Skip to content

Skip to content In Texas, the estate itself usually pays the taxes during probate, not the beneficiaries directly. Texas has no state inheritance tax and no state estate tax, and for someone dying in 2025, federal estate tax applies only if the estate exceeds $13.99 million.

If you've just been named executor, that answer may bring some relief, but it probably doesn't make the job feel simple yet. You're grieving, paperwork is piling up, and now you're expected to sort out tax returns, deadlines, and bills that may come due before the estate has ready cash.

That confusion is common. Many executors assume “no Texas inheritance tax” means “no tax problem at all.” In real life, the hard part is usually not whether heirs owe tax for inheriting. The hard part is figuring out what the estate still owes, when it must be paid, and how to cover those bills without creating personal risk for yourself.

An Executor's First Question Who Pays the Taxes

Individuals stepping into this role often share the same concern. “Am I personally supposed to pay these taxes?” In most Texas probate cases, the answer is no. You manage the process, but you normally pay valid tax obligations from estate assets, not from your own checking account.

That distinction matters. An executor is the person named in a will to handle the estate. If there isn't a will or no executor can serve, the court may appoint an administrator. In either role, you're the estate's legal manager during probate. Under the Texas Estates Code in Titles 2 and 3, that job includes gathering assets, addressing debts, and distributing what remains only after proper administration.

What this means in plain English

Probate is the court-supervised process of transferring a deceased person's property, paying debts, and closing the estate. Taxes are part of those debts.

A few practical rules help keep this manageable:

- Use estate funds when available: Final tax bills, estate income taxes, and property taxes tied to estate assets are generally paid from the estate.

- Don't distribute too early: Heirs may be waiting on their inheritance, but taxes and other priority debts come first.

- Don't assume every tax applies: Some estates need only a final individual income tax return. Others may also need an estate income tax return.

Practical rule: Your job isn't to absorb the tax burden yourself. Your job is to make sure the estate handles it correctly and in the right order.

If you need a broader overview of how administration works before focusing on taxes, our guide to the Texas probate process can help place these duties in context.

Understanding Your Role and Texas Tax Law

Texas families usually get one piece of good news right away. Texas doesn't impose a state inheritance tax or a state estate tax. That means a beneficiary usually doesn't owe Texas tax solely because they inherited a house, a bank account, or other property.

That said, probate still involves tax work. The person who died is called the decedent. Everything they owned and owed becomes part of the estate for administration purposes. The executor or personal representative has authority, under the Texas Estates Code, to collect estate property, handle claims, and settle proper debts before distributing the remainder.

Three terms that clear up most confusion

Many executors feel overwhelmed because the same few words keep appearing in court papers and tax documents. Here's the plain-English version:

- Decedent: The person who passed away.

- Estate: The property, accounts, debts, and obligations left behind.

- Executor or personal representative: The person responsible for managing those affairs through probate.

This duty is practical, not just procedural. If the decedent still owed income tax, if the estate earns income after death, or if property taxes continue on a house in the estate, someone has to keep those issues organized. That someone is usually you.

Why the estate code matters

Titles 2 and 3 of the Texas Estates Code govern the administration of estates. You don't need to memorize sections to understand the central rule: the representative must handle estate business carefully and in the right order. That includes debts and taxes.

For many families, tax questions overlap with the house itself. If the estate includes a home, property taxes, title issues, and occupancy can all affect administration. If you're also sorting out residency or valuation questions, this overview of understanding Texas homestead exemption can help you think through one of the most common estate assets.

If you want a probate-specific explanation of how taxes fit into administration, this resource on probate taxes in Texas is a useful companion read.

The simplest way to think about your role is this: you stand in the middle between the estate's assets, the estate's debts, and the people waiting to inherit.

The Four Types of Taxes You May Encounter

You may open the mail and find four different tax notices tied to one estate. That does not mean four separate people are responsible. It means you have four buckets to sort, each with its own deadline and payment source.

For an executor, the hard part is often cash flow, not the tax label. An estate can look wealthy on paper because it owns a house, land, or investment account, while having very little cash available to pay a bill that is due now. If you pay heirs too early or ignore a deadline, that paper wealth does not protect you from problems later. This overview of debts and taxes in Texas probate gives more context on how these obligations fit together.

Texas Probate Tax Cheat Sheet

| Type of Tax | What It Is | Who Pays | Common IRS Form |

|---|---|---|---|

| Final individual income tax | The decedent's last personal income tax return for income received before death | The executor or other authorized filer, using estate funds if tax is owed | Form 1040 |

| Federal estate tax | A tax that applies only if the estate is large enough under federal law | The estate, administered by the executor | Form 706 |

| Estate income tax | Tax on income the estate earns after death | The estate, through the executor | Form 1041 |

| Property taxes | Taxes tied to real estate or other taxable property held by the estate | The estate | Varies by taxing authority |

The decedent's final income tax return

This return covers income the person received before death, such as wages, retirement payments, business income, or investment income. The filing duty usually lands on the executor or another authorized person.

The payment issue is where confusion starts. The tax belongs to the decedent, but if money is owed, it is usually paid from estate funds. If the estate has not been gathered yet, or most of it is tied up in a home or other illiquid asset, you need to plan carefully before distributing anything. A refund can also belong to the estate, which makes timing and paperwork matter in both directions.

Federal estate tax

Many executors worry about this first because it gets the most attention. In practice, it applies to relatively few estates, but it still deserves a careful check.

The cash-flow lesson here is easy to miss. Even if no federal estate tax is due, you may need valuations, account statements, and documentation to confirm that. If tax is due, the amount can be large enough that an executor has to consider whether liquid assets are available or whether property may need to be sold to raise funds. A house cannot write a check by itself.

Estate income tax after death

After death, the estate can become its own taxpayer if it earns income during administration. Interest, dividends, rent, and some business income can all fall into this category.

That creates a second track of tax responsibility. One track looks backward at the decedent's final personal taxes. The other looks at what the estate itself earns while you are managing it.

This can also create a practical trap. An executor may assume money sitting in an account is just being preserved, while the account is generating taxable income. If the estate receives rent from a house or mineral income from property, there may be tax due before the asset is ever sold and before beneficiaries receive anything.

Property taxes do not stop because probate is pending

County tax deadlines keep running even while the family is still sorting out ownership, access, and probate paperwork. If the estate holds a home, ranch land, or other taxable property, those bills can continue to come due during administration.

This is often the clearest cash-flow problem in probate. The estate may own a valuable house and still have no checking account with enough money to cover taxes, insurance, maintenance, and utilities. In that situation, the executor usually has to hold back available cash, collect income if any exists, or decide whether a sale is necessary to keep the estate current. Waiting too long can lead to penalties, interest, and pressure from heirs who do not yet see why the property cannot be handed over.

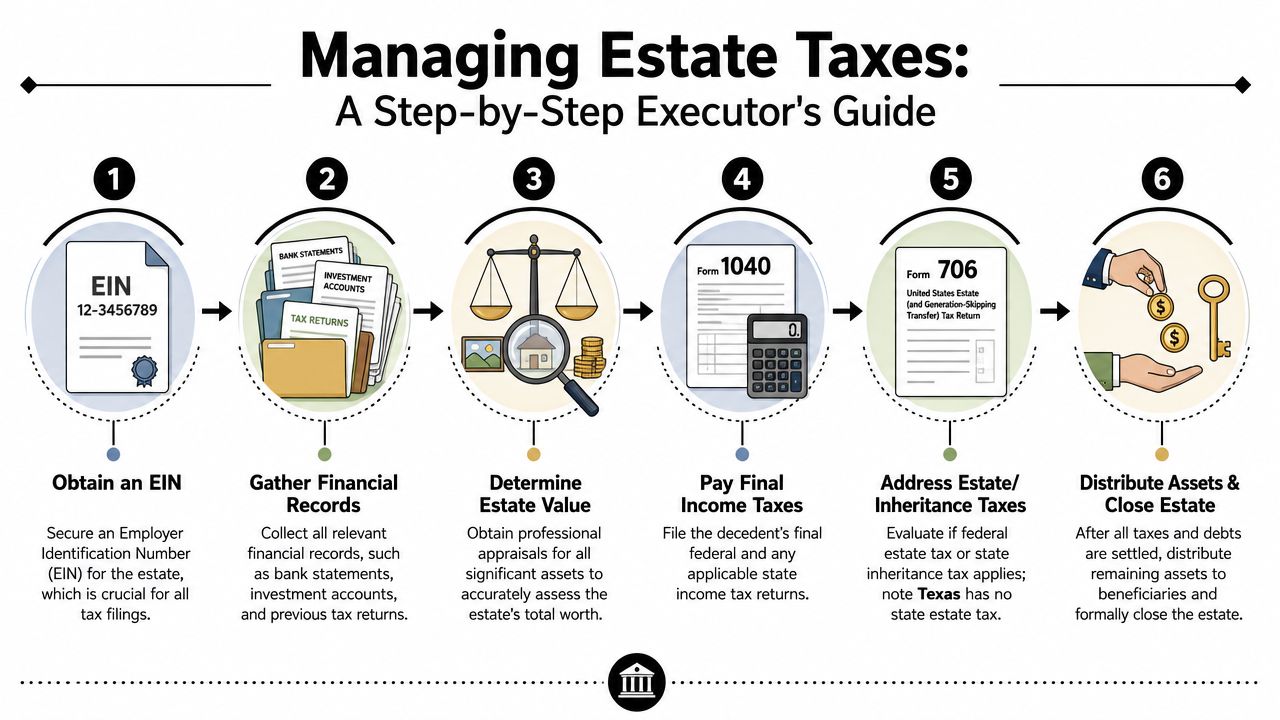

A Step-by-Step Guide to Managing Estate Taxes

As an executor, managing estate taxes requires a clear order of operations. Follow these steps in sequence to protect the estate and reduce the risk that a tax bill lands on your desk after money or property has already gone out to heirs.

Start by creating a clean financial lane for the estate

One of the first executor mistakes is trying to sort everything out from a personal account, a pile of mail, and memory. That creates confusion fast.

Begin by separating the estate's finances from your own.

- Apply for an EIN for the estate. The estate may need its own taxpayer identification number for banking and tax filing.

- Gather the core records. Collect prior tax returns, bank statements, brokerage records, deeds, loan documents, and any business paperwork.

- Open an estate bank account. That gives you one place to receive incoming funds and one place to pay approved expenses.

This recordkeeping step works like setting up a labeled file box before you start sorting family papers. It takes a little effort up front, but it prevents expensive confusion later.

Inventory assets with cash flow in mind

The next step is not just listing what the estate owns. You also need to ask a harder question. Which assets can pay a tax bill on time?

That distinction matters. A house, land, vehicles, or investment accounts may give the estate real value on paper while leaving you short on cash in practice. Executors often feel pressure from beneficiaries who see value and assume distributions can happen soon. Tax deadlines do not wait for an illiquid estate to become convenient.

As you prepare the probate inventory, note which assets are liquid, which produce income, and which may need to be sold or managed carefully to cover ongoing obligations.

Match each possible tax return to the estate's actual facts

Once the records and asset list are in place, identify what returns may be required. Many executors often feel overwhelmed at this stage, because there can be more than one tax track running at the same time.

You may need to deal with:

- The decedent's final individual income tax return, if there was reportable income before death

- The estate's income tax return, if estate assets earn income during administration

- A federal estate tax return, if the estate is large enough under current federal law

- Local property tax obligations, which continue while probate is pending

The question is not whether every estate has all four. The question is which of these apply to this estate, in this year, with these assets.

Build a tax calendar before paying heirs

After you know which filings may be required, put the deadlines in writing. Do not keep them in your head.

At minimum, note the due date for the final individual return, any estate income tax filing deadlines, property tax due dates, and any federal estate tax deadline if that issue is even potentially in play. A practical overview of debts and taxes in probate can help you connect those tax dates to the larger probate timeline.

This step protects cash. It also protects you.

If you distribute money too early and later discover a tax bill, you may have to chase funds back from beneficiaries or explain why the estate cannot pay a priority debt. That is a miserable position for any executor, especially a family member already carrying grief.

Reserve funds before making distributions

Treat estate cash like water stored for a long trip through West Texas. If you give it away too early, getting through the rest of the trip becomes much harder.

Before distributing property or funds, hold back enough to cover known taxes, expected filing costs, professional fees, and a reasonable cushion for surprises. That reserve matters most in estates that are asset-rich but cash-poor. A valuable home does not pay the IRS or the county tax office by itself.

Sometimes the practical solution is collecting income, delaying distributions, or considering a sale if the estate cannot stay current otherwise. Questions about liquidation often come up in many states. For a general look at process issues in another market, some families also read about selling inherited property in Florida, though Texas executors should still follow Texas probate procedure.

Get help before a missed deadline becomes your problem

You do not need to guess your way through tax filings. If the estate includes rental income, a closely held business, mineral interests, large investment accounts, or uncertain asset values, bring in a probate lawyer or CPA early.

A short consultation at the start often costs less than fixing a late filing, a penalty notice, or an avoidable distribution mistake. The goal is simple. Know what is owed, know when it is due, and make sure the estate has enough accessible funds to pay it before anyone takes their share.

Real-World Challenge The Estate Has a House but No Cash

Maria is named executor of her father's estate in Houston. She has her Letters Testamentary, access to his mail, and a growing folder of bills. The problem is simple on paper and stressful in real life. Her father owned a house free and clear, but there isn't much money in his bank account.

The heirs want to keep the home in the family. Maria wants that too. But the estate still has obligations. Her father's final income tax return may need to be filed. Property taxes on the house haven't disappeared. Utilities, insurance, and maintenance continue while probate is pending.

Why this situation creates real risk

The hard part isn't understanding that the estate pays taxes. The hard part is that the estate may not have liquid cash to do it.

Justia explains that taxes are high-priority debts, and an executor may face personal liability for penalties or interest if they fail to file or pay on time in its discussion of paying taxes from an estate. That means Maria cannot directly deed the house to the heirs and hope the remaining issues work themselves out later.

She has to stop and ask practical questions:

- Can the estate pay current tax bills from existing funds?

- Are there smaller assets that can be sold first?

- Will the heirs contribute funds temporarily, with proper documentation?

- Does the house itself need to be sold if no other solution works?

Maria's options before distribution

Maria meets with a probate attorney and a tax professional. Together, they map the estate's obligations and timing. Instead of making a rushed distribution, she holds the house in the estate while evaluating ways to create cash.

One option is to sell personal property or other minor assets first. Another is for heirs to advance funds to cover urgent estate expenses, with clear records showing whether those funds are loans or contributions. In some cases, a sale of the house becomes necessary because preserving the asset would put the executor at risk and leave the estate unable to satisfy priority debts.

Questions about selling real estate in probate come up in many states, not just Texas. For a comparison point on how these sales are handled elsewhere, this guide to selling inherited property in Florida shows how probate real estate issues often turn on timing, court authority, and marketability.

This short video also gives helpful context on probate administration concerns families commonly face:

If disagreements arise over whether property should be sold, who should carry costs, or how taxes affect the estate's real estate, our page on the impact of federal and state taxes on Texas real estate in probate addresses that intersection in more detail.

Common Tax Mistakes Executors Make and How to Avoid Them

Many executor tax problems start with pressure. A family wants answers, bills keep arriving, and the estate may own valuable property without having much cash in the bank. Under that kind of strain, even a careful executor can make a mistake that creates delay, conflict, or personal risk.

Distributing property before taxes are pinned down

This is one of the costliest errors because it feels kind and efficient in the moment. The executor sees grieving heirs, wants to reduce tension, and transfers money or property before the estate's tax picture is fully clear.

A better approach is to treat distributions like the last step, not the first reward. Before anything goes out, confirm which returns still need to be filed, estimate what may be owed, and hold back enough cash to cover taxes, preparation costs, and any surprise bill that arrives later. If the estate is asset-rich but cash-poor, that reserve matters even more.

Using personal funds or mixing accounts

This problem often starts with good intentions. An executor pays a property tax bill, insurance premium, or utility invoice from a personal checking account just to keep things current.

That shortcut can blur the paper trail.

Estate money should move through an estate account whenever possible. If you have to front an emergency expense, keep the invoice, proof of payment, and a written note explaining why the payment was necessary and whether reimbursement is expected. Clear records protect you if an heir later questions where the money went.

Missing that the estate may have its own filing duties

This point trips up many first-time executors because the person who died and the estate feel like one financial story. For tax purposes, they can be two separate taxpayers.

The decedent may need a final individual income tax return. The estate may also need its own income tax return if it earns income during administration, such as rent, dividends, interest, or sale proceeds that create taxable gain. As noted earlier, filing deadlines can arrive before the estate has easy access to cash. That is why executors need to identify possible returns early, especially when the main asset is a house, land, or a business interest rather than liquid funds.

Keeping weak records and skipping valuations

Poor documentation turns an already hard job into a harder one. If you cannot show what an asset was worth, when a bill was paid, or why money was held back, you may struggle to defend perfectly reasonable decisions.

Keep copies of returns, bank statements, appraisals, closing documents, receipts, correspondence with heirs, and notes about major choices. A house, for example, is not just a family asset. During probate, it is also a source of carrying costs, possible tax exposure, and valuation questions. Good records help explain why you delayed a distribution, sold an asset, or reserved cash.

A careful executor creates a paper trail that shows each decision was reasonable, documented, and made in the estate's best interest.

For more complicated estates, executors often work with a CPA, a tax preparer, and a probate firm such as Law Office of Bryan Fagan, PLLC. That kind of team approach can help when the estate has uneven cash flow, disputed asset values, or multiple filings due before property can be sold.

Key Insight Your Executor Tax Checklist

The hardest shift for many executors is not learning the tax rules. It is accepting that your job has changed. You may be a son, daughter, spouse, or sibling, but during probate you are also a fiduciary. That means you are the person expected to slow things down, protect estate funds, and make sure taxes are handled before anyone receives property.

That mindset matters most when the estate looks wealthy on paper but feels broke in real life. A house can carry sentimental value and market value at the same time, yet neither one pays the IRS, the county, or the accountant by itself. Until assets are sold, refinanced, or converted to cash in some lawful way, you may be responsible for meeting deadlines with very limited liquidity. The real insight is that probate tax work is often a cash management problem first and a tax filing problem second.

A practical checklist helps, but a decision filter helps more. Before you pay a bill or make a distribution, ask:

- Does this payment protect the estate or create risk for me personally?

- Is cash needed for a tax filing, property expense, or professional fee that is coming due soon?

- If the estate owns mostly illiquid assets, what is the plan to turn value into usable cash in time?

- Would I be able to explain this decision clearly to a court, a beneficiary, or a tax preparer six months from now?

Those questions keep you focused on order, timing, and proof. They also help you resist family pressure. An heir may see a house and assume there is plenty to divide. An executor has to see the same house and ask whether it is carrying unpaid taxes, insurance costs, maintenance expenses, or a sale timeline that could leave the estate short of cash.

If you remember one point from this article, make it this one: the estate usually bears the tax burden, but the executor bears the responsibility for making sure money is available, deadlines are met, and distributions do not happen too soon. That is how you protect the heirs, the estate, and yourself.

If you're facing probate in Texas, our team can help guide you through every step from filing to final distribution. Whether you need help with the Texas Probate Process, Wills & Trusts, Probate Litigation, or related estate issues, the attorneys at Law Office of Bryan Fagan, PLLC can help you understand your options and move forward with confidence. Schedule your free consultation today.