When a loved one passes away, the last thing you want to do is navigate a maze of financial paperwork. In the simplest terms, non-probate assets are accounts or property that transfer directly to a named beneficiary after death. They completely bypass the often long and very public Texas probate court process.

Think of them like pre-addressed packages. They go straight to the intended recipient without ever needing to be sorted and approved at the courthouse. This guide is for Texas families, executors, and heirs seeking clarity during a difficult time. We’ll explain these assets in plain English and provide the reassurance you need.

Understanding the Foundation of Your Estate

When an estate is settled in Texas, every single thing the deceased person owned gets sorted into one of two buckets: probate or non-probate. Getting this distinction right is the first—and most critical—step for any executor or family member managing final affairs.

Probate assets are things owned solely in the decedent’s name, like their personal bank account or the family home titled only to them. The distribution of these assets is controlled by their will or, if there isn’t one, by state law. Either way, they must go through a formal court process laid out in the Texas Estates Code (specifically Title 2) to legally change hands.

The Direct Path of Non-Probate Assets

Non-probate assets, on the other hand, play by a different set of rules. Their transfer isn’t dictated by the will at all. Instead, legal documents like beneficiary designation forms or the way a property is titled call the shots. These assets essentially have their own built-in set of instructions that are automatically triggered by the owner’s death.

This direct-transfer mechanism is exactly why they’ve become a cornerstone of modern estate planning. In fact, many estates today are intentionally structured so that a huge portion of wealth passes this way. It’s estimated that up to 60% or more of an individual’s estate in the United States may be held in non-probate forms like retirement accounts and jointly owned property.

To help you see the difference clearly, here’s a quick breakdown.

Probate vs. Non-Probate Assets at a Glance

| Characteristic | Probate Assets | Non-Probate Assets |

|---|---|---|

| Controlled By | The Will (or Texas Intestacy Law) | Beneficiary Designation or Account Titling |

| Transfer Process | Requires court approval through probate | Transfers automatically upon death |

| Public Record | Yes, probate is a public court proceeding | No, transfers are private |

| Speed of Transfer | Can take months or even years | Often takes just days or weeks |

| Common Examples | Solely-owned bank accounts, real estate | Life insurance, 401(k)s, Joint Accounts, Trusts |

This table shows just how different these two paths can be. The route an asset takes has major implications for how quickly heirs get access to it and how much privacy the family has.

The single most important thing to remember is this: a will does not control non-probate assets. A beneficiary designation on a life insurance policy or a 401(k) will almost always override whatever is written in a will. This is a common point of confusion that can cause a world of hurt and unintended consequences if it’s not managed carefully.

This separation of assets is fundamental. For families in the midst of grieving, knowing that funds from a life insurance policy or a retirement account can be accessed quickly—without waiting for a judge’s permission—can provide crucial financial stability during an incredibly difficult time. You can learn more about these distinctions in our guide to probate and non-probate assets. Having this understanding gives you clarity and reassurance as you start the process of organizing a loved one’s estate.

Common Examples of Non Probate Assets

Knowing what a non-probate asset is in theory is one thing. Spotting one in a real-world financial portfolio is another. Thankfully, these tools are quite common in Texas, and each one uses a specific legal mechanism to send assets directly to a beneficiary—completely sidestepping the probate court.

Let’s walk through some of the most frequent examples you’ll come across.

Bank and Brokerage Accounts

Many financial accounts can be set up to avoid probate with simple but powerful instructions. Think of these designations as a direct order given to your bank or brokerage firm, telling them exactly what to do when you pass away.

- Payable-on-Death (POD) Bank Accounts: A POD designation is an instruction you give your bank. It names a specific person who can claim the money in your checking or savings account just by showing up with a death certificate. The funds never enter the probate estate.

- Transfer-on-Death (TOD) Brokerage Accounts: This works just like a POD account but for your investments—stocks, bonds, and mutual funds. A TOD registration allows your chosen beneficiary to take ownership of the securities without any court involvement.

These tools are incredibly straightforward. During your lifetime, the beneficiary has absolutely no access to or control over the money. But upon your death, they inherit the account directly, privately, and quickly.

Life Insurance and Retirement Funds

These are probably the most well-known types of non-probate assets. At their core, they are contracts designed from the very beginning to pay a specific person when the account holder dies.

- Life Insurance Policies: The death benefit from a life insurance policy is paid straight to the beneficiary you named in the policy. This money is not controlled by your will and is completely separate from your probate estate.

- Retirement Accounts (401(k)s, IRAs, 403(b)s): Just like life insurance, the funds stashed in these accounts go directly to the designated beneficiary. This is one area where keeping your beneficiary forms updated is absolutely critical, as these designations will always override whatever your will says.

For many families, these assets provide a vital financial lifeline in the days and weeks after a loss. If you’re curious about the details, you can learn more about how IRAs and 401(k)s go through probate in Texas in our in-depth guide.

Realistic Scenario: Maria named her son, Alex, as the beneficiary of her $250,000 life insurance policy years ago. In her more recent will, she stated that all her assets should be split equally between Alex and her daughter, Sofia. When Maria passed away, Alex contacted the insurance company, provided the death certificate and claim forms, and received the entire $250,000 check within a few weeks. Maria’s will, which was just starting the long probate process, had no say over this money. This gave Alex the funds he needed to handle funeral expenses, but it also unintentionally left Sofia out of a significant asset, highlighting the importance of aligning all documents.

Real Estate and Titled Property

How a piece of property is titled is one of the most powerful factors determining whether it ends up in probate. Texas law offers a few specific ways to own real estate that create an automatic transfer of ownership at death.

One of the most popular methods is Joint Tenancy with Right of Survivorship (JTWROS). When two or more people own property this way, and one owner dies, their share automatically passes to the surviving owner(s). The property deed itself contains the legal instructions for the transfer, making probate completely unnecessary for that asset.

Assets Held in a Living Trust

A Living Trust is a legal tool you create to hold your assets. You transfer ownership of your property—your house, bank accounts, investments—into the name of the trust while you’re still alive. You typically name yourself as the trustee, so you keep full control.

When you pass away, a “successor trustee” you’ve already named steps in to manage and distribute the assets exactly as you instructed in the trust document. Because the trust owns the assets, not you personally, they aren’t part of your probate estate. This process of selling a house held in a trust after death is a great example of how the successor trustee handles things outside of court. This strategy offers a huge degree of control and privacy, which is why it’s a cornerstone of so many Texas estate plans. Our firm can help you explore Wills & Trusts to see if this is the right fit for your family.

The Strategic Benefits of Non Probate Assets

Knowing what non probate assets are is one thing. Understanding why they’re such powerful tools in a Texas estate plan is where the real value lies. For families trying to navigate the emotional and financial turmoil after a loss, these assets can be a profound source of relief and stability.

The biggest advantage is simple: speed. The formal probate process can drag on for months, sometimes even years. Non probate assets, on the other hand, often land in the hands of beneficiaries within weeks. For a grieving spouse or child who needs immediate cash for funeral costs or just to pay the bills, that quick transfer isn’t just a convenience—it’s a lifeline.

Maintaining Privacy and Reducing Costs

Another huge benefit is privacy. Probate is a public court proceeding, which means your will, a detailed list of your assets, and the names of your heirs become public record. Anyone can look it up. Non probate transfers, however, happen quietly between the financial institution and the beneficiary, shielding your family’s financial affairs from prying eyes.

This direct handoff also helps slash the costs of administering an estate. By shrinking the size of the probate estate, you can often lower court fees and legal expenses, leaving more of your legacy for the people you intended it for. This efficiency is a big reason why the US Trusts and Estates industry has ballooned to around $290.1 billion. Families are increasingly turning to tools like trusts to manage these assets, trying to dodge probate delays and keep things private.

The Critical Importance of Regular Reviews

While the upsides are clear, non probate assets aren’t without their risks. Their greatest strength—that direct transfer that bypasses the will—can also be their biggest downfall if you’re not careful. The instructions on a beneficiary designation form are legally binding and will almost always trump whatever your will says.

This creates a serious risk if your designations get stale.

A Cautionary Example: John named his wife as the beneficiary of his 401(k) when they got married. Years later, after a bitter divorce, he updated his will to leave everything to his kids. But he forgot one crucial step: changing his 401(k) beneficiary. When he died, his entire retirement account legally went to his ex-wife, no matter what his will said. That single oversight unintentionally disinherited his children from a massive asset.

This kind of story happens far more often than people think. It’s a painful lesson that highlights the absolute necessity of reviewing your accounts regularly. A solid estate plan isn’t just about the will; it’s about making sure every single beneficiary designation lines up perfectly with your current wishes.

Striking the Right Balance

Non probate assets give you a powerful way to provide for your loved ones efficiently and privately. They are a cornerstone of modern estate planning, allowing for a smooth and immediate transfer of wealth during an incredibly difficult time. But their effectiveness hinges entirely on diligent management.

By understanding both their strategic benefits and their potential dangers, you can make smarter decisions. Tools like a Revocable Living Trust offer a fantastic way to consolidate assets, keep control, and make sure they get distributed exactly as you wish, all outside of probate. Learning about the benefits of a revocable living trust can offer deeper insight into building a secure and private estate plan. Ultimately, a balanced approach is what ensures these tools work for you, not against you.

A Practical Guide for Claiming These Assets

When you’re responsible for settling a loved one’s affairs, the list of tasks can feel endless and overwhelming. The good news? Claiming non-probate assets is often far more straightforward than navigating the main estate through court. This guide breaks down the process into clear, manageable steps—a practical roadmap for a difficult time.

Let’s follow a step-by-step process that an executor or heir would take in Texas.

Step 1: Locate the Key Documents

Before you can take any action, you need to find the right paperwork. This is the foundation for the entire process. Carefully go through your loved one’s files, desk, and safe deposit box, looking for specific documents that point to non-probate assets.

Your search should focus on finding:

- Account Statements: Recent statements for bank accounts, investment portfolios, and retirement accounts (like 401(k)s or IRAs).

- Insurance Policies: The original life insurance policy is ideal, but even a recent premium notice can provide the policy number and company contact information.

- Property Deeds: If they owned real estate jointly, the deed will specify if it includes a “right of survivorship.”

- Trust Documents: If they had a living trust, you’ll need the trust agreement itself.

Gather everything you can find, creating a separate file for each potential non-probate asset. This initial organization will save a tremendous amount of stress later.

Step 2: Identify and Separate the Assets

With the documents in hand, your next job is to sort them into two piles: probate and non-probate. Look for key phrases on the statements and policies. Do you see your name listed as the “Payable-on-Death (POD) Beneficiary” on a savings account or the “Transfer-on-Death (TOD) Beneficiary” on a brokerage account? Does a life insurance policy clearly name you as the sole beneficiary?

These are all non-probate assets. They belong to you directly, by contract, and will not be part of the court-supervised probate process the will must go through. A solely-owned checking account and car, however, are probate assets and will be handled according to the will. Making this distinction early is crucial for understanding which rules apply to which asset.

Step 3: Contact the Financial Institutions

Now it’s time to make some phone calls. This step can feel intimidating, but a little preparation goes a long way. When you call the bank, brokerage firm, or insurance company, have the account or policy number and your loved one’s Social Security number ready.

You can say something simple and clear:

“Hello, my name is [Your Name], and I’m calling about my mother, [Mother’s Name]. She passed away recently, and I am the named beneficiary on her account, number [Account Number]. I need to start the process of filing a claim.”

The representative will guide you from there. They will explain exactly what forms you need and where to send them. It’s a good idea to take notes during these calls, writing down the representative’s name and any reference numbers they provide.

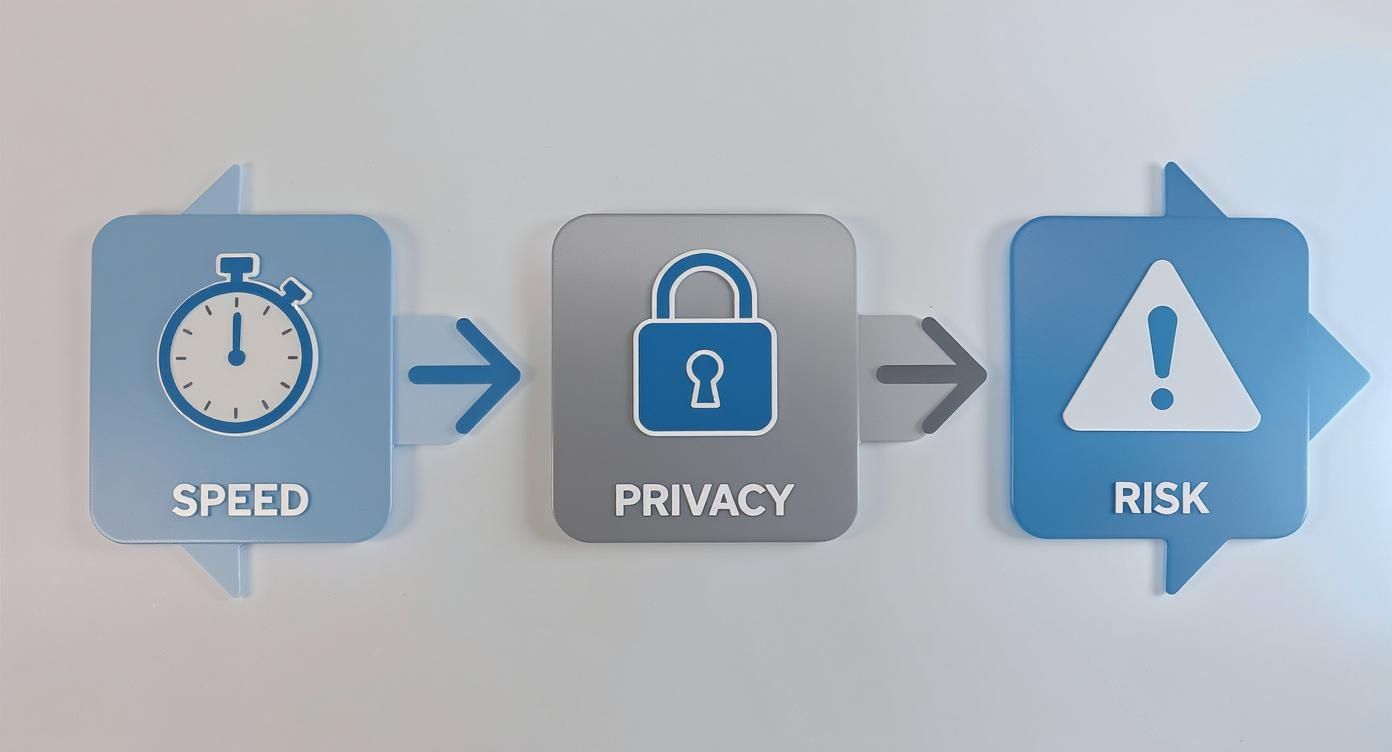

This visual shows the trade-offs often considered when planning with non-probate assets, balancing the need for speed and privacy against potential risks if not managed correctly.

The infographic highlights that while these assets offer a faster and more private transfer, they carry the risk of becoming outdated if beneficiary designations aren’t regularly reviewed.

Step 4: Gather and Submit the Required Paperwork

Each institution will require a specific set of documents to release the funds. You will need to gather these items, which almost always include:

- A Certified Death Certificate: You will need multiple official copies. It’s wise to order 10-15 copies from the funeral home or the Texas Bureau of Vital Statistics, as each institution will require its own original certified copy.

- A Completed Claim Form: The bank or insurance company will provide this. Fill it out carefully and double-check it for accuracy.

- Proof of Identity: A copy of your driver’s license or other government-issued ID is usually required to prove you are the named beneficiary.

Make copies of everything before sending the originals via certified mail. This provides a tracking number and confirmation of delivery, giving you peace of mind that your sensitive documents have arrived safely.

Step 5: Coordinate with the Probate Process

Even though non-probate assets are separate, it’s important to keep them in mind as the executor of the will. While these funds belong directly to the beneficiaries, they can sometimes be relevant to the larger estate, especially if there are significant debts or tax implications.

For a deeper understanding of the executor’s full duties, you can review the complete Texas Probate Process.

This means keeping clear records of the assets received outside of probate. This transparency ensures you are fulfilling all your duties as executor correctly while also claiming the assets that are rightfully yours as a beneficiary. By following these steps methodically, you transform a daunting task into a series of achievable actions.

Key Takeaway

The most critical takeaway is that non-probate assets operate independently of a will. Beneficiary designations on accounts like life insurance, 401(k)s, and POD/TOD bank accounts are legally binding contracts. For families, this means faster access to funds and enhanced privacy. However, it also means that failing to keep these designations updated after major life events (like divorce or marriage) can lead to assets going to unintended people, overriding the wishes stated in a will. Regular reviews of all beneficiary forms are essential for a sound estate plan.

How Non-Probate Assets Affect Debts and Taxes

There’s a common—and dangerous—misconception that non-probate assets live in a protected bubble, completely shielded from the outside world. While it’s true they get to skip the courtroom drama of probate, they aren’t always untouchable when it comes to the estate’s financial obligations.

It’s a difficult truth, but an important one: just because an asset transfers directly to you doesn’t mean it’s automatically free and clear. Understanding how debts and taxes can still reach these assets is critical for both executors and beneficiaries.

The Reach of Creditors in Texas

In Texas, the probate estate is the first line of defense for paying a decedent’s debts. But what happens when the probate assets—like a checking account owned solely by the deceased—run dry before all the final medical bills, credit card balances, and other liabilities are paid off?

This is where things can get complicated. Under specific circumstances outlined in the Texas Estates Code, Title 3, creditors may have the right to pursue certain non-probate assets to satisfy their claims. This is especially true for funds held in multi-party accounts, like joint or POD accounts. The law is designed to prevent people from using these designations simply as a way to dodge their legitimate debts.

Key Insight: If you’re a beneficiary, don’t rush to spend inherited funds from a non-probate asset, especially if you know the estate has significant debts. It’s smart to wait until the executor has a clear picture of the estate’s total assets and liabilities. Acting too soon could mean you’ll have to pay that money back.

This doesn’t give creditors a free-for-all on every non-probate asset. Things like life insurance proceeds, for example, often have very strong protections. But the possibility exists, which makes it essential to work with an attorney to figure out which assets might be exposed in a debt-heavy estate.

Navigating the Tax Implications

Avoiding probate is not the same as avoiding taxes. That’s a crucial distinction that can save beneficiaries from some very costly surprises down the road. Several types of taxes can still come into play.

- Income Tax on Retirement Accounts: When you inherit a traditional 401(k) or IRA, you’re inheriting pre-tax money. As you withdraw funds from that account, you will have to pay income tax on every dollar, based on your own ordinary income tax rate.

- Capital Gains Tax and the ‘Stepped-Up Basis’: For assets like a jointly owned home or a brokerage account with a TOD designation, the tax situation is often much better. These assets typically get a “stepped-up basis” in value as of the date of the owner’s death. This is a huge benefit—it means if you sell the asset shortly after inheriting it, you will likely owe little to no capital gains tax.

- Estate Taxes: Texas doesn’t have its own state inheritance tax, but very large estates might still be on the hook for federal estate taxes. For federal purposes, it doesn’t matter whether an asset is probate or non-probate; both are included when calculating the total value of an estate.

These rules can get complex, and every family’s situation is different. For a broader perspective on how asset planning intersects with tax law, you might find it helpful to explore more financial and tax articles.

Ultimately, the best way to navigate this is to consult a professional who understands both Texas probate law and the tax code. They can help ensure everything is handled correctly, preventing unexpected tax bills and protecting your family’s inheritance.

When You Need a Texas Probate Attorney

While many non probate assets seem to transfer smoothly on paper, trying to navigate every detail alone—especially while grieving—is a burden no family should have to carry. Knowing when to call for backup isn’t a sign of weakness; it’s a smart move to protect your loved one’s legacy.

Some situations are just too tangled or carry too much financial risk to handle without an experienced ally. Sometimes the fight comes from the outside, like a bank that drags its feet releasing funds, even when you have all the right paperwork. Other times, the trouble is internal, buried in confusing documents or conflicting family wishes.

Navigating Complex Scenarios

An attorney becomes absolutely essential when you hit certain red flags. These aren’t just minor hiccups; they are situations with serious legal and financial stakes, where one wrong step could ignite a family feud or undo your loved one’s intentions.

Think about reaching out for legal help if you run into any of these issues:

- Conflicting Beneficiary Designations: What happens if a life insurance policy names an old girlfriend, but a newer prenuptial agreement promises those funds to the current spouse? These kinds of conflicts require a deep dive into Texas law to sort out correctly.

- Outdated Beneficiary Forms: It’s a gut-wrenching discovery to find an ex-spouse is still the named beneficiary on a major retirement account. An attorney can help you explore any possible legal remedies, though these cases are often an uphill battle. This is an area where Probate Litigation may become necessary.

- Creditor Claims: If the estate has more debts than assets in probate, figuring out which non-probate funds (if any) can be used to pay creditors is a complex legal puzzle.

- Complex Family Dynamics: Blended families, estranged relatives, or simmering disagreements among heirs can turn a straightforward asset transfer into a source of lasting pain. Legal help can also be crucial if a loved one becomes incapacitated, which may involve a Guardianship proceeding.

These scenarios pop up more often than you might think. While an impressive 83% of Americans say estate planning is important, very few actually have the right legal structures in place to manage their assets without a hitch. An attorney brings clarity to the chaos, helps you sidestep costly mistakes, and offers peace of mind when you need it most.

Your Partner in Probate and Estate Planning

At The Law Office of Bryan Fagan, we’re not just lawyers; we’re partners who can help your family navigate these challenges with confidence and compassion. Whether you need a guide through the entire Texas Probate Process or help creating foundational documents like Wills & Trusts, our team is here to provide the clear, supportive guidance you deserve.

Key Insight: A free consultation is one of the most powerful first steps you can take. It’s a no-risk way to understand your legal standing, map out your options, and make informed decisions without any upfront cost. It’s your chance to find a clear path forward during a deeply confusing time.

Don’t let a small question mark grow into a major legal battle. Reaching out early is the best way to protect both your loved one’s wishes and your family’s future.

Frequently Asked Questions About Texas Non Probate Assets

When you’re dealing with an estate, a lot of questions pop up. It’s completely normal. Here are some of the most common ones we hear from Texas families about non-probate assets, answered in plain English.

Do Non Probate Assets Avoid Taxes

This is a huge point of confusion for many people. While these assets skip probate court, they don’t necessarily skip taxes. The good news is that Texas has no state inheritance or estate tax.

However, federal taxes might still come into play. A classic example is an inherited traditional 401(k) or IRA. When the beneficiary takes distributions from that account, they’ll owe income tax on the money, just as the original owner would have.

What if a Beneficiary Has Already Died

It happens more often than you’d think. If the primary beneficiary you named on an account has passed away, the asset will typically go to the contingent beneficiary—that’s the backup person you designated.

But what if you never named a backup? In that case, the asset often loses its non-probate status. It gets pulled back into the estate and will almost certainly have to go through the probate process to determine who legally inherits it.

Can a Will Override a Beneficiary Designation

The answer is a firm no. A will cannot and does not override a beneficiary designation on a life insurance policy, POD account, or retirement fund. Think of that designation as a direct contract between you and the financial institution—and it’s legally binding.

This is exactly why it’s so critical to review and update your beneficiaries regularly. Life changes. After a marriage, divorce, or the birth of a child, updating these forms should be at the top of your to-do list.

Are Cars with a TOD Designation Non Probate Assets

Yes, they are, and it’s a fantastic tool for Texans. The Texas Estates Code specifically allows vehicle owners to add a Transfer on Death (TOD) designation to their car titles.

It’s a simple form, but it’s powerful. This one step allows your vehicle to pass directly to the person you name, completely bypassing the probate court for that specific asset. It saves a lot of time and hassle.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.