Losing a loved one is hard enough. Then the phone starts ringing, bills arrive in the mail, and someone asks whether the estate has to pay a debt you’ve never seen before. If you’re serving as an executor or administrator in Texas, that moment can feel personal and urgent, even when the debt itself may be old, disputed, or legally unenforceable.

That’s where the statute of limitations creditor claims texas estate rules matter. In plain English, these rules set deadlines. Some deadlines limit how long a creditor has to sue on a debt. Others let the estate create a much shorter window by giving proper probate notice. Used correctly, those deadlines help you protect the estate, avoid paying stale claims, and move toward final distribution with confidence.

Texas law doesn’t expect you to guess your way through this. It gives personal representatives a process. If you understand the process and act promptly, you can bring order to a situation that often feels chaotic.

When the Phone Rings Managing Debts After a Loved One's Passing

One of the most difficult parts of probate is how ordinary grief gets interrupted by administrative demands. You may still be planning a service or sorting through family papers when a credit card company calls, a medical bill appears, or a lender wants answers.

Many families assume the safest response is to pay every bill that shows up. That’s understandable. It feels responsible. But in probate, paying too quickly can create new problems, especially if the claim is late, unsupported, or lower in legal priority than other estate obligations.

What these rules are really for

A statute of limitations is a legal deadline. After the deadline passes, a creditor may lose the right to enforce a claim. In the estate setting, those deadlines do more than create a calendar problem for creditors. They give the estate a path to finality.

Think of them as guardrails. They help answer questions like these:

- Is this debt still legally collectible

- Did the creditor get proper notice

- Has the creditor filed the claim on time

- Did the estate respond correctly

- If the claim is rejected, did the creditor sue in time

Those questions matter because the executor or administrator doesn’t owe every person who calls money. The personal representative owes a duty to the estate, the beneficiaries, and the lawful creditor body as a whole.

Texas probate law is designed to sort valid claims from late or unsupported ones, not to pressure grieving families into paying first and asking questions later.

A common real-life situation

A daughter is appointed executor under her father’s will. Two weeks later, a collection company demands payment on an old account. She feels trapped. If she ignores it, she worries she’ll be sued. If she pays it, she worries she may be using estate money improperly.

That tension is exactly why probate procedure matters. Texas law gives the estate tools to identify creditors, send notice, review claims, reject improper claims, and pay valid debts in the right order. Once you understand those tools, the situation usually feels much less overwhelming.

Understanding the Two Clocks for Texas Estate Creditor Claims

To understand the statute of limitations creditor claims texas estate issue, you need to separate two different timelines that affect the same debt.

That distinction matters more than many families expect. A creditor may have had the legal right to collect before death, yet still lose the ability to recover from the estate if the probate process is handled correctly. For a personal representative, that is not a technical detail. It is one of the main tools for protecting estate funds and reaching a final distribution with confidence.

The first clock is the ordinary debt-collection deadline

Before probate enters the picture, every debt has its own legal shelf life. In Texas, many common debts are subject to a four-year limitations period, which often runs from the date the claim accrued. If you want a plain-language overview, this Texas four-year probate limitations guide explains the rule and how it can affect estate administration.

Death can pause that ordinary limitations period for a time under Texas law. Lawyers call that tolling. In simple terms, the countdown stops temporarily after death, which prevents the claim from expiring while no one yet has authority to act for the estate.

That first clock answers one basic question. Was this debt still legally enforceable at all?

The second clock is the probate claims deadline

Once a personal representative is appointed, probate creates a separate set of deadlines that can be even more important in day-to-day administration. Effective strategy is then required.

If you know about an unsecured creditor, proper notice can start a shorter deadline for that creditor to present its claim to the estate. That gives the representative a way to bring uncertainty under control instead of waiting indefinitely for old bills, collection letters, or late-filed demands.

In other words, the estate does not have to sit still and hope creditors go away. The representative can use the notice process to force a decision point.

Practical takeaway: One clock asks whether the debt was still alive under ordinary law. The other asks whether the creditor followed probate procedure in time after the estate took the right steps.

Why these two timelines cause so much confusion

Families often hear a single rule and assume it resolves everything. It rarely does.

A statement like “the debt is within four years” only addresses whether the claim may still exist under general limitations law. It does not answer whether the creditor presented the claim properly in probate. On the other hand, a creditor’s demand letter does not automatically mean the estate must pay. The representative still has to examine whether the debt is valid, timely, supported, and properly asserted.

Here is the cleanest way to separate the two:

| Clock | What it governs | Why it matters |

|---|---|---|

| General limitations clock | Whether the debt remained legally enforceable under ordinary collection law | A debt that already expired before death usually does not become collectible again just because probate was opened |

| Probate claims clock | Whether the creditor acted on time after probate procedures began and notice was given | A creditor with a valid debt can still lose its claim by missing probate deadlines |

A real-world example

Suppose your brother dies owing money on an old unsecured personal loan. The loan is still within the ordinary limitations period, so the creditor starts out with a claim that may be legally enforceable. You are later appointed executor, gather records, identify that lender, and send the required notice.

Now the situation changes.

The creditor can no longer relax and rely only on the longer pre-death collection timeline. Probate has created a second deadline, and the estate has taken a step that may shorten the window to act. If the creditor misses that probate deadline, the estate may have grounds to reject the claim and keep administration on track for the heirs.

That is why a careful personal representative does more than sort mail and pay bills. The job includes reviewing which debts are still enforceable, deciding who should receive notice, documenting delivery, and using the claim and rejection process to close the estate in an orderly way. That playbook helps protect the estate from stale, unsupported, or late claims while preserving funds for the people entitled to inherit.

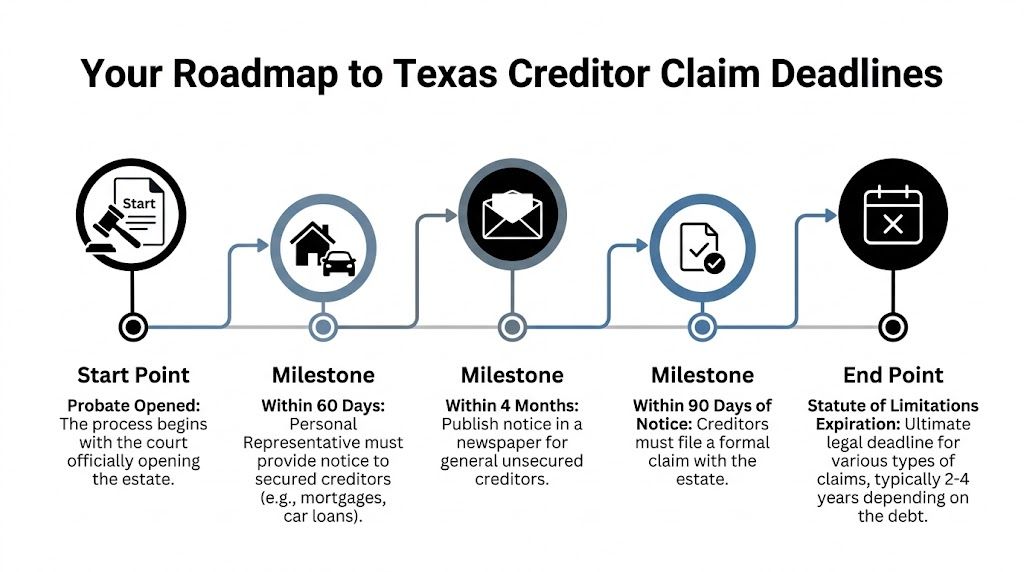

Your Roadmap to Texas Creditor Claim Deadlines

You have been appointed, the mail is piling up, and a hospital bill arrives three days after a credit card statement. Then a lender calls and asks when the estate plans to pay. This is usually the moment an executor realizes probate is not just about gathering assets. It is also about controlling the timeline so old debts do not delay the family’s final distribution.

A helpful way to view this stage is as a set of doors that open and close in order. As personal representative, you do not just wait to see what creditors do. You can use notice rules, claim review, and rejection procedures to press the process toward an orderly ending.

Unsecured creditors and the four-month deadline

Texas gives the estate a practical tool for creating finality with many unsecured debts. As explained in this discussion of Texas creditor rights against estates, a known unsecured creditor who receives the required notice may be barred if it does not act within four months.

Unsecured creditors are usually creditors without collateral. Credit cards, medical bills, signature loans, and many older personal obligations fit here.

For families, the point is simple. Proper notice can shorten the period of uncertainty. If you know a creditor exists and the law requires direct notice, sending it promptly may prevent that claim from lingering over the estate for months longer than necessary.

What happens after a claim is filed

Once a creditor files a claim, the process becomes more structured. The personal representative generally has 30 days to allow or reject the claim. If the claim is rejected, the creditor generally has 90 days to file suit.

That sequence matters because it shifts the pressure.

A claim does not stay in limbo just because it was submitted. You review it, decide whether the estate should accept it, and if you reject it, the creditor must take the next formal step within the required time. Used carefully, that procedure helps protect estate funds for heirs instead of letting unsupported claims drift along unanswered.

Here is the usual order:

- The creditor files a claim

- You review the claim and supporting documents

- You allow or reject it within the required period

- A rejected creditor must sue within the deadline or risk losing the claim

If you want a better sense of how much freedom an executor may have while handling these decisions, this overview of independent administration without court supervision in Texas gives helpful background.

Secured debts follow different rules

A mortgage is not handled like a Visa bill.

Secured creditors have rights tied to specific property, such as a home, car, or equipment. That often changes both the paperwork and the strategy. In practice, the question is not only whether money is owed, but also whether the creditor will look first to the collateral, to estate funds, or to both as Texas probate procedure allows.

That is why careful executors separate debts into categories early. Grouping every bill together can lead to expensive mistakes.

A practical timeline for the personal representative

Many families feel calmer once they can see the process in plain English.

First, gather and sort

- Collect mail, email statements, loan papers, judgments, and tax notices

- Separate debts by type: unsecured, secured, taxes, support obligations, and estate expenses

Next, use notice deliberately

- Identify known creditors who should receive direct notice

- Send notice correctly and keep proof of mailing, delivery, and dates

Then, review what comes in

- Check whether the claim includes enough support, such as contracts, invoices, account statements, or lien documents

- Compare the claim to the applicable probate deadlines

After that, make a decision

- Allow valid claims

- Reject claims that are unsupported, overstated, untimely, or otherwise improper

- Track the lawsuit deadline after rejection

Only then, consider distributions

- Wait until the creditor process is far enough along that heirs are not exposed to avoidable risk

Where executors often get into trouble

Three mistakes cause many of the problems I see.

The first is paying too quickly out of a desire to be fair. That instinct is understandable, especially during grief, but an executor should confirm that the claim was properly presented and should be paid from estate funds before writing a check.

The second is letting a filed claim sit without a response. Silence can cost the estate a useful procedural defense.

The third is distributing property to heirs before the debt process is under control. Once money has gone out, getting it back is rarely easy.

Handled carefully, these deadlines are more than calendar entries. They are part of a playbook. Used at the right time, notice and rejection procedures help close the estate with fewer surprises and a clearer path to final distribution.

Independent vs Dependent Administration and Creditor Claims

The kind of probate administration matters because it changes how much freedom the personal representative has when dealing with debts. In Texas, the two common paths are independent administration and dependent administration.

In both systems, the representative still has to handle claims carefully. But the day-to-day process feels very different.

Independent administration gives more flexibility

In an independent administration, the executor or administrator usually acts with less routine court supervision. That often makes the estate faster to manage. It also means the representative has to be organized and cautious, especially when deciding whether to pay, dispute, or reject a claim.

If you’d like a fuller overview of that structure, this guide to independent administration without court supervision in Texas is a helpful starting point.

A representative in an independent administration often has more room to:

- Review claims directly

- Send notices promptly

- Reject unsupported claims

- Time distributions carefully

That freedom is useful, but it also places more responsibility on the representative to follow the Estates Code correctly.

Dependent administration adds court oversight

In a dependent administration, the court stays much more involved. A representative may need court approval for actions that would be handled more directly in an independent case. That can be protective, especially where family conflict exists or the estate is complicated, but it usually adds delay and expense.

Here’s a brief visual explanation that many families find useful before deciding how these administrations differ in practice.

Side-by-side comparison

| Issue | Independent administration | Dependent administration |

|---|---|---|

| Court involvement | Lower routine involvement | Higher ongoing involvement |

| Handling claims | Representative acts more directly | Court approval may be needed more often |

| Speed | Often more efficient | Often slower |

| Representative burden | More personal responsibility | More court protection |

The best procedure for one estate may be the wrong one for another. A simple estate with a cooperative family can look very different from an estate with disputes, missing records, or creditor pressure.

Why this matters for creditor claims

The deadlines themselves don’t disappear just because a case is handled one way or the other. What changes is how smoothly the representative can act on those deadlines. In an independent administration, a timely and well-documented rejection can be a strong protective move. In a dependent administration, the representative may have more judicial backing but less speed.

For grieving families, the key point is reassurance. If probate feels slow or technical, that doesn’t mean something is wrong. It often reflects the type of administration and the level of oversight the case requires.

Your Step-by-Step Playbook for Managing Estate Debts

A lot of personal representatives have the same unsettling moment. The funeral has barely passed, the mail keeps coming, and then a collector calls asking when the estate will pay. It can feel like you are already behind.

You are not behind. You need a process.

The job is bigger than listing bills. A good personal representative uses notice, review, and rejection procedures to control the timing of claims, protect estate funds, and clear the way for a final distribution that heirs can trust. That is why this section is a playbook, not just a deadline list.

Step one gather the full debt picture

Start by building the estate’s debt file. Collect mail, account statements, loan documents, tax notices, medical bills, and anything showing automatic payments or recurring charges. Check the decedent’s email and bank records if you have legal access to do so, because many accounts are now paperless.

This first step works like sorting papers on a kitchen table before making any decisions. Until you know what is there, it is too early to pay, dispute, or ignore anything.

A practical first-pass system is:

- Secured debts, such as mortgages and car liens

- Priority expenses, such as funeral costs, administration expenses, and family allowance

- General unsecured debts, such as credit cards and personal loans

- Claims needing closer review, where the amount is unclear, the paperwork is missing, or the debt may be old

That last category matters more than many families expect. Some demands sound urgent but arrive with little proof.

Step two use notice as a protective tool

Notice helps set the rules of the game early.

If proper notice goes out, some creditors must act within shorter time periods. That gives the estate a way to bring uncertainty to the surface instead of waiting months or years to see who may appear. For a personal representative, that is one of the best ways to keep the probate process moving toward closure.

Families sometimes worry that sending notice invites more trouble. In practice, it often does the opposite. It draws real claims out into the open and helps fence off claims that are late, unsupported, or never formally presented.

Step three review each claim like an examiner, not a bill payer

When a claim arrives, pause before writing any check.

Ask a series of plain questions:

- Is this creditor correctly identified?

- Is there enough documentation to show the debt is real?

- Was the claim presented in the required way?

- Was it timely?

- Is the amount accurate?

- Is it secured, priority, or unsecured?

- Has any part of it already been paid, settled, or discharged?

The representative’s role is accuracy. Some claims should be paid. Some should be negotiated. Some should be rejected because the proof is weak or the timing is wrong.

Step four allow or reject claims on purpose

This is the point where strategy matters most. If a claim should not be paid, use the formal probate procedure instead of leaving the creditor in limbo. A proper rejection can force the creditor to decide whether it will file suit and prove the claim.

That shift matters. It moves the estate out of a passive role and places the next burden on the creditor.

If you want a closer explanation of the process, this guide on rejecting a creditor claim in Texas probate walks through the mechanics.

Takeaway: The estate does not have to treat every demand for payment as valid. Proof, procedure, and timing all matter.

Step five pay valid claims in the proper order

Even when a debt is real, timing and order still matter. Estate funds are not handled like a regular checking account where whoever asks first gets paid first. Texas probate law sets priorities, and following that order helps protect the representative from personal liability.

As noted earlier, funeral expenses, family protections, administration expenses, secured claims, support obligations, and general unsecured debts are not all treated the same. If the estate does not have enough money to pay everyone, that order can determine who gets paid and who does not.

This is one of the most practical ways the law protects the family. It keeps the loudest creditor from jumping the line.

A realistic scenario

An executor finds four immediate demands. A funeral home invoice has arrived. The probate lawyer needs payment for administration work. A car lender has a lien on the vehicle. A credit card company is calling and pushing for immediate payment.

The executor does not pay based on pressure. The executor collects the paperwork, checks whether the credit card claim was properly presented, and decides whether it should be allowed or formally rejected. At the same time, the executor preserves funds for expenses that carry higher legal priority.

That approach protects the estate from two common mistakes. One is paying the wrong claim too early. The other is draining cash that should have been reserved for obligations the law treats as more important.

A short working checklist

| Task | Why it matters |

|---|---|

| Collect records | You cannot evaluate claims you have not identified |

| Sort each debt by type | Secured, priority, and unsecured claims follow different rules |

| Send proper notice | Notice can shorten the time some creditors have to act |

| Check the proof | Estates should pay supported claims, not assumptions |

| Allow or reject formally | A clear response preserves the estate’s defenses |

| Pay in legal priority order | Correct order protects the representative and helps preserve the inheritance |

Key Insight Protecting Your Family's Inheritance

The most important thing to understand is this. Texas creditor-claim law is not built only for creditors. It is also built to protect estates.

Families often come into probate thinking debt collection is a one-way street. It isn’t. The personal representative has legal tools. Those tools include notice procedures, claim-review procedures, rejection procedures, and payment-priority rules under the Texas Estates Code. When used correctly, they help the estate separate valid claims from stale, unsupported, or lower-priority demands.

What finality really looks like

Finality in probate doesn’t mean every creditor is happy. It means the representative followed the law carefully enough that the estate can close with confidence. Debts were identified. Notice was given where required. Claims were reviewed. Invalid claims were challenged. Valid claims were paid in the proper order. Then distributions to heirs could happen on firmer ground.

This is the core promise behind the statute of limitations creditor claims texas estate framework. It gives the representative a path toward closure.

Families usually feel more at ease once they realize probate is not just about paying debts. It is about controlling the process lawfully and protecting the people the decedent meant to provide for.

The practical lesson

Prompt action matters. So does documentation. Delay can leave old questions open longer than necessary. Careful probate administration can shorten those windows and reduce the chance of unpleasant surprises late in the case.

If you’re serving as an executor, you don’t have to know everything on day one. You do need a method. When you work from a method, this process becomes far more manageable.

Answering Your Pressing Questions on Texas Estate Debts

Am I personally responsible for my loved one’s debts

Usually, no. In most cases, the estate is responsible for valid debts, not the executor personally and not family members just because of the relationship. The main exception is when someone is independently liable for the debt, such as a co-borrower or guarantor. An executor can create risk, though, by mishandling estate funds or paying claims out of order.

Do I have to pay a bill just because a creditor mailed one

No. A mailed bill is not the same thing as a properly allowed claim in probate. The representative should confirm whether the debt is valid, whether it was timely presented, and whether it fits within the estate’s payment priorities. This is one reason probate procedure exists.

What happens if a surprise debt appears late in the estate

Don’t panic. First, check whether the creditor received notice, whether the claim was timely, and whether the debt is enforceable. A late-arriving demand is not automatically collectible. The answer often depends on the creditor’s category, the notice history, and the stage of the administration.

Do mortgages and car loans follow the same rules as credit cards

Not exactly. A mortgage or vehicle loan is usually a secured claim, meaning the debt is tied to collateral. A credit card debt is usually unsecured. That difference matters because secured creditors often have rights tied to the property itself, while unsecured creditors generally depend on the estate-claim process.

What if the estate doesn’t have enough money to pay everyone

Then priority becomes critical. Texas law does not require the representative to pay creditors randomly or equally. The Estates Code sets an order for payment. If the representative follows that order properly, lower-priority creditors may go unpaid without creating personal liability for the representative.

What about funeral expenses and family support

Those are treated with special importance under Texas law. They are not just another bill in the stack. The Estates Code gives them priority, which is one reason executors should avoid paying general unsecured creditors too early.

Can I distribute property to heirs while claims are still unresolved

That can be risky. If you distribute too soon and a valid higher-priority claim remains, the estate may not have funds available to pay it. A careful representative usually waits until the creditor process is far enough along to know what obligations remain.

What if the creditor threatens me on the phone

Stay calm and do not make promises. Ask for the claim in writing and direct communications through the estate process. Collection pressure can feel intimidating, especially after a loss, but threats do not change Texas probate deadlines or payment priorities.

Why do people hire probate counsel for this part

Because small timing mistakes can have large consequences. A missed notice, a late rejection, or a premature payment can affect the whole estate. Having guidance often makes the process smoother, especially when the debts are disputed, the estate may be insolvent, or family members are already under stress.

If you’re facing probate in Texas, the Law Office of Bryan Fagan, PLLC can help guide you through every step, from filing to final distribution. Whether you need help with the Texas Probate Process, Guardianship, Wills & Trusts, or Probate Litigation, our team is here to offer clear answers and compassionate support. Schedule your free consultation today.