Losing a loved one is hard enough. Then the paperwork starts, the bank asks for documents you’ve never heard of, and family members begin asking when funds will be available. If you’ve been named executor, it’s normal to feel uncertain about what to do first.

In Texas, handling a deceased person’s bank accounts isn’t just an administrative task. It’s part of your legal duty under the Texas Estates Code, especially the rules in Titles 2 and 3 that govern estate administration, probate property, creditor issues, and distribution. The good news is that there is a path forward, and it becomes much easier once you understand why each step matters.

Many people searching for estate bank account probate texas are really asking a more human question: “How do I protect my loved one’s money, follow the law, and avoid making a mistake while I’m grieving?” That’s the right question to ask.

Your First Duty Managing Estate Finances with Care

When you become an executor, you step into a position of trust. You’re not acting for yourself. You’re acting for the estate, the beneficiaries, and in many situations, creditors too. That’s why one of your first responsibilities is to separate estate money from your own money.

Why your personal account is off limits

A common mistake happens early. An executor pays a funeral bill from a personal debit card, deposits a refund check into a personal checking account, or moves a deceased parent’s funds “just to keep things organized.” That feels practical in the moment. Legally, it creates risk.

Texas executors are expected to avoid commingling funds, which means mixing estate money with personal money. The estate should have its own account, its own records, and a clear paper trail. That separation helps you prove what came in, what went out, and why.

Practical rule: If the money belonged to your loved one or now belongs to the estate, it should move through the estate’s financial process, not through your personal account.

Why this matters so much in Texas probate

If someone dies without a will in Texas, and their bank accounts don’t have beneficiary designations, those accounts usually go through full probate. That process can take 6 to 12 months and consume up to 10% of the account’s value in fees, with administrator compensation alone ranging from 1% to 5% of the estate’s value, according to this discussion of what happens to bank accounts when someone dies without a will in Texas.

That doesn’t mean every estate becomes expensive or contentious. It means mistakes with estate funds can make a difficult process slower, costlier, and more stressful for everyone involved.

A steady starting point

An estate bank account is the central account used to receive estate money, pay valid estate expenses, and keep accurate records during administration. It becomes the financial hub of the probate estate.

If you want a plain-English overview of what that role involves day to day, this guide to estate executor duties can help frame the responsibility in practical terms. For a Texas-specific explanation of your authority and obligations, our page on understanding the duties of an executor of an estate is a useful next step.

Here’s the comforting part. You don’t need to solve everything on the first day. You do need to protect the money, slow down before moving funds, and make sure each step is legally supported.

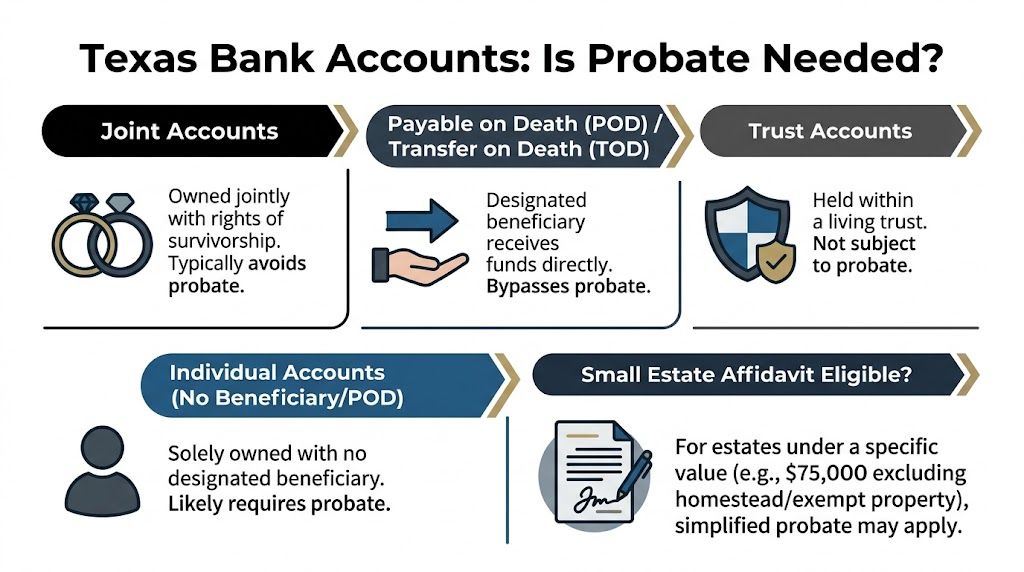

Does This Bank Account Require Texas Probate?

A common early stress point sounds like this: “The bank account is in Mom’s name, my name is also on it, and I need to pay bills. Can I just use it?” In Texas, the answer depends on the account paperwork, not on what the family assumed the arrangement meant. Slowing down here can prevent expensive mistakes, hurt feelings, and accusations later.

Accounts that may pass outside probate

Some bank accounts transfer outside the probate estate because the owner already put instructions in place with the bank or titled the account in a different legal name.

- POD accounts usually allow a named beneficiary to claim the funds from the bank after the owner’s death.

- TOD accounts can work in a similar way if the bank records were set up properly.

- Trust-owned accounts are often controlled by the successor trustee, if the account is titled in the trust’s name.

- Some small estates may use a simplified probate procedure instead of full administration.

The Texas State Law Library’s guide on bank accounts before probate explains why this question turns on the bank’s records. It also highlights a rule that surprises many families. In Texas, a joint account does not automatically mean the survivor owns everything after death.

The joint account trap

This is one of the most common sources of family conflict.

A son may have been added to an account only to help his father write checks or monitor expenses. After the death, the son may believe the account became his because his name was already there. Texas law may treat that account very differently if the signature card or account agreement does not include clear survivorship language.

Banks follow the contract on file. A will usually does not override a POD designation, and it usually does not create survivorship rights that were never written into the account documents.

A practical way to check the account

Work through the account like a folder with labels on it. The label determines who has authority, not the family’s memory of why the account was opened.

| Account question | Why it matters |

|---|---|

| Was there a POD or TOD beneficiary on file? | The bank may transfer the funds directly to that person. |

| Was the account owned by a trust? | The successor trustee may have authority instead of the executor. |

| Was it jointly owned? | You still need to confirm written survivorship language in the account records. |

| Was it solely owned with no beneficiary? | That usually means the account is part of the probate estate. |

If anything is unclear, ask the bank for the signature card, account agreement, or beneficiary designation on file. Do not rely on old conversations, online access, or the fact that someone helped with bills during life.

Why this step matters so much

Executors often feel pressure to act fast, especially when funeral costs, mortgage payments, or anxious relatives are in the background. But using the wrong account too soon can create a mess that takes months to clean up. Money may have to be traced, repaid, or explained to the court and other heirs.

One account can pass outside probate while another account at the same bank still belongs to the estate. That is why careful account-by-account review matters. If you need help organizing what must be disclosed to the court, our guide to listing bank accounts in Texas probate inventory documents explains how those accounts are identified and reported.

How to Open an Estate Bank Account in Texas

You may reach this stage and feel two things at once: relief that the court has finally appointed you, and anxiety about making a mistake with money that belongs to someone you love. That reaction is normal. Opening the estate account is often the first task that feels practical, but it also sets the tone for the rest of the administration. If you set it up cleanly, you make later questions from the court, creditors, and family members much easier to answer.

Start with court authority

A bank needs proof that you are the person legally allowed to act for the estate. In most testate estates, that proof is Letters Testamentary. In an intestate estate, or in some other situations, the court may issue Letters of Administration instead.

Those Letters work like your badge of authority. They tell the bank that you are not acting based on family agreement, a promise in the hallway, or a copy of the will alone. You are acting under court authority. Without that document, many banks will not discuss account access in any meaningful way.

You will also need an EIN, which is the estate’s tax identification number. The estate is now a separate financial entity for administration purposes, so the account should be opened in the estate’s name, not under your Social Security number.

Why the EIN matters

Executors are often surprised by this step. The deceased person had Social Security numbers, personal bank accounts, and a long financial history. Even so, after death, the estate needs its own identifier for tax reporting and banking.

That separation protects you.

If estate money flows through your personal account, even for a short time, it can look like you treated estate funds as your own. You may know you were only trying to pay a bill quickly. A beneficiary or creditor looking back later may see something very different. A separate estate account creates a clean paper trail from the start.

Banks commonly ask for:

- Certified Letters Testamentary or Letters of Administration

- The original death certificate

- Your government-issued ID

- The estate EIN

The account title will usually follow a format like Estate of [Deceased Name]. Ask the bank for its exact titling requirement, because even small wording differences can matter in its internal system.

A simple example

Suppose your mother had a checking account in her name alone, with no payable-on-death beneficiary. The court appoints you as executor. You obtain certified Letters Testamentary, apply for the EIN, and take those documents, along with the death certificate and your ID, to the bank. The bank opens a new account in the estate’s name, then transfers the funds from your mother’s frozen account into that estate account.

That transfer is more than paperwork. It shows where the money came from, who had authority to receive it, and where it is being held for debts, taxes, and eventual distribution. If you later need to categorize bank statements, that clean starting point saves time and reduces confusion.

Follow the order carefully

Families often feel pressure here. Mortgage payments are due. Funeral expenses may need reimbursement. Relatives may ask when funds will be available.

The safest order is still the same. Get appointed. Get the EIN. Open the estate account. Then move estate money through that account.

That sequence matters because probate is not only about gathering money. It is also about protecting everyone involved from avoidable disputes. If you pay expenses too early, from the wrong place, or without records, you can create suspicion among beneficiaries and problems if creditor claims later need to be handled in a specific order. A good overview of those issues appears in this Texas probate debts and taxes guide.

This video gives a helpful overview of the practical process many Texas families face:

What to bring and what to ask

Go to the bank with a narrow goal. Open the correct account. Confirm the bank’s release procedure. Get clear answers before you leave.

Bring a folder with originals and copies, then ask:

- What exact account title do you require?

- Do you need certified Letters dated within a certain time period?

- What is your procedure for transferring funds from the deceased person’s frozen account into the estate account?

- Will monthly statements and tax documents be issued in the estate’s name?

- Are there restrictions on checks, debit cards, or online access for fiduciary accounts?

That last question helps more than many executors expect. Some banks treat estate accounts differently from ordinary checking accounts, and you want to know those rules before a payment deadline appears.

Some executors also meet with counsel before the bank visit, especially if the estate includes business funds, family conflict, or heirs in different states. The Law Office of Bryan Fagan, PLLC handles Texas probate administration, including executor guidance on bank account setup and court compliance.

Using the Account Paying Debts and Keeping Records

The estate account is the family’s shared record of what came in, what went out, and why. If you treat it carefully from the start, you reduce the risk of confusion later, especially when relatives are grieving, worried, or already second-guessing each other.

What money should move through the estate account

Use this account as the estate’s central hub. Money that belongs to the estate should flow in. Approved estate expenses should flow out. That separation matters because mixing estate money with your own funds can create suspicion and make your accounting far harder than it needs to be.

Common deposits include funds released from probate assets, refunds owed to the estate, paychecks made payable to the estate, and proceeds from selling estate property. Keeping those transactions in one place gives you a clean paper trail. Later, if a beneficiary asks where the money went, you are not relying on memory during an already emotional time.

Pay debts carefully, not quickly

Executors often feel pressure to start paying bills as soon as mail begins arriving. Slow down enough to confirm what each bill is. Some claims are valid estate debts. Some are not. Some must be handled in a particular order under Texas probate law.

A practical way to think about it is this. The estate account is not a family checking account. It is a fiduciary account, which means every payment should answer three questions: What was this for? Was it proper to pay? Can I prove it?

Before money leaves the account, keep:

- The bill, invoice, or creditor claim that shows why payment is requested

- Proof of payment such as a canceled check, bank confirmation, or receipt

- The payment date and amount for your ledger

- Any notes from your attorney or court approval if the issue was disputed or unclear

If you want a practical overview of the order of claims and common tax issues, this guide to debts and taxes in Texas probate helps explain why one wrong payment can create problems for the estate and for you personally.

Good records protect more than paperwork

Texas probate requires an accurate inventory and accounting of estate property. Bank accounts and cash transactions are a major part of that picture. If records are incomplete, the court may ask questions, beneficiaries may lose trust, and routine administration can turn into an avoidable dispute.

Good bookkeeping lowers the temperature in the room. It gives family members something concrete to review instead of filling gaps with fear, grief, or assumptions.

A recordkeeping routine that works in real life

You do not need a complicated system. You need one you will consistently keep up with month after month.

Set aside time once each month and work through the same short checklist:

| Task | What to save |

|---|---|

| Review bank statement | Full monthly statement in PDF or paper form |

| Match each withdrawal | Invoice, receipt, or written explanation |

| Match each deposit | Copy of check, transfer record, or supporting letter |

| Update your ledger | Running balance and notes about purpose |

Many executors also create a simple folder for each month, either on paper or on a computer, so every statement and receipt stays together. If organizing transactions feels harder than the legal side, this practical guide on how to categorize bank statements can make the bookkeeping process easier to manage.

Be careful with reimbursements and executor compensation

This is one of the most common trouble spots.

You may be entitled to reimbursement for proper estate expenses or compensation as executor, depending on the will and Texas law. But the estate account is not a place for informal withdrawals, round-number transfers, or payments you cannot clearly explain later. Even honest mistakes can look improper when relatives see money leaving the account without supporting records.

If you pay yourself anything, make sure the basis for that payment is documented, allowed, and transparent. A clear paper trail protects you and helps keep family disagreement from turning into a court fight.

Key Insight When to Call a Probate Attorney

Key Insight: Managing an estate bank account correctly is about more than depositing checks and paying bills. It is how you carry out your loved one’s wishes, protect family relationships, and protect yourself from mistakes that can create personal liability.

A lot of executor work is manageable once the path is clear. Trouble starts when the estate looks simple on the surface, but one account, one disagreement, or one unpaid debt changes the picture. That is why legal help often makes the biggest difference before a problem grows.

An estate administration works a lot like caring for a house after a storm. If all you see is a few wet spots, you may be able to clean up and move ahead. If the foundation shifted, waiting usually makes the repair harder and more expensive. Probate problems can work the same way.

Situations that call for legal help sooner rather than later

Some warning signs deserve attention right away:

- Someone is contesting the will or questioning whether it is valid. That can affect who has authority to act and who should receive estate funds.

- The estate may owe more than it owns. Texas law sets rules for handling creditor claims, and paying the wrong bill first can create problems for the executor.

- Family members are already in conflict over inheritance, spending, account ownership, or whether money should pass outside probate.

- A bank account is connected to a business or sole proprietorship. Business income, expenses, taxes, and records often require added care.

- You live outside Texas. Local court procedures, filing requirements, and bank practices can be harder to handle from a distance.

- A minor, dependent, or incapacitated person has an interest in the estate. Those cases often involve added court oversight and stricter rules.

Even one of these issues can change your job from basic administration to legal risk management.

How a probate attorney helps

A probate attorney helps by spotting issues early, explaining what authority you have, and helping you avoid steps that are hard to undo. That may include reviewing account ownership, determining whether funds belong in the estate, responding to creditor issues, preparing court filings, and helping you communicate clearly with beneficiaries.

This matters for emotional reasons too. Grief can make ordinary decisions feel heavier. If relatives are suspicious or confused, even a small banking mistake can look like favoritism or misconduct. Clear legal guidance can lower that tension before it turns into a long family dispute.

Some families also realize, after going through a loss, that their own documents need attention. In that case, it can help to review your planning separately after the estate is under control, especially if this probate exposed gaps or unclear instructions.

Final Steps Distributing Assets and Closing the Estate

The last stage of probate often feels emotional in a different way. The urgent tasks are mostly behind you, but accuracy still matters. Before anything is distributed, the estate should be in a position where debts, approved expenses, and required filings have been handled.

Your final accounting should show what came into the estate account, what was paid out, and what remains for distribution. Beneficiaries should be able to follow the story of the estate from opening balance to final balance without guessing.

Once the estate is ready, you distribute the remaining funds according to the will or, if there is no will, according to Texas intestate succession rules under the Estates Code. After those distributions are complete, the estate bank account can be closed, and the necessary closing documents can be filed with the probate court so you can be discharged from your duties.

This closing step matters more than people realize. It is how you formally end your responsibility. Until the estate is properly wrapped up, loose ends can stay attached to you.

If you’re facing probate in Texas, careful handling of the estate bank account can make the process steadier, cleaner, and less painful for your family.

If you’re facing probate in Texas, our team can help guide you through every step, from filing to final distribution. The Law Office of Bryan Fagan, PLLC works with Texas families, executors, and heirs on probate administration, estate bank account issues, wills and trusts, guardianship matters, and probate disputes. Schedule your free consultation today.