The call often comes at the worst moment. A parent has just passed. You're still making funeral arrangements, and then someone asks, “What about the bank accounts?”

You find a checkbook in a drawer, maybe a stack of statements, maybe online banking alerts still hitting a phone. Bills are due. A mortgage may still be drafted automatically. Utilities might be linked to the same account. If you've been named executor, it's normal to feel pressure right away.

Most families assume a spouse, adult child, or named executor can walk into the bank and sort it out. Texas probate law rarely works that way. Banks care about authority, paperwork, and account title. That can feel cold when your family is grieving, but there is a reason for it.

If you're dealing with frozen accounts after a death in Texas, the most helpful thing you can know is this: there is a path forward. It may involve probate. It may not. The right answer depends on what kind of account your loved one had and whether someone was legally named to receive it.

Losing a Loved One and Facing the Bank

Maria's father dies unexpectedly. A few days later, she finds two bank statements on the kitchen counter. One account looks like his everyday checking account. The other may be a savings account. Her father named her as executor in his will, so she assumes she can go to the bank, show her ID, and transfer the money where it needs to go.

The bank employee is kind, but the answer is still no.

That moment confuses a lot of families. Maria isn't being accused of doing anything wrong. The bank isn't trying to be difficult. It cannot rely on family relationships alone. In Texas, the bank wants legal proof that the person asking for access has authority to act for the estate.

That's where many executors get stuck. They know there's money in the account. They know bills still need attention. They know the loved one trusted them. But they don't yet have the court documents the bank needs.

The process becomes easier once you break it into pieces. First, identify what kind of account it is. Second, figure out whether the account passes through probate or outside of it. Third, if probate is required, get the court authority that allows you to act.

You do not need to solve everything in one day. You need to take the next correct step.

Why Banks Freeze Accounts After a Death

When a Texas bank learns that an account holder has died, it often restricts access to an account that was held in that person's name alone. Families describe this as the account being “frozen.” In practical terms, that means the bank won't freely release funds until the right person shows up with the right authority.

The bank is protecting the estate

This freeze is usually a protective step. The bank is trying to prevent unauthorized withdrawals, fraud, and family disputes. If the bank released money to the wrong person, it could harm heirs, creditors, and the estate itself.

Texas law focuses on legal authority, not informal family permission. The Texas State Law Library explains that in Texas, bank accounts usually aren't available for immediate withdrawal after death. Heirs or creditors generally must wait until the court appoints an executor or administrator, and if there is no will, they must wait at least 90 days from the person's death before seeking certain court access to account balances, as noted in the Texas State Law Library probate guidance.

Practical rule: Being the closest relative does not automatically give you authority over a deceased person's bank account.

That point matters under Texas Estates Code Title 2, which covers estates of decedents, including probate administration and the appointment of personal representatives. Until the court recognizes someone as the executor or administrator, the bank usually won't treat any family member as the person in charge.

Why the executor still has to wait

Many readers ask a fair question: “If the will names me executor, why can't I act right now?” The answer is that the will names you, but the probate court confirms your authority. In most probate estates, banks want Letters Testamentary if there is a will, or Letters of Administration if there is not. Those are court-issued papers that show the bank who may act for the estate.

A few terms in plain English help here:

- Executor means the person named in a will to handle the estate.

- Administrator means the person the court appoints when there isn't a will or no executor can serve.

- Letters Testamentary are the court papers proving the executor has authority.

- Letters of Administration are similar papers for an administrator.

The freeze is temporary, not permanent

A frozen account does not mean the money disappears. It means access is delayed until the bank sees lawful authority or confirms the account transfers outside probate.

That delay can be frustrating, especially when regular bills are still pending. But the freeze is part of a larger process designed to protect everyone involved and make sure the funds go where Texas law says they should go.

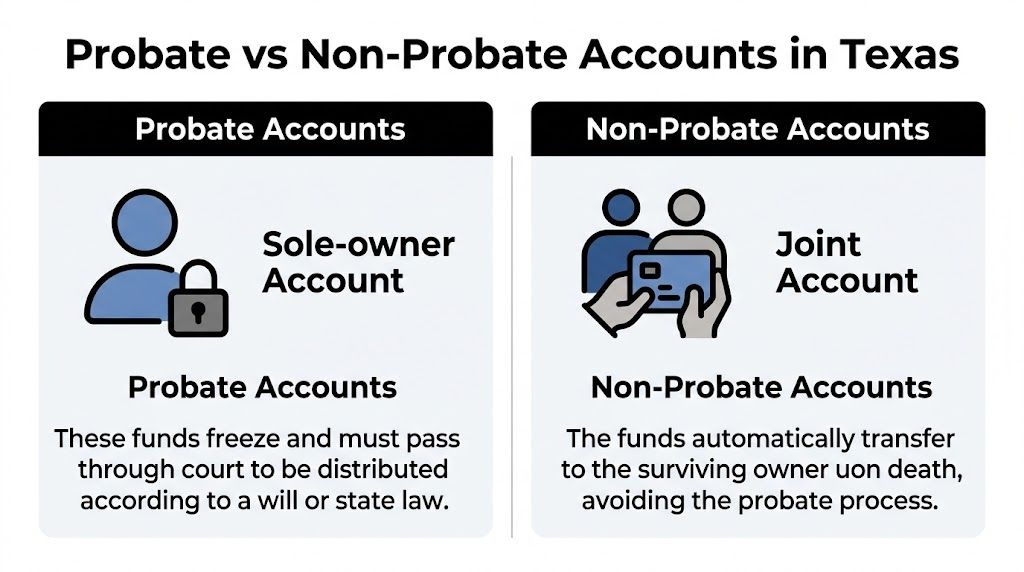

Probate vs Non-Probate How Your Account Type Matters

The most important question is not “Was there money in the bank?” It's how the account was titled.

Probate accounts

A bank account often goes through probate if it was owned only by the person who died and there is no beneficiary designation that controls what happens next. In that situation, the funds usually become part of the estate and are handled under Texas Estates Code Title 3, which deals with administration of estates.

For an executor, that usually means the account remains restricted until the court appoints a personal representative and the bank receives the required documents.

Common examples of probate accounts include:

- Single-owner checking accounts with no payable-on-death designation

- Single-owner savings accounts with no transfer mechanism outside probate

- Accounts the family thought were joint, but the paperwork does not create survivorship rights

Non-probate accounts

Some bank accounts transfer outside probate. These are often easier for families because the money passes directly to the person named in the account agreement.

Texas law resources explain that payable-on-death accounts transfer directly to the named beneficiary without court involvement, and the beneficiary can usually receive the funds by presenting the bank's required documentation, as described in TexasLawHelp's explanation of payable-on-death bank accounts.

Here is the basic comparison:

| Account type | Usual path after death | What the bank usually wants |

|---|---|---|

| Sole-owner account with no beneficiary | Probate | Court authority from the personal representative |

| POD account | Direct transfer to named beneficiary | Bank-required documentation |

| Joint account with valid survivorship terms | Direct transfer to surviving owner | Proof of death and bank paperwork |

| Account owned by a trust | Managed under trust terms | Trust documents and related paperwork |

A will does not automatically change a bank account's built-in transfer terms. The account agreement still matters.

Joint accounts are where families get confused

Many Texans believe that adding someone to an account means that person automatically owns the balance when the other owner dies. Texas law is more exact than that. A joint account does not automatically include survivorship rights unless the account agreement clearly says so.

That issue appears in the Texas Estates Code provisions governing multiple-party accounts. In plain English, if the paperwork does not clearly create a right of survivorship, the surviving co-owner may not automatically take the account outside probate.

This is one reason account documents matter so much. The label “joint” by itself doesn't always answer the legal question.

A quick real-world example

Suppose Daniel dies with two accounts:

- A checking account in his name alone

- A savings account that names his daughter as POD beneficiary

The checking account may need probate administration. The savings account may pass directly to the daughter through the bank's beneficiary process. Same person. Same bank. Different result.

Families planning ahead often benefit from learning more about understanding your power of attorney options, but it's important to remember that a power of attorney ends at death. After death, account access depends on probate authority, beneficiary designations, trust terms, or survivorship language.

If you're trying to sort out which assets avoid court and which do not, it helps to review the category of non-probate assets in Texas.

An Executor's Step-by-Step Guide to Managing Estate Funds

Once you know an account belongs to the probate estate, your role becomes more practical. You are no longer asking, “Can I get the money today?” You're asking, “What paperwork do I need, and in what order?”

Step one, get appointed by the probate court

If there is a will, the usual starting point is filing the will with the appropriate Texas probate court and asking the court to admit it to probate. If there is no will, the process is different, but the same core principle applies: the court must appoint someone with authority to act.

For many executors, the key document is Letters Testamentary. Without it, the bank often will not let you move estate funds.

Texas probate guidance notes that an executor may need Letters Testamentary just to open a new estate account and move assets into it, and the process can take time because institutions may require death certificates, notarized forms, and other paperwork, especially for out-of-state representatives, as explained in this discussion of Texas probate and estate bank account access.

Step two, get an EIN and open an estate account

A common mistake is trying to use the deceased person's old checking account as if nothing has changed. That usually creates accounting problems.

Instead, the executor often opens a new estate account. Think of it as the estate's temporary checking account. Estate money is gathered into this account, and from it, approved expenses, debts, and later distributions are paid.

Why this matters:

- Clean recordkeeping: You can track what came in and what went out.

- Separation of funds: Estate money should not mix with your personal money.

- Better administration: It's easier to prepare inventories, accountings, and final distributions.

Keep every receipt, statement, and deposit record. Executors get into trouble less often because of bad intent than because of poor records.

Step three, present the bank with the right documents

After appointment, you'll usually contact each bank and ask what its estate department requires. Many banks want some combination of:

- Certified death certificate

- Letters Testamentary or Letters of Administration

- Your identification

- Bank-specific claim or transfer forms

- Possibly notarized paperwork

Delays often happen at this stage. Different institutions have different internal procedures, even when the legal authority is clear.

For readers who want a visual overview, this short video walks through related probate concepts:

Step four, move estate funds into the estate account

Once the bank accepts your authority, the frozen funds are often transferred into the estate account. If your loved one had multiple accounts at multiple banks, this can take patience.

A realistic example helps. Assume Kevin lives in Houston and is executor for his aunt's estate. She had one checking account at a local bank and one savings account at a national bank. Kevin is appointed executor, gets certified copies of his Letters Testamentary, opens an estate account, and submits each bank's required paperwork. One bank processes the transfer quickly. The other asks for a notarized form and a fresh death certificate copy. Nothing is unusual about that. It's just administrative work that has to be completed correctly.

Step five, pay proper expenses before making distributions

The money in the estate account is not automatically ready to hand out to family members. The executor has duties under the Texas Estates Code to handle valid estate obligations and administration tasks before making final distributions.

That may include:

- Securing incoming funds, such as balances from probate accounts.

- Paying approved estate expenses, such as certain court and administration costs.

- Addressing valid debts or claims according to Texas law.

- Distributing the remaining balance to the beneficiaries or heirs entitled to receive it.

If you're an executor working across state lines, or if the estate involves several institutions, a probate attorney, CPA, and bank estate department can each play a role. The Law Office of Bryan Fagan, PLLC is one Texas firm that assists with probate filings, estate administration, and related account-transfer issues.

Common Bank Account Problems During Probate

The legal steps are manageable. The stress usually comes from timing, uncertainty, and competing demands.

Bills are due, but the account is frozen

This is often the first crisis. Mortgage drafts, utility bills, insurance payments, and tax obligations don't stop just because an account is restricted.

One Texas probate source reports that simple estates may gain bank access in about 4 to 8 weeks, while more complex estates can take months, and the account freeze can immediately disrupt automatic payments until a court-appointed representative presents legal authority, according to this guide on Texas probate bank account access.

That doesn't mean every bill goes unpaid. It means the executor must be careful and strategic. Sometimes family members temporarily cover urgent expenses and later seek reimbursement through proper estate administration. Sometimes creditors or service providers will work with the family once they understand probate is pending. Documentation matters.

The family disagrees about who should receive the money

This usually happens when account paperwork is unclear, when someone expected to be a beneficiary but wasn't, or when a joint account does not clearly include survivorship rights.

If the bank sees conflicting claims, it may refuse to guess. In some disputes, the matter can turn into probate litigation or a separate court proceeding where a judge determines who has the better legal claim.

When a bank is unsure, caution is normal. The institution is trying to avoid releasing money to the wrong person.

Out-of-state executors face extra friction

An executor who lives outside Texas often has the same legal authority as a local executor once appointed, but the paperwork process can feel slower. Banks may ask for certified documents, notarized forms, identity verification, and mailing delays can add another layer of frustration.

A few practical habits help:

- Call before visiting: Ask for the bank's estate department requirements in writing if possible.

- Order multiple certified copies: You may need them for several institutions.

- Track every submission: Keep a log of dates, names, and requested documents.

- Don't distribute funds too early: Wait until the estate's obligations are properly addressed.

Creditor claims can change the timing

Executors often feel pressure from heirs who want immediate distributions. But estate funds may need to remain in the account while claims, expenses, and other administration issues are resolved under Texas law.

That is why rushing can create personal risk for an executor. If you distribute funds too early and valid obligations remain, fixing the problem later can be expensive and unpleasant.

Key Insights for Texas Heirs and Executors

If you've been asking, “What Happens to Bank Accounts During Probate in Texas?”, the answer depends less on family relationships and more on account title, beneficiary designations, and court authority.

Takeaway

- Account type controls the path: A sole-owner account may need probate, while a POD or properly structured survivorship account may transfer directly.

- Court papers matter: For probate accounts, banks usually want Letters Testamentary or similar court authority before releasing funds.

- The estate needs its own workflow: Executors often need a separate estate account, organized records, and a careful plan for expenses and distributions.

- Delays are common, not a sign of failure: A slow bank response usually means the institution is following its internal estate procedures.

- Planning ahead can reduce family stress: Wills, trusts, beneficiary designations, and careful account setup can make things much easier later.

Texas families also benefit from learning how the broader Texas probate process works, when guardianship matters may arise for vulnerable loved ones, how wills and trusts shape asset transfers, and when probate litigation becomes necessary if disputes develop.

If you're the executor, you do not have to know every answer on day one. Your job is to protect the estate, follow the court's process, and make decisions carefully. With the right guidance, that is completely manageable.

If you're facing probate in Texas, our team can help guide you through every step from filing to final distribution. Schedule your free consultation today with Law Office of Bryan Fagan, PLLC.