Setting up a trust fund is a powerful way for Texas families to protect what they’ve built and ensure their wishes are followed, often without getting tangled up in the lengthy probate court process. It’s about creating a legal playbook that puts a trusted person—the trustee—in charge of managing your assets for the people you care about most, your beneficiaries. This gives you incredible control over your legacy while offering peace of mind.

Why Texas Families Choose Trust Funds Over Wills

When Texas families begin planning for the future, a will is often the first tool that comes to mind. While a will is an essential part of any estate plan, it’s not always the best tool for transferring assets smoothly. This is where understanding how to set up a trust fund becomes a game-changer, especially for those hoping to ease the burden on their loved ones.

In plain English, a will is a set of instructions for the probate court. After you pass away, your will must be legally validated, your debts settled, and only then is your property distributed to your heirs. This process, known as the Texas Probate Process, is public, can be slow, and is often stressful for a grieving family.

A trust, on the other hand, is a private legal arrangement you create to hold your assets. You appoint a trustee to manage everything for your beneficiaries according to your rules. Because the trust—not you—owns the assets, they generally sidestep the entire probate process when you die. This means a faster, more private, and often less contentious transfer of your legacy.

The Core Advantage: Avoiding Probate

For most families we work with, the primary reason they explore why to set up a trust is to stay out of the Texas probate system. Probate can freeze assets for months, sometimes even years, creating a real financial strain and emotional burden on loved ones.

Key Insight: A will is a ticket to probate court. A properly funded trust is a ticket around it. This single distinction is the most powerful reason families choose trusts to protect their privacy and streamline inheritance.

Trusts have become a go-to strategy for families nationwide. In the U.S., which oversees nearly half of the world's $28.6 trillion in regulated fund assets, savvy families use trusts to avoid the delays and costs of probate. While our focus is on Texas law, it helps to know this is a widely-used tool. You can explore the differences between living trusts and wills from a broader perspective to see how these concepts apply elsewhere.

More Than Just Asset Transfer

Beyond dodging probate, trusts offer a level of control that wills simply cannot provide. They give you a structured way to manage your legacy and protect your beneficiaries long after you're gone.

Here are a few common situations where a trust is the superior choice:

- Protecting Young Beneficiaries: You can structure the trust so a child receives their inheritance in stages—for instance, at ages 25, 30, and 35—rather than a large lump sum they may not be prepared to manage at 18.

- Providing for a Loved One with Special Needs: A Special Needs Trust can hold assets for a disabled family member without jeopardizing their eligibility for essential government benefits like Medicaid.

- Managing Complex Family Dynamics: In blended families, a trust can ensure your assets go to your children from a previous marriage while still providing for your current spouse during their lifetime. This is a common objective in many Wills & Trusts plans.

A trust isn't just a stack of legal papers; it's a carefully crafted plan that reflects your values and provides real, lasting security for the people you love. It’s a proactive step toward creating a legacy that is clear, private, and protective.

Understanding the Key Roles in Your Trust

When you set up a trust, you're not just signing a document; you're creating a private legal entity with a specific mission. To bring that mission to life, every trust needs a cast of key players, each with a distinct and vital role. Getting these roles right is the first step toward building a trust that truly works for your family.

At its core, every trust in Texas involves three fundamental parties, as defined in the Texas Estates Code:

- The Grantor (or Settlor): This is you—the person creating and funding the trust. You are the one who sets the rules, defines the goals, and places the assets into the trust's care.

- The Trustee: This is the manager you appoint to follow your instructions. The trustee has a fiduciary duty—a high legal standard requiring them to act solely in the best interests of the beneficiaries.

- The Beneficiary: These are the people or entities (like a charity) you want to benefit from the trust assets. They are the entire reason the trust exists.

Think of it like building a team. You're the owner and architect (the Grantor), you hire a responsible general manager (the Trustee), and the players who receive the benefits are your loved ones (the Beneficiaries).

The Critical Choice: Selecting Your Trustee

Of all the decisions you'll make, none is more important than choosing your trustee. This individual or institution will hold the legal and ethical responsibility to manage your assets and care for your beneficiaries according to your exact terms. It's a role of immense trust and responsibility, governed by the Texas Trust Code.

You generally have two options: an individual, like a family member or trusted friend, or a corporate trustee, such as a bank or trust company. Each path comes with significant pros and cons that demand careful thought.

A family member might know your loved ones personally and understand the family dynamics, which can be a huge plus. However, putting a sibling or child in charge can sometimes create unintentional conflict, especially when they have to make tough financial calls that affect other relatives.

A Real-World Scenario: Choosing Between Family and a Professional

Consider the Garcia family. Maria wants to set up a trust for her two adult children, Alex and Ben. Her first thought is to name Alex as the trustee since he’s responsible and has a good head for numbers. But Ben has struggled with managing his finances in the past. Maria's trust includes a "spendthrift" provision, giving the trustee discretion to distribute funds based on Ben's needs while protecting the principal from creditors or poor decisions.

By naming Alex as trustee, Maria would be placing him in the difficult position of having to say "no" to his own brother. This could strain their relationship for years to come. The emotional toll of managing a sibling's inheritance can be immense and often leads to disputes that end up in probate litigation.

After discussing this with her attorney, Maria realizes a neutral third party would be better. She opts for a corporate trustee from a local bank. This professional trustee can make objective decisions based on the trust's written rules, preserving the brothers' relationship while ensuring Ben is cared for exactly as Maria intended. This single decision removes the emotional burden from her children and ensures professional management of the funds. It's a crucial part of any well-thought-out Wills & Trusts plan.

Creating a Legally Sound Texas Trust Document

Once you've settled on the right type of trust and picked the people who will run the show, it's time to translate all those decisions into an official legal document. This isn't just paperwork—it's the actual legal foundation for your entire estate plan. While it’s tempting to use DIY legal websites to save money, we have seen them pave the way for future heartbreak and incredibly expensive legal battles for families down the road.

A trust document is a precision instrument, not a simple fill-in-the-blank form. It has to comply with the Texas Trust Code, found in Title 9 of the Property Code. A single misplaced word or a vaguely written phrase can create loopholes or, even worse, invalidate the entire trust. If that happens, your assets get thrown right back into the probate process you were trying so hard to avoid.

The Dangers of DIY Trust Creation

Creating a trust without a qualified attorney is a significant risk. Online templates are generic by nature. They cannot possibly account for your unique family dynamics, the nuances of Texas law, or the potential conflicts that could arise years from now.

We have had to clean up the mess from DIY documents more times than we can count. The most common mistakes we see are:

- Invalid Provisions: Wording that accidentally violates Texas law, making certain parts of the trust completely unenforceable.

- Ambiguous Instructions: Vague language about how and when to distribute assets, which is practically an invitation for beneficiaries to start fighting.

- Failure to Plan for Contingencies: No plan for what happens if a beneficiary dies, a trustee becomes incapacitated, or someone refuses their role.

These errors almost always lead to a judge getting involved. That means the trust's money gets drained by legal fees, all while your loved ones are dealing with profound stress during an already difficult time.

Crafting a Custom Plan with an Attorney

Working with an experienced Texas estate planning attorney is about building a trust document that is truly built to last. The same meticulous principles found in guides on how to draft contracts that actually work apply here, but with the added weight of your family's future. An attorney will walk you through the critical decisions that become the heart and soul of your trust.

This process is all about defining clear rules for every possible scenario. We'll nail down specifics, including:

- Distribution Standards: Will beneficiaries get funds only for specific needs, like health and education? Or will they receive set payments when they hit certain ages?

- Incapacity Clauses: We'll create crystal-clear instructions for how your finances will be managed if you ever become unable to make decisions for yourself.

- Special Protections: Including a spendthrift clause is a powerful tool. It can shield a beneficiary's inheritance from their creditors or protect it in a future divorce.

The need for properly structured trusts is growing, especially as financial pressures increase. For Texas seniors looking at Medicaid asset protection, the process starts with an attorney assessing net worth, followed by drafting a trust that is fully compliant with the Texas Trust Code. While small estate affidavits can work for estates under $75,000, trusts are far superior for larger portfolios. They give your executor immediate access to assets, completely bypassing the typical 6–12 month probate delay.

Key Insight: A professionally drafted trust is your voice, speaking with legal authority for your family when you no longer can. It anticipates challenges, prevents conflict, and provides a clear roadmap for your trustee to follow your exact wishes.

The differences between trust types have a massive impact on how these rules are written. For instance, exploring the nuances of a revocable trust vs. irrevocable trust is a crucial part of the drafting phase, as it affects everything from your taxes to asset protection.

Ultimately, investing in professional legal help is the single best way to ensure your trust delivers the peace of mind and protection your family truly deserves.

Step-by-Step Guide: How to Properly Fund Your Trust

Getting your trust document signed and notarized feels like crossing the finish line, but it’s actually just the starting line. We have seen the heartbreak firsthand: a family spends time and money creating the perfect trust, only to discover years later that it’s just an empty legal shell. An unfunded trust is like a safe with nothing inside—it can’t protect or distribute a single asset.

The process of moving your assets into the trust is called “funding,” and it's the single most important step in making your estate plan actually work. This is where your plan moves from paper to reality. It's what ensures your assets bypass probate and are managed exactly as you’ve laid out.

The Mechanics of Moving Assets

Funding a trust simply means retitling your assets from your individual name into the name of the trust. The exact steps, however, change depending on what you own.

- Real Estate: For your home or any other property, you'll need a new deed. This legal document officially transfers ownership from you to your trust. For example, the title would change from “John and Jane Doe” to “John and Jane Doe, Trustees of the Doe Family Trust.” This isn't just a simple form—it has to be prepared correctly and filed with the county clerk to be valid. You can learn more by reading our guide on how to change a deed on a house.

- Bank Accounts: Head to your bank. You’ll need to work with them to change the ownership on your checking, savings, and money market accounts. Sometimes this means opening new accounts in the trust’s name, but often you can just retitle the existing ones.

- Investment Accounts: If you have brokerage accounts with stocks, bonds, or mutual funds, your financial advisor can help. They’ll have the specific paperwork needed to transfer ownership over to the trust.

- Life Insurance and Retirement Accounts: This is a big one that people often get wrong. For assets like 401(k)s, IRAs, and life insurance policies, you generally do not change the ownership. Instead, you update the beneficiary designation forms to name the trust as the primary or contingent beneficiary. It's a critical and frequently overlooked detail.

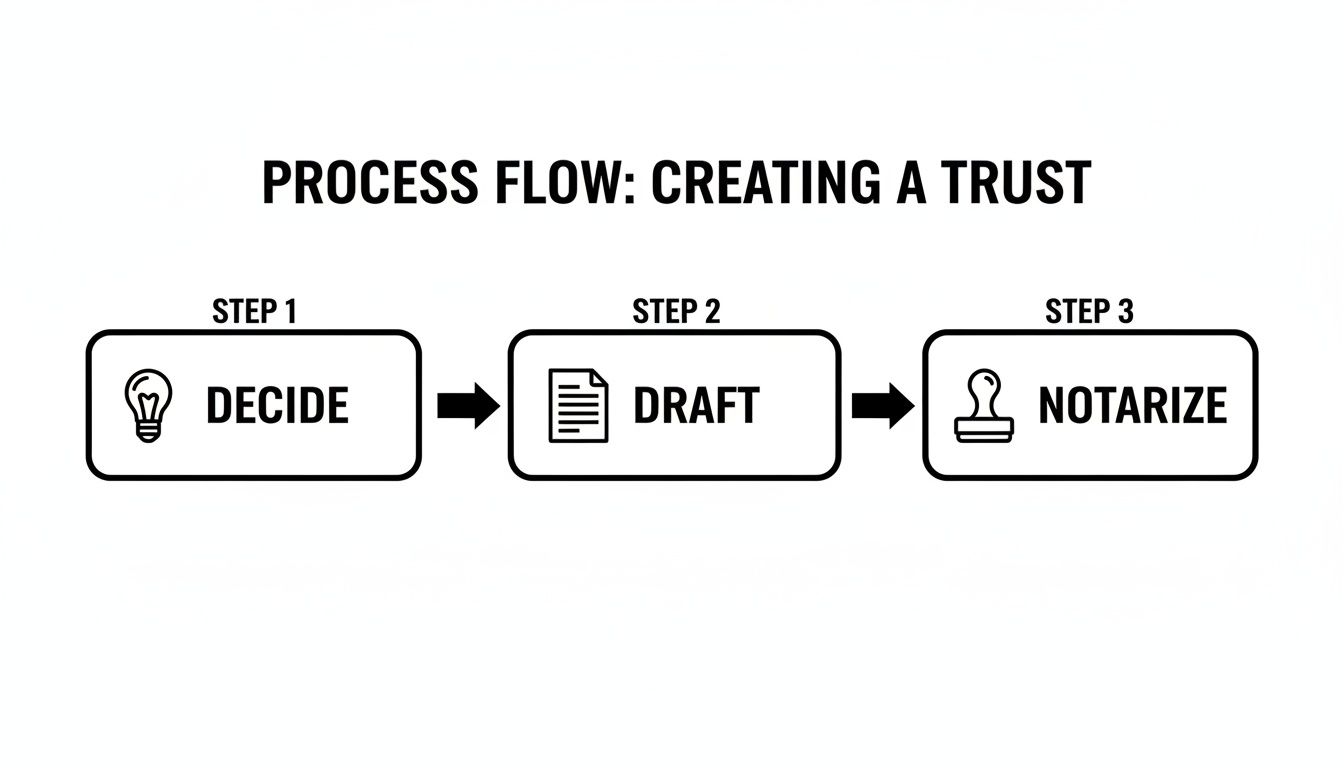

This whole process—decide, draft, notarize—is really just the setup for the most important part: funding.

This diagram lays it out perfectly. The real power of the trust is unlocked only after you take that final step of moving your assets into it.

To help you stay organized, here's a simple checklist for funding some of the most common assets.

Asset Funding Checklist for Your Texas Trust

| Asset Type | Action Required | Key Consideration |

|---|---|---|

| Real Property (Home, Land) | Prepare and record a new deed transferring the property to the trust. | The deed must be filed with the county clerk's office where the property is located. |

| Bank Accounts | Go to the bank to retitle accounts or open new accounts in the trust's name. | Bring a copy of your trust document or Certificate of Trust with you. |

| Non-Retirement Investments | Contact your brokerage firm to complete their transfer of ownership forms. | This applies to stocks, bonds, and mutual funds held in a taxable account. |

| Life Insurance | Update the beneficiary designation form to name the trust as a beneficiary. | Do NOT change the owner. This could have negative tax consequences. |

| Retirement Accounts (IRA, 401k) | Update the beneficiary designation form to name the trust as a beneficiary. | Consult an attorney; naming a trust as a retirement account beneficiary has complex tax rules. |

| Business Interests | Execute an "Assignment of Interest" or similar document for LLCs or partnerships. | Review the company's operating agreement for any restrictions on transfers. |

This checklist is a starting point. Every estate is different, so it's crucial to inventory all your assets and create a specific plan for each one.

Your Safety Net: The Pour-Over Will

Life gets busy. It’s incredibly easy to open a new bank account or buy a vacation property and completely forget to title it in the trust's name. This is where a special type of will, called a pour-over will, acts as an essential safety net.

A pour-over will is simple. It directs that any assets still in your individual name at the time of your death should be "poured over" into your trust. Now, it's not a perfect fix. Any assets caught by the pour-over will still have to go through probate. But, the will ensures they ultimately end up in your trust to be managed according to your wishes, rather than being divided up based on rigid state laws.

Takeaway: Your trust is only as strong as its funding. Think of the pour-over will as your backup plan, but diligent and complete funding is your primary strategy for ensuring your estate plan succeeds without court intervention.

Managing Your Trust for the Long Term

Getting your trust set up and funded is a huge accomplishment for your family’s future, but it's not a one-and-done deal. Think of a trust as a living document—it needs attention and proper care to do its job. This ongoing process is called trust administration, and it’s all about making sure your assets are protected and your wishes are followed, year after year.

While you're alive and well, you'll most likely be your own trustee. You’ll manage the assets just like you always have, with one small but crucial difference: the trust officially owns everything. The real test, however, comes when your successor trustee has to step in, either because you're incapacitated or after you've passed away.

The Successor Trustee's Core Duties

When your successor trustee takes the reins, they’re stepping into a role with serious legal and moral weight. The Texas Trust Code imposes a fiduciary duty on them, which is a plain-English term for one simple rule: they must act only in the best interests of the beneficiaries. It's not a suggestion; it's the law.

Their main responsibilities boil down to a few key jobs:

- Smart Investment Management: The trustee has to manage the trust’s assets responsibly. They don't need to be a Wall Street guru, but they must make sensible decisions to protect and grow the trust’s value. Often, this means hiring a financial advisor to help.

- Meticulous Record-Keeping: Every penny has to be accounted for. The trustee is required to keep flawless records of all income, expenses, distributions, and transactions. There’s no room for error here.

- Filing Tax Returns: A trust is its own legal entity, which means it often has to file an annual income tax return (Form 1041). The trustee is on the hook for making sure this gets done correctly and on time.

- Distributing Assets to Beneficiaries: This is where your instructions are everything. The trustee must follow the terms of your trust to the letter, paying out assets exactly as you directed.

This last point is where you can give your trustee—and your family—a true gift: clarity.

A Real-World Scenario: Navigating a Distribution Request

Let’s imagine your trust directs the trustee to make distributions for a beneficiary's "health, education, and support." One of your children comes to the trustee and asks for $25,000 to launch a new business, arguing it qualifies as "support."

If your trust document is vague, your trustee is now in a bind. Is a risky startup considered "support"? A poorly defined term is an open invitation for family conflict and could even drag the trust into expensive probate litigation if other beneficiaries disagree.

But a well-drafted trust provides clear guardrails. It might define "support" as covering reasonable living expenses like a mortgage or insurance but specifically exclude speculative business ventures. That simple definition empowers the trustee to make an objective, legally sound decision. It turns a potential family war into a straightforward administrative task, protecting the trustee from liability and keeping the peace.

Common Missteps in Trust Administration

Even a trustee with the best intentions can make some critical mistakes. Steering clear of these common pitfalls is vital for the health of your trust.

Key Insight: The single most damaging mistake a trustee can make is commingling funds. This means mixing their personal money with the trust's assets, like paying their own credit card bill from the trust bank account. It’s a massive breach of fiduciary duty that can trigger a legal and tax catastrophe.

Other frequent blunders include:

- Poor Communication: Keeping beneficiaries in the dark about the trust's finances and activities almost always breeds distrust and conflict.

- Favoring One Beneficiary: A trustee must be impartial. They have to treat every beneficiary fairly according to the rules you set in the trust.

- Delegating Improperly: While a trustee can (and should) hire experts like accountants or lawyers, they can't hand off their core decision-making duties. The buck stops with them.

Managing a trust is a serious job. Whether you're handling your own revocable trust today or grooming a successor trustee for their future role in a Guardianship or trust administration scenario, understanding these responsibilities is the key to making sure your legacy is secure.

Wrapping It Up: Your Final Act of Care

Setting up a trust fund in Texas is far more than just a smart financial move. It's a powerful, achievable way to protect your assets, provide for your family, and completely sidestep the public, often drawn-out probate court process. It’s about creating a private, crystal-clear roadmap for your legacy.

While the steps are logical, the nuances of Texas law—especially the specific rules found in the Texas Estates Code—make professional guidance a necessity. Working with an experienced estate planning attorney isn't just about getting documents drafted; it’s about ensuring your plan is legally bulletproof and actually does what you want it to do.

Think of your trust as the ultimate act of care for the people you love most. It provides them with clarity and security during an incredibly emotional time. It prevents the kind of family fights that can tear people apart and relieves your loved ones of unnecessary administrative headaches.

Takeaway: A well-crafted trust is more than a legal strategy. It's a deeply personal statement that organizes your affairs, protects your beneficiaries, and ensures your wishes are honored with precision and compassion.

By taking these steps now, you’re not just managing wealth—you’re securing your family’s future and giving everyone, including yourself, lasting peace of mind. The process itself is a gift to your loved ones, simplifying their lives when they need it most. This is the real purpose of thoughtful Wills & Trusts planning. The entire point is to avoid common disasters that derail an estate, like the family conflicts that so often explode into messy probate litigation.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.

Answering Your Questions About Texas Trusts

When families start exploring trusts, a lot of questions pop up. It's completely normal. Below, we’ve put together plain-English answers to some of the most common questions we hear from clients here in Texas. Our goal is to clear up the confusion so you can feel confident about your next steps.

How Much Does It Cost to Set Up a Trust Fund?

This is usually the first question on everyone's mind, and the honest answer is: it depends. The final cost really hinges on how complex your financial life is and what you need the trust to do. A straightforward revocable living trust is going to cost less than something highly specialized, like a trust designed for a family member with special needs.

You’ll see cheap templates online, and while they might seem like a bargain, they often create massive, expensive legal headaches down the road. Investing in a professionally drafted trust by an experienced Texas attorney isn't just a cost—it's an investment in your family's future security. Think of it as paying once for lasting peace of mind.

How Long Does the Process Take?

Most people are surprised to learn that setting up a trust is a much quicker process than they imagined. After an initial meeting where we map out your goals, the legal documents themselves can often be drafted and signed within just a few weeks.

The part that usually takes the most time is the funding process. This is where you actually retitle your assets—like your house, bank accounts, and investments—into the name of the trust. How long this takes depends on how many assets you have and how fast the different financial institutions move. With a little organization, the whole thing can be wrapped up in a matter of weeks, not months.

Can I Be My Own Trustee?

Absolutely. In fact, for a revocable living trust, this is the standard setup. As the creator of the trust (the grantor), you can also be the one who manages it (the initial trustee), so nothing changes in your day-to-day financial life.

You’ll also name a successor trustee—this can be a trusted person or a financial institution—who will step in to manage the trust if you become incapacitated or after you pass away. This structure gives you complete control during your lifetime and ensures a seamless, private transition when the time comes.

Is a Trust Better Than a Will?

This isn't really an "either/or" question. A trust and a will are different tools that do different jobs, and a solid estate plan almost always includes both. A will is basically your instruction manual for the Texas Probate Process. On the other hand, a properly funded trust is designed to keep your assets out of that court process entirely.

For most families, a trust is a far better tool for transferring assets. It’s private (unlike a will, which becomes public record), it’s efficient, and it gives you much more control over how and when your heirs receive their inheritance. A will simply can't protect you if you become incapacitated or let you set up staggered distributions for your beneficiaries the way a trust can.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.