When you reach the end of a Texas probate case, the emotional weight often shifts. The shock of the loss may have softened, but the responsibility hasn’t. You’ve likely spent months gathering records, paying bills, protecting property, answering family questions, and trying to honor someone’s wishes while learning a court process you never asked to manage.

Now you’re staring at one last major task: the final accounting.

For many executors, this is the moment that feels strangely harder than the beginning. Early in probate, people expect paperwork. Near the end, they’re tired. They want closure. They worry that one missing receipt, one unexplained transfer, or one unhappy heir could turn the finish line into another round of court hearings.

That concern is understandable. Final accounting approval texas probate matters because it’s the court’s way of confirming that the estate was handled properly before everything is wrapped up. Done well, it protects beneficiaries, clears the path for distribution, and helps protect you as executor.

A simple example helps. Suppose Maria was appointed executor for her father’s estate in Texas. She sold no assets without authority, paid the funeral bill, kept the mortgage current on his home, collected funds from a checking account, and worked carefully with her siblings. Months later, she’s left with a legal question that feels bigger than all the others: how does she prove, in a way the court will accept, that every dollar was handled correctly?

That’s where a clear plan makes all the difference. If you’re still sorting out what property belongs in the estate, this practical guide to understanding property probate can help clarify the asset side of the picture before you finalize the numbers.

Introduction The Final Hurdle in Your Probate Journey

The final accounting is often the last serious hurdle between an open estate and a closed one. It isn’t just another form. It’s the written financial history of the estate from the day you took authority to the day you ask the court to let you finish.

Executors often tell me the same thing at this stage. They don’t mind doing the work. They just want to know they’re doing it right. That’s especially true when grief and family dynamics are both still present, even if everyone is trying to be civil.

You don’t need perfection. You need a complete, honest, well-documented record that the court and the heirs can follow.

Texas probate law gives structure to that process, but the terminology can make ordinary people feel like they’re one step behind. Words like “inventory,” “claims,” “disbursements,” and “discharge” sound technical. In plain English, they mean this: list what came in, list what went out, explain what remains, and show why your plan is proper.

This part of probate feels high-stakes because it is. But it’s manageable when you break it down into pieces and understand what the court wants to see.

What Is a Final Accounting and Why Does It Matter

A final accounting is a full financial report of the estate administration. It shows what property the estate started with, what money came in during administration, what debts and expenses were paid, and what property remains for distribution.

In plain language, it answers the court’s biggest question. What happened to the estate while you were in charge?

The two jobs a final accounting performs

The first job is transparency. Beneficiaries and heirs need a clear picture of how the estate was managed. They’re entitled to understand whether funds were collected, debts were paid correctly, and distributions match the will or Texas law.

The second job is protection. A careful accounting helps protect the executor from later accusations that money disappeared, expenses were improper, or assets were distributed unfairly. If you’ve acted faithfully, the accounting is your proof.

That’s why courts take it seriously. In Travis County, probate auditors conduct statutorily mandated reviews of over 450 annual and final accountings each year in probate and guardianship matters, a reminder that these filings receive real scrutiny, not a rubber stamp, as described by the Travis County Probate Audit Department.

When Texas law requires it

Whether a formal final accounting is required depends in part on the kind of administration.

Here is the practical difference:

| Administration type | What it usually means for accounting |

|---|---|

| Dependent administration | A final accounting is required before the estate can close |

| Independent administration | Court involvement is lighter, but accounting issues can still arise and may be requested or strategically provided |

Under Texas Estates Code § 362.005, dependent administrations require a final accounting before closing. Under Texas Estates Code § 404.001, beneficiaries can demand a full accounting from the personal representative after 15 months from issuance of Letters Testamentary, and later demands may be made at 12-month intervals.

That matters even in an independent administration. Many executors assume “independent” means no one will ever ask questions. That isn’t how real life works. If heirs are uneasy, delayed communication can quickly become a formal demand for records.

What the court expects to see

A proper accounting usually needs to tell a complete financial story, including:

- Starting assets such as bank accounts, real property, vehicles, and other estate property

- Income received during administration, including proceeds or payments that came into the estate

- Expenses paid such as debts, court costs, taxes, funeral expenses, and administration costs

- Remaining property that is still on hand and ready to be distributed

- Supporting documents like statements, receipts, and returns that back up the numbers

Practical rule: If a judge or heir asks, “Where did this money go?” your accounting should answer that question without guesswork.

Why voluntary accounting can be wise

Even if the law doesn’t force an immediate final accounting in every independent administration, offering one can be smart. It creates a record. It lowers suspicion. It gives beneficiaries something concrete to review before positions harden.

That’s especially valuable in families where no one is openly fighting, but everyone is a little tense. Those are the cases that often swing one way or the other based on communication.

A final accounting isn’t just paperwork. It’s the document that turns months of executor work into a clear, reviewable record the court can approve and the family can understand.

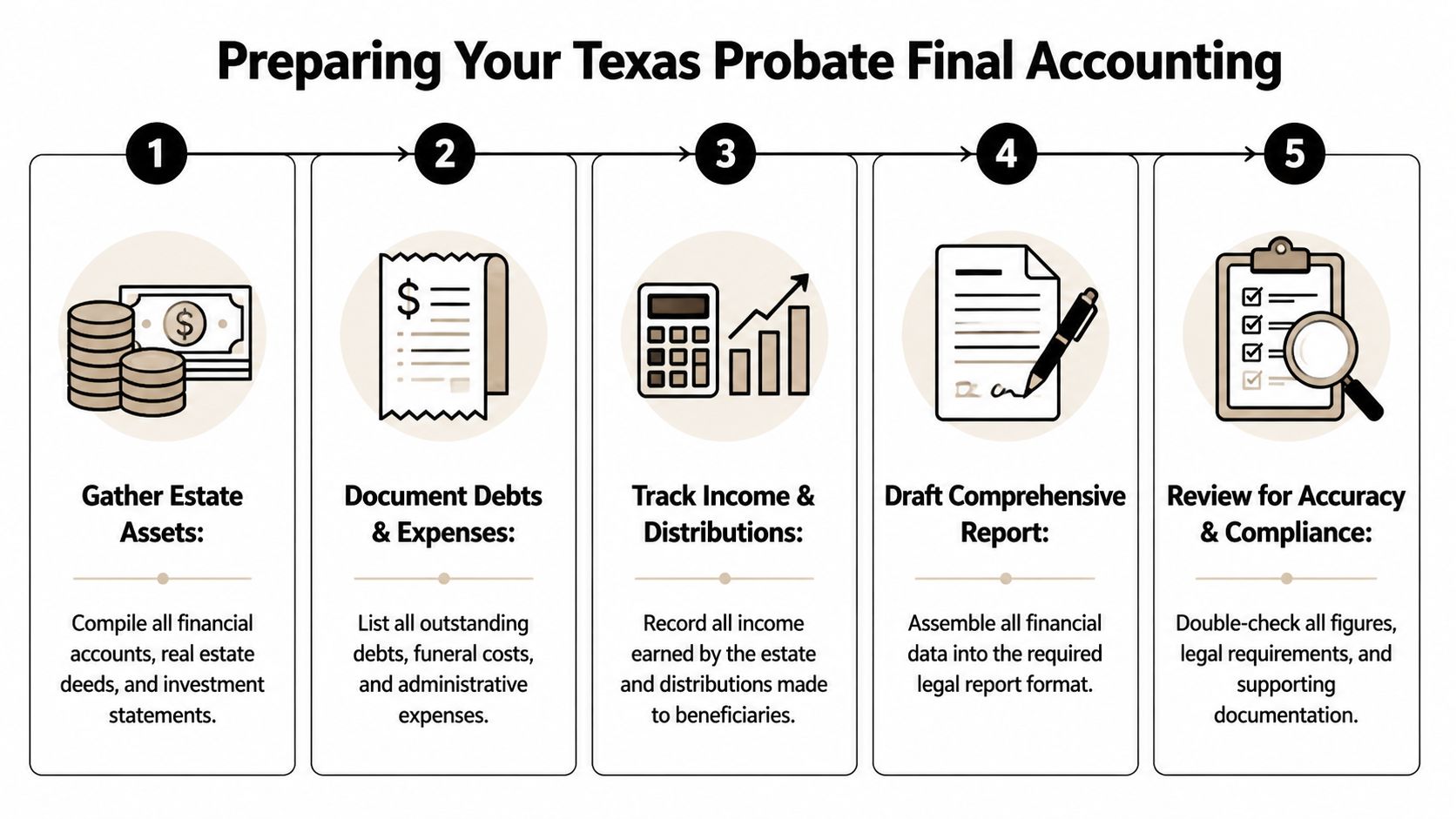

Preparing Your Texas Probate Final Accounting

A final accounting usually goes off course long before it is filed. The pattern is familiar. An executor pays a property tax bill from the estate account, sells a vehicle, reimburses a cousin for mowing the yard, and assumes those details will be easy to reconstruct later. Months pass. Statements are scattered, the memo lines are vague, and a beneficiary starts asking pointed questions.

That is the moment to slow down and build the record the court expects to see.

The safest approach is to prepare your accounting the way a careful auditor or skeptical heir would read it. Your job is not just to total numbers. Your job is to show a clean chain from what the estate started with, to what came in, to what went out, to what remains. If that chain is easy to follow, you lower the chance of objections and reduce your own exposure to claims that funds were mishandled.

Start by reconciling your opening point. For many Texas estates, that means pulling the inventory, appraisement, and list of claims, along with bank statements, deeds, vehicle titles, and any business records. The inventory works like the estate’s opening snapshot. If an asset appeared there, your accounting should explain where it is now. If an asset was missed early, correct the record before filing the final papers rather than hoping no one notices.

That review often reveals the first hidden problem. Executors sometimes mix probate assets with non-probate assets, such as transfer-on-death accounts, survivorship accounts, or life insurance proceeds paid directly to a beneficiary. Including property the estate never controlled can make the accounting inaccurate and invite a challenge that was avoidable from the start.

Next, build a receipts ledger that reads like a timeline. List each item the estate received during administration, the date it arrived, where it came from, and the document that proves it. Rent checks, tax refunds, dividends, sale proceeds, and account transfers should each stand on their own line. Grouping them into one total may save a few minutes now, but it creates confusion later.

For readers who want a closer explanation of the categories Texas courts often expect, this guide on Texas probate accounting requirements is a helpful companion.

A short training resource can also help you visualize the larger probate flow before you compile the final numbers:

Now turn to disbursements. Personal liability concerns usually begin with them. Expenses are often proper, but they need context. A line that says only “reimbursement” or “house expense” is an invitation for someone to ask whether the payment benefited the estate or the executor personally.

Use plain descriptions that answer the question behind every expense: why was this money spent, and who benefited from it?

- Administration costs such as filing fees, publication costs, certified copies, and postage

- Property preservation expenses such as insurance, utilities, lawn care, repairs, and security

- Professional fees such as accounting fees, appraisal fees, or attorney’s fees

- Debt and tax payments that were properly reviewed and paid from estate funds

- Approved reimbursements supported by receipts and a clear estate purpose

A good rule helps here. If you had to explain the payment to the judge in one sentence, could you do it without searching your memory or your inbox?

Specificity matters even more with unusual transactions. If you sold a car to a family member, document the valuation method and the sale terms. If you made a partial distribution before closing the estate, identify the authority for doing so and show how you protected creditors. If you reimbursed yourself, keep receipts and make the estate purpose unmistakable. These are the transactions that often trigger litigation, not because they are always wrong, but because they often look unclear on paper.

A short example shows the difference.

Susan, an independent executor, sells the decedent’s pickup truck and deposits the proceeds into the estate account. Later, she pays for a roof patch to prevent water damage before the house is listed. If her accounting says only “truck sold” and “repair paid,” an heir may suspect she underpriced the truck or overpaid a contractor she knows. If her accounting lists the sale date, bill of sale, deposit amount, repair invoice, and proof that the repair protected estate property, the same transactions are far less likely to become a dispute.

After that, identify what remains on hand for distribution. This part should read like a closing inventory, not a rough estimate. Cash should match the estate account balance. Real property should be described clearly, especially if it will pass in kind rather than be sold. Personal property should be tied to the will, a family settlement, or the applicable intestacy rules.

A simple distribution map often helps more than a dense paragraph:

- Cash on hand. State the amount and who receives it under the will or intestacy rules.

- Real property. State whether it will be distributed, sold, or transferred under another court-approved arrangement.

- Specific personal property. Match each item to the beneficiary named in the will or other legal basis for transfer.

- Residual estate property. Show how the remainder will be divided after expenses and debts are resolved.

Before filing, test the accounting for weak spots that commonly lead to objections. Look for round-number entries with no support, checks written to cash, unexplained transfers between accounts, reimbursements to the executor, and payments made close to the end of administration. None of those items automatically means trouble. Each one deserves extra documentation and a brief explanation.

One final practice can save significant time and stress. Give heirs or beneficiaries a clean, readable draft before positions harden, especially if the estate had sales, reimbursements, or delayed distributions. Early review does not waive your authority as an independent executor. It often prevents suspicion from turning into a formal objection.

A strong final accounting is part math, part storytelling. The numbers must be right, but the sequence has to make sense to a reader who was not there for every decision. If your records let someone follow the estate from opening inventory to final distribution without guessing, you are in a much better position to close the estate efficiently and protect yourself along the way.

Filing With the Court and Notifying Heirs

You have balanced the estate checkbook, gathered the backup, and prepared a final accounting that makes sense on paper. Then closing stalls because the filing packet was incomplete or a required person did not receive notice. That is one of the most frustrating probate delays in Texas, and one of the easiest to prevent with a little planning.

Court approval has two tracks. One track is the math. The other is procedure. An independent executor who handles both carefully is far more likely to get the accounting approved without extra hearings, amended filings, or accusations that something was hidden.

E-filing is part of closing the estate

In many Texas counties, probate filings are submitted electronically. Final accountings often go through the same system, along with the application for approval and any supporting materials the court or auditor expects to see.

Local practice matters here. Some courts want attachments organized a certain way. Some want a proposed order uploaded as a separate document. Some probate auditors are particular about how receipts, disbursements, and distributions are labeled. Checking the local rules before you file can save weeks of delay.

A useful mindset is to treat the filing packet like a closing binder for a business sale. The judge or auditor was not present for each transaction. Your job is to make review easy, not merely technically sufficient.

What usually goes into the filing packet

The exact documents depend on the county and the estate, but executors commonly file:

- The final accounting

- An application or petition asking the court to approve it

- Supporting records, schedules, or auditor-requested attachments

- A proposed order for the judge to sign

- Proof of service or other notice documents

Before you hit submit, do one last liability check. Make sure the names match the court record, the account balances tie out to the ending date in your accounting, and every attachment is readable. A blurred bank statement or an unsigned verification creates avoidable questions.

Notice to heirs deserves the same care as the accounting itself

Notice is not clerical cleanup. It is part of protecting the order you are asking the court to sign.

If an heir or beneficiary should have received notice and did not, the problem is bigger than inconvenience. The court may reset the hearing, require corrected service, or give an unhappy family member an opening to argue that the process was unfair. For an independent executor, that kind of procedural mistake can turn a routine closing into a dispute about conduct.

If you want a plain-English explanation of who may need notice and why, review this guide to notice to beneficiaries in Texas probate.

Here is why careful notice pays off:

- It gives interested parties a fair chance to review what you filed

- It lowers the risk that silence later turns into a claim of secrecy

- It strengthens the final order against later attack

- It helps separate real disputes from simple questions before the hearing

Send notice in a way you can prove later. Keep copies of what was sent, when it was sent, and to whom. If an address was uncertain, document how you confirmed it. Those small records often matter more than executors expect.

What the court is looking for at this stage

Judges and probate auditors are usually asking a practical question: can this estate be closed on a clear and defensible record?

They typically review the filing from four angles:

| Court concern | What they’re checking |

|---|---|

| Accuracy | Do the numbers reconcile with the attached records? |

| Completeness | Does the filing account for what came in, what went out, and what remains for distribution? |

| Authority | Do the transactions appear consistent with the will, court orders, and the executor’s duties? |

| Notice | Did the right people receive proper notice in a provable way? |

That last point is where careful executors can separate themselves from the pack. Many objections begin before anyone files a formal objection. They start when an heir feels surprised, excluded, or unable to follow the paper trail.

A proactive filing strategy that avoids common trouble

Do not file the minute the accounting is almost ready. File when the packet reads clearly, the notice plan is confirmed, and your proof folder is complete.

For estates with family tension, business interests, reimbursements to the executor, or disputed valuations, prepare a short cover summary for heirs when notice goes out. You are not arguing your case. You are reducing the odds that someone misreads a transaction and assumes the worst. In especially tense matters, outside help with organization and communication can be useful. Lighthouse Consultants' dispute resolution services may assist with financial documentation issues that often fuel probate conflict.

One final practical habit helps protect you personally. Save a complete copy of exactly what was filed and exactly what was served. If a question comes up months later, you want the answer in your records, not in your memory.

How to Handle Objections and Minimize Personal Liability

You file the final accounting, then an heir calls and says, “Something here does not look right.” For many executors, that is the moment their stomach drops. In practice, an objection often starts much earlier, with confusion about one transaction, one missing explanation, or one reimbursement that looks suspicious on paper.

Your job is to lower the temperature before that confusion turns into a fiduciary-duty claim.

Start by treating objections as audit points

A final accounting works like a financial map. If one line item is unclear, an heir may assume the whole map is unreliable. That is why experienced independent executors do not wait for a formal filing to test weak spots. They review the accounting the way a skeptical beneficiary would review it.

Ask yourself a few direct questions:

- Would a stranger understand why each payment was made?

- Do reimbursements to the executor have receipts, dates, and a short explanation?

- Do valuations have backup that can be shared quickly if challenged?

- Is there any transaction that could look like self-dealing without context?

- Have family members been given enough information to avoid surprise?

That last question matters more than many guides admit. A large share of probate fights begin with surprise, not fraud.

The best liability strategy is to remove mystery early

Independent executors in Texas often have broad authority, but broad authority does not prevent suspicion. It can increase it if heirs do not understand what happened and why.

A short explanatory summary can do a great deal of work here. If the estate paid for roof repairs before sale, say so. If you reimbursed yourself for filing fees, postage, or property insurance advanced from personal funds, say so. If an asset sold below what an heir expected, attach the appraisal, broker opinion, or other support.

Clear explanation is not a concession. It is evidence that you are acting carefully and in good faith.

For tense estates, especially those involving blended families, closely held businesses, disputed valuations, or executor reimbursements, it also helps to organize records in a way that can be reviewed without argument. Families sometimes benefit from outside support such as Lighthouse Consultants' dispute resolution services to present financial details clearly and reduce confusion.

Know what actually creates personal liability

An heir’s anger does not create personal liability by itself. Personal exposure usually comes from conduct that suggests the executor failed in the duties of loyalty, care, honesty, or impartiality.

Common problem areas include:

- Mixing estate money with personal money

- Paying beneficiaries before debts, taxes, or expenses are resolved

- Keeping poor records, especially for cash transactions or reimbursements

- Giving one beneficiary better information or better treatment than another

- Using estate property for personal convenience or gain without clear authority

- Ignoring reasonable requests for clarification until a dispute hardens

If you want a clearer picture of the conduct that can trigger claims, review this explanation of Texas executor breach of fiduciary duty claims.

A practical rule helps here. If a transaction would require a long verbal explanation, it probably needs better written documentation.

How to respond if an objection is filed

Once an objection is on file, slow down and get organized. Defensive reactions usually create more risk than the objection itself.

Use this order:

- Read the objection line by line. Separate emotional language from the actual complaint.

- Match each disputed item to your records. Pull receipts, bank statements, invoices, appraisals, emails, and prior notices.

- Check whether the problem is clarity or correctness. Some objections are solved by explanation. Others require a correction.

- Fix real mistakes promptly. Courts usually respond better to an executor who corrects an error than one who argues with an obvious problem.

- Avoid side conversations that create new evidence problems. Keep communications measured, accurate, and documented.

- Get legal advice early if the objection hints at self-dealing, removal, surcharge, or unequal treatment.

That sequence protects both the estate and the executor personally. It also helps keep a limited dispute from spreading into a broader accusation about your entire administration.

A common trigger many executors miss

Reimbursements are often where trouble starts.

You may know you paid storage fees, lawn care, insurance, locksmith charges, or emergency repair costs out of your own pocket for the estate’s benefit. An heir who sees only a repayment line item may see something very different. Without receipts and a short explanation, an ordinary reimbursement can look like you paid yourself first.

Treat every reimbursement as if it will be questioned later. Save the receipt, note the purpose, connect it to the estate asset involved, and make sure the amount matches the paper trail exactly.

That habit does more than answer objections. It reduces the chance that a disappointed heir can frame a routine transaction as misconduct.

Stay calm, stay neutral, stay documented

The safest posture is steady and boring. Courts like executors whose records are clean, explanations are consistent, and decisions can be traced from authority to action to documentation.

If you approach objections that way, you improve the odds of resolving the dispute efficiently, protecting the accounting, and reducing the chance that your service as executor turns into a personal lawsuit.

Key Insight After Approval What Comes Next

Key Insight: A well-prepared final accounting does more than satisfy the court. It gives the executor a cleaner exit, gives beneficiaries fewer reasons to question what happened, and helps close the estate without carrying risk into your personal life.

You receive the signed order and feel the weight start to lift. That reaction is understandable. But approval is closer to the last checklist before landing than the moment the plane touches the ground. A few closing steps still matter, and handling them carefully is one of the best ways to prevent late disputes.

Final distribution should match the approved path

After approval, complete distributions exactly as authorized by the court, the will, and Texas law. Precision matters here. Many post-approval conflicts start when an executor gets informal, rounds numbers, transfers property too early, or skips written proof that a beneficiary received what was due.

That usually includes:

- Distributing remaining estate funds to the correct beneficiaries

- Transferring title to estate property that is ready to pass out

- Paying final approved administrative expenses

- Collecting receipts, releases, or written acknowledgments when appropriate

Those last documents are often overlooked. They can be very helpful later if a beneficiary claims a distribution was short, late, or never made.

Discharge is part of protecting yourself

Court approval of the accounting is important, but it is not always the same as being fully discharged from service. Discharge is the court’s formal sign-off that your job is finished once the remaining steps are completed.

For an independent executor, this point deserves real attention. If you close your file mentally before you close it legally, you leave room for avoidable problems. Confirm what the order says, complete every required transfer, and make sure any final receipt, release, or closing document is in place before you treat your role as over.

A simple rule helps here. Do not assume "approved" means "finished." Read the order like a checklist.

Keep your records after the estate closes

Do not toss the file once the last distribution goes out.

Keep copies of the accounting, bank records, receipts, tax documents, correspondence, signed beneficiary acknowledgments, and the court’s closing papers for several years, as noted earlier. If a beneficiary raises a question later, or a tax issue appears, good records let you answer with documents instead of memory.

That is one of the quietest ways to reduce personal liability. A complete file discourages weak claims because the paper trail is already there.

Watch for the post-approval mistakes other guides skip

The period right after approval can trigger trouble if an executor relaxes too soon. Common examples include paying a final expense that was not clearly documented, making unequal distributions to "work things out" within the family, or transferring an asset before confirming there is no remaining issue tied to it.

The safer approach is steady and procedural:

- Review the signed order line by line.

- Match each distribution to the governing document and your accounting.

- Get written proof of what was paid or transferred.

- Keep a closing file that another person could understand without your help.

That approach is not flashy. It works. It shortens the chance for conflict, helps you close the estate with confidence, and reduces the odds that your final act as executor becomes the start of a personal dispute.

Conclusion Your Partner in Texas Probate

A Texas executor often reaches this point with one question still hanging in the air: "Have I finished this the right way?" That concern is normal. Final accounting approval usually means you are near the end, but the safest executors treat the closing stage like a last inspection before handing over the keys.

If you kept a clear paper trail, matched each action to the court’s order and the will, and paused before making informal family accommodations, you did more than complete paperwork. You reduced the chance of objections, protected yourself from avoidable personal liability, and made it easier for the estate to close without one last dispute.

Probate law can still become difficult quickly, especially if an heir starts asking hard questions, an asset does not transfer cleanly, or the accounting reveals a loose end that needs to be fixed before distributions are complete.

If you want help handling those final steps carefully, our team can guide you through the process from probate filing through closing the estate with clear answers and practical next steps. Contact Law Office of Bryan Fagan, PLLC for compassionate guidance and a free consultation.