Skip to content

Skip to content A bank statement after a death can feel heavier than it should. You're grieving, sorting mail, and trying to figure out whether the money in that account can pay a mortgage, cover funeral costs, or remain safe until someone has legal authority to act.

Most families don't know what happens next, and that's normal.

In Texas, a bank account doesn't all follow one rule. What happens depends on how the account was set up. A payable-on-death beneficiary, joint ownership terms, or trust ownership can keep the account outside probate. A sole-owned account with no transfer feature often becomes part of the probate estate. That distinction matters because it affects who can access the money, how long things may take, and whether the bank will freeze the account.

If you're trying to understand What Happens to Bank Accounts During Probate in Texas?, the answer usually starts with one practical question: was this account designed to transfer automatically, or will the court need to authorize someone to manage it?

Families often find relief once they know which lane they're in. The legal process may still require paperwork, but confusion starts to lift.

If you need a broader overview of court procedure, our guide to the Texas probate process can help you place bank accounts in the larger estate-administration picture.

Navigating a Loved One's Finances After Loss

On Monday, Social Security lands in your mother's checking account. On Tuesday, the electric bill auto-drafts. By Wednesday, the bank has been told about the death, and the account that kept the household running is suddenly restricted.

That whiplash is one of the hardest parts for families. Grief is already heavy. Then ordinary money tasks start breaking all at once.

A bank freeze usually does not mean the bank is being difficult. It means the bank is putting up a temporary gate until it knows who has legal authority to act. In probate, that gate matters. It protects the account from the wrong person taking funds, but it also creates real day-to-day problems if mortgage payments, insurance premiums, streaming charges, or payroll deposits were still flowing through that account.

Why families get confused

Many families expect the will to act like a master key. In real life, a bank often looks first at the account agreement, the title on the account, and any beneficiary form on file. That is why one account may stay available to a surviving co-owner while another is frozen pending probate, even though both belonged to the same person.

Joint accounts can add another layer of confusion because "joint" does not always mean the survivor automatically owns the funds. The account paperwork has to include the right survivorship language. Our explanation of Texas joint accounts with right of survivorship covers that distinction in plain terms.

A good starting question is simple. How was this account set up at the bank?

Practical rule: Before you assume probate controls the account, check the account title, any payable-on-death beneficiary, and whether automatic payments or direct deposits are tied to it.

What to gather first

Before calling every bank and credit union, collect the documents that help you see the full picture:

- Recent bank statements so you can confirm the exact account names and identify where money was regularly coming in and out

- The death certificate because the bank will usually ask for it before discussing account status

- Any will or trust documents that may identify the person expected to act for the estate

- A list of automatic drafts and direct deposits so you can spot immediate pressure points, such as utilities, mortgage payments, insurance, pension income, or government benefits

That last step saves families a lot of frustration. The legal question is who can access the funds. The practical question is what happens this week if the water bill drafts tomorrow and the paycheck or benefit deposit is still headed to a restricted account. Both questions matter, and most families are dealing with both at the same time.

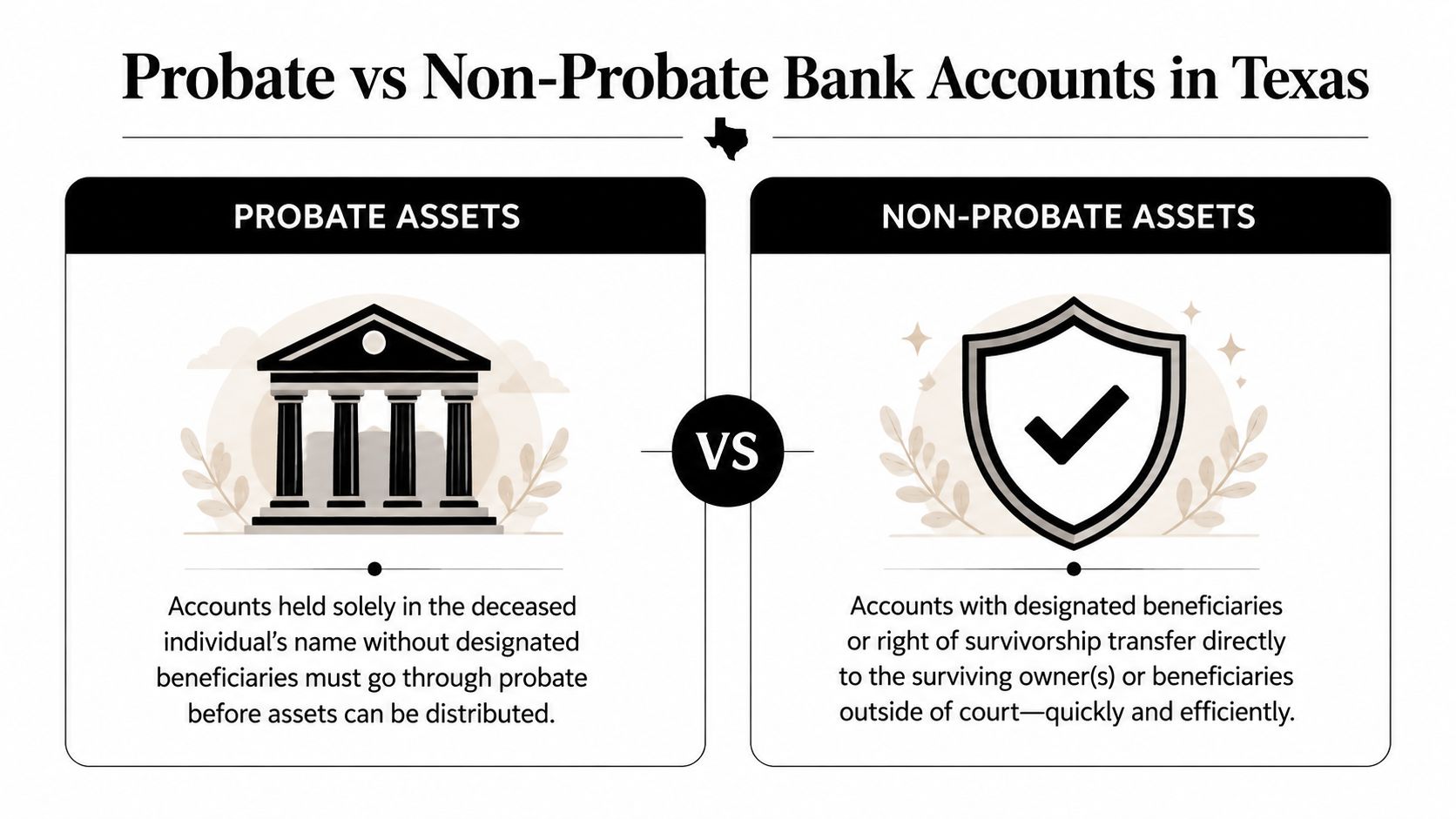

Which Bank Accounts Must Go Through Probate

A helpful way to sort this out is to ask one question first: did the account already have instructions for what happens at death?

If the answer is no, the account usually becomes part of the estate and probate is often needed before anyone can access it. If the answer is yes, the bank may be able to transfer the funds directly under the account paperwork.

That sounds simple. In practice, families often face difficulties at this stage. They are not only asking who inherits the money. They are also trying to figure out what happens to the electric bill on autopay, the Social Security deposit scheduled for next week, or the rent payment that normally comes out on the first.

The dividing line

Probate usually applies to a bank account when the deceased person owned it alone and did not name a payable-on-death beneficiary or place it in a trust. In that situation, the bank will often freeze access until the proper estate representative has court authority.

Accounts often pass outside probate when the bank's records already name who receives the funds. Common examples include a payable-on-death designation, a valid right of survivorship agreement, or trust ownership.

A beneficiary designation works like a set of written delivery instructions. The bank looks to that instruction first. A right of survivorship means the surviving owner receives the account automatically, but only if the account agreement clearly created that right.

How Texas Probate Treats Different Bank Accounts

| Account Type | Goes Through Probate? | How It Transfers |

|---|---|---|

| Solely owned account with no beneficiary | Usually yes | Through the estate, after court authority is established |

| Account with payable-on-death beneficiary | Usually no | Directly to the named beneficiary |

| Joint account with right of survivorship | Usually no | To the surviving account holder under the account agreement |

| Account held in a trust | Usually no | Managed and distributed under the trust terms |

Four common account setups

Sole-owned checking or savings account

This is the account that most often creates immediate pressure. If only the decedent owned the account and no beneficiary was named, the bank will usually treat the funds as estate property. Even a close family member usually cannot withdraw money just because they helped with bills before death.

This is often the account tied to everyday life. Mortgage drafts, streaming subscriptions, insurance premiums, and income deposits may all be hitting the same account. So while the legal issue is probate, the day-to-day issue is cash flow disruption.

Payable-on-death account

A POD account usually passes directly to the named beneficiary through the bank's claim process. The money generally does not have to go through probate first.

Still, families should pause before spending it. A direct transfer solves the ownership question, but it does not automatically solve the household bookkeeping problems already in motion.

Joint account

A joint account may avoid probate, but only if the account documents include survivorship language. Many families hear "joint account" and assume the survivor automatically owns everything. Texas law is more exact than that. The signature card and account agreement matter.

If you need help checking the wording, this guide to joint accounts with right of survivorship in Texas explains what to look for.

Trust account

If the account is titled in the name of a trust, the successor trustee usually handles it under the trust terms instead of through the probate court. In many families, these accounts cause less delay because the trust document already names who can step in and act.

Banks usually follow the account contract and beneficiary records before they follow family assumptions.

As you review each account, look beyond the balance. Check the title on the statement, the ownership type, any beneficiary listed, and whether the account is connected to regular deposits or automatic payments. That is often where the first real problems show up.

The Executor's Role Accessing and Managing Estate Funds

When a bank account does belong to the estate, someone has to step into a legal role and handle it properly. In many Texas estates, that person is the executor named in the will. If there's no will, the court may appoint an administrator to serve a similar function.

What gives the executor authority

The key court document is usually Letters Testamentary. In plain English, this is the court's written confirmation that the executor has authority to act for the estate. Banks usually won't release probate funds until they see the death certificate and the proper court-issued letters.

That's why being named in the will isn't enough by itself. The will names the person. The court officially authorizes the person.

What the executor usually does with bank funds

Once appointed, the executor's job is more than collecting money. It involves organization and separation.

- Notify the bank of the death and ask what documents the institution requires.

- Present the death certificate and court letters so the bank can verify authority.

- Identify which funds belong to the estate and which pass outside probate.

- Open an estate bank account to receive probate funds and pay estate expenses.

- Avoid mixing estate money with personal money, even for short-term convenience.

That estate account matters. It creates a clean record of what came in, what was paid out, and what remains for distribution to heirs or beneficiaries.

Finding accounts you don't know about

Sometimes the problem isn't access. It's uncertainty. The family suspects a bank account exists but doesn't know where, or doesn't know whether the balance is small enough to use a simplified procedure.

Texas law provides a Chapter 153 court mechanism that allows an interested person to obtain a court order compelling a bank to disclose a deceased's account balances. This can help determine whether non-exempt assets fall below the $75,000 threshold for a Small Estate Affidavit and may help avoid full probate administration, as explained in this discussion of obtaining deceased bank account information in Texas.

A practical overview of account handling after death is also available in this article on estate bank accounts in Texas probate.

A short video can also help if you're trying to picture how the paperwork fits together:

For many families, the hardest part is waiting. But once the executor has legal authority and a proper estate account, the financial side of the estate usually becomes much easier to manage.

A Real-World Example The Tale of Two Accounts

Consider a fictional Texas family, the Jacksons.

Their father dies with two bank accounts. One is a savings account with his daughter Elena listed as the payable-on-death beneficiary. The other is a checking account he used for his monthly bills, and that checking account is in his name alone with no beneficiary on file.

The account that moved quickly

Elena calls the bank about the savings account. The bank confirms she's the named beneficiary and asks for identification and a death certificate. After that process is complete, the funds can transfer to her without the account becoming part of the probate estate.

That feels straightforward because the bank already has instructions on file for what happens at death.

The account that stopped cold

The checking account is different. It's the account tied to household bills, a streaming service, and a few automatic drafts Elena didn't even know about. Once the bank receives notice of death, access is restricted.

Elena can't just use her father's debit card to “keep things going.” Even with good intentions, that creates risk.

The account that paid daily bills during life is often the account that creates the most stress after death.

What Elena had to do next

Her father left a will naming Elena as executor, so she files the will with the probate court. After the court admits the will and issues Letters Testamentary, Elena returns to the bank with the required documents.

She then closes out the probate-related funds from the frozen personal account and moves them into an estate account. From there, she can pay proper estate expenses and keep records of every transaction.

The Jacksons' two accounts teach the lesson many families learn the hard way. The bank doesn't treat all money the same after death. One account can pass by contract. Another may require court authority before a single dollar moves.

Common Problems with Bank Accounts in Probate

The hardest part for many families is not figuring out who inherits the money. It is getting through the weeks when the account that handled ordinary life suddenly cannot.

A parent dies, the bank restricts the checking account, and the practical problems start piling up fast. The mortgage company still drafts on the first. The electric bill is still set to autopay. A pension payment may arrive after death and need to be returned. A debit card stored in half a dozen online accounts keeps triggering attempted charges. The legal process may be orderly, but the household cash flow often is not.

The Texas State Law Library's guide on steps to take before probate is helpful for the early checklist. Families often need one more layer of guidance, though. They need a plan for the day-to-day money problems that show up before an executor has full control.

The day-to-day trouble spots

A frozen account can create several separate headaches at once:

- Mortgage or rent payments bounce even though the home still has to be protected

- Utilities and insurance stop drafting unless someone contacts each company and arranges a new payment method

- Subscriptions and memberships keep billing until they are canceled one by one

- Direct deposits cause confusion because some payments can stay in place temporarily, while others may need to be reported or returned

- Online access is limited because being able to see an account online is not the same as having legal authority to use it

- Out-of-state executors lose time when a local branch wants original documents or in-person identity verification

This is why families often feel stuck. The money may exist, but the account that used to run the household is no longer available for ordinary use.

Delay creates pressure

Probate takes time, and bills do not pause while paperwork moves through the court.

That gap creates real friction. A house still needs electricity. Property insurance still needs to stay active. Someone has to track which charges should be stopped, which must still be paid, and which deposits should not be spent. If you are trying to understand how banks may release funds without full Texas probate, it helps to explore those limited options early, especially when a family is short on accessible cash.

Good records matter here. Keep a running list of failed drafts, incoming deposits, companies contacted, and deadlines. That simple habit can save an executor from repeated confusion later.

Disputes, debts, and mixed messages

Some problems are administrative. Others are personal.

A family member may believe joint use during life meant ownership after death. Another relative may insist the money should be divided under the will. A creditor may contact the bank or the executor claiming the estate owes a balance. When several people are calling the same institution with different instructions, banks tend to slow everything down and ask for formal proof before releasing funds.

Small business owners often run into an extra layer of confusion when personal and business cash flow overlap. If that applies to your family, it can help to understand related financial rules, including MCA laws in Texas for small businesses, because merchant cash advances and similar obligations can complicate what looks like an ordinary bank account problem.

If your family is dealing with a disagreement over ownership, administration, or distribution, our Probate Litigation page explains how contested probate issues are typically handled.

Can You Access Funds Without Full Probate

Sometimes, yes.

A full probate administration is not the only path in Texas, and that matters when a family is staring at a frozen checking account while rent, utilities, or insurance drafts are still trying to hit. In the right estate, a shorter court procedure can give you a lawful way to deal with limited assets without the time and expense of a full administration.

Simpler procedures that may fit

Texas law provides a few simplified options, but each one fits only certain facts. The right tool depends on the size of the estate, whether there is a valid will, whether debts remain, and how the account was titled.

- Small Estate Affidavit may help in a qualifying smaller estate when the estate meets the legal requirements and a full administration is unnecessary.

- Muniment of Title can work when there is a valid will and no need for ongoing estate administration, often because debts are limited or already resolved.

- Order of No Administration may be available in narrower situations involving very small estates.

These options are less like a shortcut and more like using the correct lane at the courthouse. If the estate fits, the process is lighter. If it does not, the bank will usually keep asking for stronger proof of authority.

Why families ask about these options so early

The question is rarely abstract. It is usually practical.

A surviving spouse may need to stop duplicate auto-payments. An adult child may need to redirect a pension deposit that arrived after death. A family may need funds for funeral costs while waiting on court paperwork. In those moments, the issue is not just who inherits the account. The issue is how to keep the household from slipping into avoidable chaos during the waiting period.

If you are trying to sort out whether a bank might release money without opening a full probate case, this guide on how banks may release funds without Texas probate gives a useful overview of the situations where that can happen.

Business owners can face an extra layer of friction. If personal and business cash flow overlapped, the family may also need to review contracts or funding arrangements tied to incoming receivables. In that setting, it can help to understand MCA laws in Texas for small businesses, especially if a lender or processor is still pulling payments from an account affected by the death.

A careful word about timing

Banks do not all treat these procedures the same way. Even when a family qualifies for a simplified option, the institution may still ask for certified court documents, a death certificate, identification, and time to review everything internally.

That delay can feel frustrating, but it is common. The bank is trying to avoid releasing funds to the wrong person.

When legal guidance helps

These procedures can save time, but only if the estate truly qualifies. A family can lose weeks by pursuing a small-estate option that does not match the debts, the account structure, or the wording of the will.

The Texas Estates Code controls these procedures, and related questions sometimes overlap with incapacity planning or the care of a surviving relative who now needs help managing finances. If that is part of your family's situation, our Guardianship resources may also be useful.

The Law Office of Bryan Fagan, PLLC handles probate administration, small estate affidavits, muniment of title proceedings, and related estate matters for Texas families who need help choosing the procedure that fits their situation.

Key Insights and Your Next Steps

When families ask what happens to bank accounts during probate in Texas, the answer usually comes down to a few core points.

Key insights

- Account setup controls the outcome. A beneficiary designation, survivorship feature, or trust title can keep an account outside probate. A sole-owned account without those features often can't be accessed until proper estate authority exists.

- A will doesn't provide access to an account by itself. The court process matters because banks usually want formal proof that the right person is authorized to act.

- The executor's job is practical, not just legal. The work often includes locating accounts, presenting documents, opening an estate account, tracking bills, and sorting out failed drafts or deposits.

- Frozen accounts create real-life friction. Mortgage payments, utilities, subscriptions, and other automatic transactions may need immediate attention.

- Some estates qualify for a simpler route. Small estate procedures and muniment of title can be valuable when the facts fit.

If you're overwhelmed, start with one question per account: Who owned it, and who was named to receive it at death?

That small step often tells you whether you're dealing with a direct transfer problem or a probate problem.

Texas Estates Code Titles 2 and 3 provide the legal framework, but families still need a clear plan for the bank, the court, and the unpaid bills that don't pause for grief. If you're handling this from another city, another state, or while supporting other relatives, experienced guidance can save time and avoid mistakes.

If you're facing probate in Texas, our team can help guide you through every step, from filing to final distribution. Schedule your free consultation today with Law Office of Bryan Fagan, PLLC.