a lot of executors into trouble because the court appointment can feel like the end of the hardest part. It isn't. In many cases, the administrative work starts once the letters are issued.

What the inventory is supposed to accomplish

The filing serves several practical purposes:

- Creates a baseline: It identifies what belongs in the estate and what doesn't.

- Supports transparency: Beneficiaries can see that assets were identified and valued.

- Guides debt payment: You can't decide how to handle estate obligations until you know what the estate owns.

- Protects the executor: A complete, well-supported filing helps show that you acted in good faith.

The law also requires more than a list of property names. The inventory must identify assets owned at death, include fair market values, distinguish between separate property and community property, and include claims owed to the estate.

What counts as a claim

Many people hear "claims" and think only about debts the estate owes. In this filing, the list of claims includes amounts owed to the estate itself. That can include a lawsuit the deceased had pending, a note receivable, or other money the estate may collect.

That detail matters. Executors sometimes focus only on bank accounts and real estate, then miss intangible claims that still have value.

Why the deadline matters

The court treats this deadline seriously because the inventory is central to administration. If an executor misses it or files something incomplete, the risks are not abstract. The verified data for this topic states that failure to comply can lead to court sanctions, removal of the executor, or personal liability.

A realistic example helps. Suppose a son is appointed executor for his father's estate. He spends weeks cleaning out a workshop and dealing with the homestead, but he doesn't gather statements for investment accounts and never files the inventory on time. A beneficiary starts asking questions. A creditor also appears. What began as a manageable estate now has two avoidable problems: missed deadlines and distrust.

Practical rule: Treat the inventory deadline like a court date, not a paperwork suggestion.

The inventory is not just for the court

Families often assume this filing is only about satisfying a judge. That's too narrow. A strong inventory does something more important. It tells every interested person that the estate will be handled from a documented record.

That is often where probate either settles down or starts to unravel.

If you're serving as executor, it helps to think of the inventory in three layers:

- Legal compliance with Chapter 309.

- Financial organization for the estate.

- Conflict prevention among heirs and creditors.

When those three layers line up, administration usually becomes smoother. When they don't, every later step gets harder.

Assembling the Inventory What to Include and How to Value It

This is the part most executors dread. It helps to break it into categories and work methodically. You are not trying to remember every asset from memory. You are building a documented file.

Start with records, not assumptions

Begin with the documents that usually reveal the estate's financial footprint:

- Mail and email records: Look for statements, tax forms, renewal notices, and account correspondence.

- Prior tax returns: These often reveal interest income, dividends, business activity, or real estate holdings.

- Deeds and titles: These help identify ownership and whether property may be separate or community.

- Bank and brokerage statements: These are key for date-of-death values.

- Lawsuit or contract files: These may reveal claims owed to the estate.

One practical tool is a running asset worksheet. List each asset, where the proof came from, whether it appears to be probate property, and what additional valuation support you still need.

For a more detailed breakdown, this resource on how to make an itemized inventory for probate in Texas is a useful companion.

Value each asset as of the date of death

Under Texas Estates Code § 309.051, each asset must be given a reasonable value as of the date of death, not today's value. That same requirement explains that valuation methods differ by asset class, that professional appraisers often charge varying fees per asset, and that the personal representative can face liability for intentional misrepresentation or gross negligence in valuations, as discussed in this explanation of Texas probate inventory valuation requirements.

That date matters more than many executors realize. If a house rises in value after death, or a brokerage account drops later, the inventory still focuses on the value at death.

Different assets need different proof

Not all property should be valued the same way. That's where many inventories become vulnerable.

Real estate

Texas real estate that belonged to the deceased at death belongs on the inventory. In many estates, real property deserves careful attention because a rough guess can trigger disputes.

A professional appraisal is often the safest route for a home, ranch, mineral-related property, or unusual parcel. If the property is likely to become a point of disagreement, a well-supported appraisal usually costs less than later litigation.

Bank accounts and investment accounts

These are usually more straightforward. Executors often use account statements showing balances on the date of death or as close to that date as possible.

The challenge is completeness. It isn't enough to list the checking account everyone knew about if there was also a savings account, CD, or brokerage account no one mentioned at first.

Vehicles and boats

These still need reasonable valuation support. The process is more defensible when tied to recognized valuation guides rather than a family member's estimate.

Personal property

Household contents can be tricky because sentimental value and fair market value are not the same. A dining table that means a great deal to the family may have a modest resale value. Jewelry, firearms, art, antiques, and collectibles may require more formal appraisal support.

Business interests

Closely held companies are often where inventory disputes become serious. A business interest may need valuation support based on recognized tax and valuation principles. If there is any tension among heirs, this is not the place to improvise.

A short overview can help if you're sorting through valuation choices:

| Asset type | Typical valuation support |

|---|---|

| Real estate | Professional appraisal |

| Bank accounts | Date-of-death statements |

| Brokerage accounts | Date-of-death account records |

| Vehicles and boats | Recognized valuation guides |

| Collectibles and rare items | Specialty appraisal |

| Business interests | Formal business valuation support |

Classification can matter as much as value

Texas executors also have to identify whether property is separate or community. That isn't a technical label with no consequence. It can affect what belongs in the estate and what passes outside the estate.

A common example is a married decedent who owned a house purchased before marriage, later refinanced during marriage, with mortgage payments made from marital income. Families often assume the entire property is either fully separate or fully community. The records may tell a more complicated story.

A defensible inventory doesn't just state a value. It also shows why the asset is in the estate and how its ownership character was determined.

This is one reason deeds, account opening documents, and prior estate planning papers matter so much. Classification errors can cause more conflict than math errors.

Build the file before you finalize the form

A practical way to approach inventory and appraisement filing texas probate is to prepare your support before completing the final sworn document.

That means creating a file for each significant asset with:

- Proof of ownership

- Date-of-death valuation support

- Classification notes

- Questions that still need attorney or appraiser review

Later, when a beneficiary asks why a value was used or why an item was listed as separate property, you have an answer supported by records.

This video gives a useful visual overview of probate administration issues families often face while gathering estate information:

A realistic example

Suppose an executor is handling an estate with a homestead, two vehicles, several bank accounts, a brokerage account, and a small interest in a family business. The executor can probably document the financial accounts quickly. The vehicles may be manageable with recognized guides. The business interest and home, however, may need outside valuation support.

That is where strategic judgment matters. Spending money on professional valuation support for the two assets most likely to trigger disagreement often protects the estate and the executor. Trying to save money by guessing usually works only until someone objects.

Filing Procedures and Strategic Choices in Administration

Once the inventory is assembled, the next question is how to file and whether a full public inventory is the right path for this estate.

Procedure matters. Strategy matters more.

Filing with the probate court

The inventory is filed in the county handling the probate case. In many counties, filing systems allow electronic submission, while some practical steps still vary by local practice and court expectations.

Before filing, confirm:

- The correct court and case number

- Whether the court requires any local form conventions

- That the inventory is sworn and complete

- That supporting records are organized even if they aren't all filed publicly

This is also where executors often discover they need legal guidance not because the form is impossible, but because the estate doesn't fit neatly into a simple checklist.

Independent and dependent administration are not the same

Texas probate procedure changes depending on the type of administration. The filing obligations may overlap, but the level of court supervision is different.

Here is the comparison most families need at this point:

| Requirement | Independent Administration | Dependent Administration |

|---|---|---|

| Court supervision | Lower day-to-day supervision | Ongoing court oversight |

| Inventory decision | May allow strategic use of affidavit in lieu if conditions are met | Full inventory filing is generally the expected path |

| Privacy concerns | More opportunity to avoid a full public inventory in qualifying cases | Less flexibility |

| Best fit | Estates with manageable debt picture and cooperative beneficiaries | Estates with higher conflict, uncertainty, or closer supervision needs |

Independent administration is often chosen because it reduces routine court involvement. If the estate qualifies, that flexibility can make a real difference in how intrusive the process feels for the family.

The affidavit in lieu option

Texas law has allowed an Affidavit in Lieu of Inventory in qualifying independent administrations since September 1, 2011, and the option can improve efficiency and privacy for some estates, but it remains underused and many executors don't understand when it helps, as noted in this discussion of the Affidavit in Lieu of Inventory in Texas probate.

This option can make sense when the estate's debts have been handled in the way the law requires and the beneficiaries have been given the verified inventory information they are entitled to receive. It can reduce the public visibility of a detailed asset list.

That said, it isn't a magic shortcut.

When the affidavit works well

An affidavit in lieu tends to work best when:

- The estate is straightforward: Assets are identifiable and not likely to be disputed.

- Debts are under control: The estate can satisfy the legal conditions for using the affidavit.

- Beneficiaries are cooperative: No one is likely to challenge the representative's handling.

- Privacy matters: The family doesn't want a detailed public filing if it can be avoided.

One example is a modest estate with a house, a few accounts, a car, and family members who already know the asset picture. In that setting, the affidavit may reduce public exposure without undermining trust.

When a full inventory is often the better strategy

Sometimes the full inventory is the stronger choice even if an affidavit may be available.

That is especially true when:

- a blended family creates tension,

- one heir has already questioned ownership,

- an asset's classification is unclear,

- a business interest or unusual property is involved, or

- someone may later accuse the executor of hiding value.

In those situations, a complete filed inventory can function as a shield. It creates a formal record early.

Privacy is valuable, but clarity is often more valuable when the family dynamic is fragile.

A scenario that shows the trade-off

Consider two estates.

In the first, a widow's estate includes ordinary accounts and a residence. Her children are the only beneficiaries, they communicate well, and the debt picture is simple. The affidavit route may fit because it preserves privacy and avoids unnecessary public detail.

In the second, a remarried decedent leaves children from a prior marriage and a surviving spouse. The estate includes a house, investment accounts, and questions about what was separate versus community property. Even if a less public route might seem attractive, a full inventory is often the better decision because everyone needs a formal starting point.

This is the part of probate where legal judgment matters more than speed. Executors often focus on what they are allowed to do. The better question is what choice best protects the estate from later dispute.

For some estates, other probate paths may also be worth discussing, including muniment of title in Texas, when the facts and goals line up. Broader procedural context is also covered in this guide to the Texas Probate Process.

One practical recommendation

If the estate includes hard-to-value property, ownership questions, or strained family communication, don't make the filing decision based only on convenience. A probate lawyer, appraiser, and CPA may each play a different role in helping you decide whether privacy, formality, or stronger documentation should lead.

The Law Office of Bryan Fagan, PLLC is one option families use for guidance on probate administration choices, including whether a full inventory or affidavit in lieu better fits the estate's debt picture, valuation issues, and beneficiary dynamics.

Common Mistakes and How to Avoid Them

Many executors think the main risk is forgetting a signature or using the wrong form. Those mistakes matter, but the larger danger is filing something that creates doubt about your judgment.

Mistake one is treating ownership as obvious

The most common fights don't always start over value. They start over whether an asset belonged to the estate at all, and whether it was separate or community property.

Avoid that by slowing down on deeds, account titles, and acquisition history. If the paper trail is mixed, don't force an answer based on family memory alone.

Mistake two is using the wrong kind of value

Executors often use insurance values, replacement cost, or what a family member believes an item is "worth." That's not the same as fair market value for probate purposes.

Use records tied to the date of death and match the valuation method to the asset. A home may need an appraiser. A bank account usually needs a statement. A collectible may need a specialist.

Mistake three is leaving out inconvenient assets

Sometimes an executor leaves out a claim, a disputed item, or property another family member is already using because listing it feels like it will cause friction. That usually backfires.

If the asset belongs on the inventory, list it and support it. Omissions are far more damaging than uncomfortable conversations.

Mistake four is waiting too long to ask for help

A delayed appraisal, unresolved classification issue, or missing financial record can push the filing into a deadline problem. That is where simple administration problems start turning into Probate Litigation.

Key Insight

Before filing, confirm five things:

- Every probate asset is identified: No account, parcel, claim, or business interest has been ignored.

- Each value matches the correct date: The file supports date-of-death valuation, not current value.

- Property character is addressed: Separate and community classifications are backed by records.

- Supporting documents are organized: You can explain each major number and ownership decision.

- The filing is timely: The court deadline is treated as fixed unless relief has been obtained.

Mistake five is assuming a simple family means a simple estate

Even cooperative families can face later confusion if no one documented why a number was used or how an asset was classified. Good relationships don't replace a good record.

If the estate includes unusual assets, a blended family, prior marriages, or unresolved debt questions, careful review before filing is usually far less expensive than correcting the record later.

After the Inventory What Happens Next

Once the inventory is filed and approved, the estate has a working foundation. That matters because nearly every later task depends on knowing what the estate contains.

The approved inventory helps the executor evaluate creditor issues, decide what estate funds are available, and move toward lawful distribution. It also becomes the baseline reference point if new questions arise about omitted property or competing claims.

For grieving families, this is usually the point where probate starts to feel less abstract. There is now a formal record instead of a loose collection of assumptions.

Filing the inventory doesn't finish the estate, but it often changes the emotional pace of the case. The administration starts moving from uncertainty toward resolution.

From there, the estate may move into debt resolution, tax-related tasks, account transfers, and final distribution under the will or Texas law. Families who are also dealing with broader planning concerns may want to review related topics such as Wills & Trusts and Guardianship.

Frequently Asked Questions on Texas Probate Inventories

What if I discover another asset after filing the inventory?

Don't ignore it. The safer approach is to correct the record promptly through an amended or supplemental filing as appropriate in your case. The goal is an accurate estate record, not pretending the original filing was complete when new information appears.

Does property located outside of Texas go on the inventory?

Texas probate inventories include Texas real estate and all personal property regardless of location if it was owned by the decedent at death. Out-of-state real estate raises different issues and may require additional proceedings in the state where that real estate is located.

Can the beneficiaries object to the inventory I file?

Yes. Beneficiaries can question the inventory, especially if they believe property was omitted, undervalued, or classified incorrectly. Your best protection is accuracy, documentation, and consistent communication. If your file shows how you reached each conclusion, objections are easier to answer.

If you’re facing probate in Texas, our team can help guide you through every step, from filing to final distribution. Schedule your free consultation today with Law Office of Bryan Fagan, PLLC.