Skip to content

Skip to content Yes, a properly structured and funded living trust is one of the most effective tools Texas families can use to completely avoid the probate process. This strategy lets your assets pass directly to your loved ones privately and efficiently, without ever needing a judge’s permission.

When you are grieving the loss of a loved one, navigating their final wishes should be a private, healing process, not a public legal battle. A trust helps ensure your family has the space to grieve without the added stress of court proceedings.

Why Texas Families Want to Avoid Probate

When a loved one passes away, the last thing your family wants is to get tangled up in a lengthy, expensive, and public court proceeding. But for many estates, that’s exactly what probate in Texas is—a major source of stress during an already heartbreaking time.

Understanding the Probate Process

In plain English, probate is the court-supervised legal process required to settle an estate after someone dies. A judge must first confirm that the deceased person’s will is legally valid. Then, the court oversees the payment of their outstanding debts and formally approves the distribution of the remaining assets to the rightful heirs.

While it serves a necessary purpose, it’s rarely a quick or simple journey. The process involves filing petitions with the court, attending hearings, notifying creditors, and creating detailed inventories of every asset. Every one of these steps is governed by the Texas Estates Code and becomes part of the public record, exposing your family’s financial affairs to anyone curious enough to look.

The True Costs of Probate in Texas

Many families are caught off guard by the real financial and emotional toll of probate. The expenses can pile up quickly, chipping away at the inheritance you worked so hard to leave behind.

Probate expenses can devour up to 10% of an estate’s total worth, covering court costs, attorney’s fees, appraisals, and executor payments. In Texas, where probate courts in bustling areas like Houston and Dallas are notoriously backlogged, proceedings often take 12-18 months on average, sometimes stretching to two years if disputes arise.

This is precisely where a living trust becomes an invaluable tool.

When you create a trust, you establish a private legal entity to hold your assets. Because the trust—not you personally—owns the property, there is nothing for the probate court to administer when you pass away. The transfer of assets happens according to your private instructions, saving your family precious time, money, and heartache. You can discover more about the specific advantages of setting up a trust in Texas in our detailed guide.

A living trust offers a compassionate alternative that prioritizes your family’s well-being. It provides a clear, private, and direct path for your legacy to continue without the delays and public scrutiny of the court system. For families seeking peace of mind, it is often the wisest choice.

Will vs. Living Trust At a Glance

To make the choice clearer, here’s a quick summary of how an estate with only a will compares to an estate with a properly funded living trust in Texas.

| Feature | Estate with Only a Will | Estate with a Living Trust |

|---|---|---|

| Probate Required? | Yes, almost always. | No, assets in the trust bypass probate. |

| Public Record? | Yes, all proceedings are public. | No, the process is completely private. |

| Cost | Often high due to court fees & attorney involvement. | Generally lower, avoids most court-related costs. |

| Timeline | 12-18 months on average, longer with disputes. | Weeks or months, depending on asset complexity. |

| Control After Death | The executor must follow court-supervised steps. | The successor trustee follows your private rules. |

| Asset Management | Court must appoint an executor to manage assets. | Successor trustee takes over immediately. |

| Contestability | Can be challenged in open court, creating delays. | More difficult to contest, offering greater security. |

This table highlights the core differences, showing why so many Texans are now turning to trusts to protect their families from the burdens of probate court.

How a Trust Keeps Your Estate Out of Court

So, how exactly does a trust manage to sidestep the entire probate system? The concept is actually far simpler than most people think. Think of a living trust as a private, legal container you create to hold your most important assets—your home, your bank accounts, and your investments.

While you’re alive and well, you have complete control over this container and everything inside it. You’re the one in charge. But when you pass away, your chosen successor simply takes over management and distributes the contents according to your private instructions, with no need for a judge’s permission. This is the core reason a trust avoids probate—it privatizes the transfer of your legacy.

The Magic of Ownership

The legal principle that makes a trust work so well is a simple change of ownership. When you move an asset into your trust, you are legally re-titling it. Your home is no longer owned by “Jane Smith,” but by “The Jane Smith Living Trust.”

Because the trust—a separate legal entity—owns the assets, there is technically nothing left in your personal name for a probate court to administer when you die. A will only controls assets you personally own. Since the trust owns the property, it falls completely outside the court’s jurisdiction, allowing your instructions to be carried out privately and immediately.

Understanding the Key Players in Your Trust

Legal concepts can feel overwhelming, especially when you’re dealing with the stress of planning for the future or grieving a loss. To simplify things, let’s break down the three essential roles involved in every Texas trust. In most cases, you’ll actually play all three roles yourself at the beginning.

- The Grantor (or Settlor): This is you, the creator of the trust. You set the rules, decide which assets go into the container, and name the people who will eventually benefit.

- The Trustee: This is the manager of the trust. While you’re alive, you are almost always your own trustee, which means you keep full control to buy, sell, or manage assets just like you always have. You’ll also name a Successor Trustee—a trusted person or institution—to take over when you pass away or become unable to manage your own affairs.

- The Beneficiary: This is the person or people who will ultimately receive the assets from the trust. During your lifetime, you are the primary beneficiary, using and enjoying your own property. After you pass, your loved ones (like your children or spouse) become the beneficiaries.

A Real-World Texas Scenario

Let’s put this into practice with a realistic example. Imagine a Houston family—let’s call them the Garcias—with a home in The Woodlands, a savings account at a local credit union, and some investments. Mr. and Mrs. Garcia create a revocable living trust and transfer the deed to their home and title to their bank accounts into the trust’s name. They name themselves as the initial trustees and their adult daughter, Sofia, as the successor trustee.

Years later, when the last parent passes away, Sofia doesn’t need to hire a probate attorney or file a single document with the Harris County court. As the successor trustee, she already has the legal authority to access the trust accounts, pay final expenses, and transfer the home’s title to herself and her brother—exactly as the trust document instructed. The entire process is private, efficient, and completely free from court interference. That is the peace of mind a well-prepared trust provides.

To learn more about how a trust can fit into a complete estate plan, explore our guides on Wills & Trusts and the Texas Probate Process.

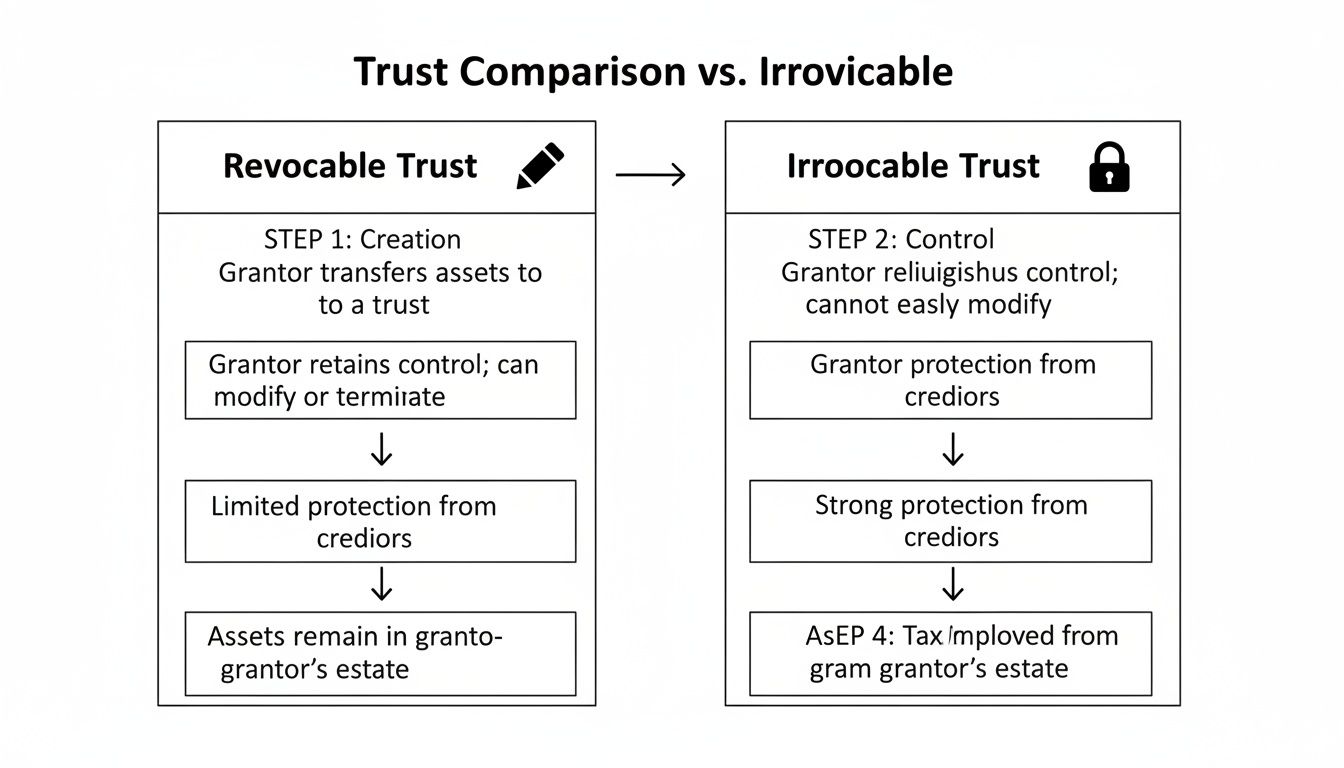

Choosing Between a Revocable and Irrevocable Trust

Once you realize a trust is the best way to keep your family’s legacy out of probate court, the next question is simple: which one is right for you? Not all trusts are created equal, and the best choice hinges entirely on your family’s unique goals, assets, and long-term vision.

For most Texas families, the decision boils down to two primary options: a revocable living trust and an irrevocable trust. Getting a handle on the fundamental difference between them is the key to making a confident and informed choice for your estate plan.

The Revocable Living Trust: Flexibility and Control

Think of a revocable living trust as a flexible blueprint for your estate. As its name suggests, it’s “revocable”—meaning you can change it, add to it, or even tear it up completely at any point during your lifetime, as long as you’re mentally competent. This level of control is precisely why it’s the go-to choice for the vast majority of families whose main goal is straightforward probate avoidance.

With a revocable trust, you keep complete authority over your assets. You can add new property, sell a car, or change who gets what whenever life happens—a marriage, a new grandchild, or a big financial shift. You serve as your own trustee, managing your affairs exactly as you always have.

This structure offers the perfect balance for most people: you get the powerful benefit of avoiding probate while sacrificing none of the control you have over your assets today.

The Irrevocable Trust: Asset Protection and Permanence

In sharp contrast, an irrevocable trust is a more permanent and rigid structure. Once you create it and transfer assets into it, you generally cannot make changes or take those assets back. This might sound restrictive, but this permanence is exactly what gives it power for more advanced estate planning goals.

Because you legally give up control and ownership of the assets placed inside, an irrevocable trust can offer significant benefits that a revocable one can’t. These advantages often include:

- Asset Protection: Shielding assets from future creditors or lawsuits.

- Estate Tax Reduction: Removing assets from your taxable estate to minimize potential federal estate taxes for high-net-worth individuals.

- Long-Term Care Planning: Helping to qualify for government benefits like Medicaid by reducing your countable assets.

An irrevocable trust is a specialized tool designed for specific, complex situations, such as those involving Guardianship for a loved one with special needs. It’s less about simple probate avoidance and more about sophisticated wealth preservation and protection strategies. To fully grasp the nuances, our firm has developed a detailed guide explaining the differences between a revocable vs. irrevocable trust that can provide even greater clarity.

Comparing Revocable and Irrevocable Trusts in Texas

Seeing the differences side-by-side can make your decision much clearer. This table highlights how each trust type operates, helping you align your goals with the right legal tool.

| Characteristic | Revocable Living Trust | Irrevocable Trust |

|---|---|---|

| Avoids Probate? | Yes, when properly funded. | Yes, when properly funded. |

| Can You Change It? | Yes, you can amend or revoke it at any time. | No, it is generally permanent once created. |

| Control Over Assets | Full Control. You remain in charge as the trustee. | No Control. You give up ownership to the trustee. |

| Creditor Protection | Limited. Assets are still considered yours. | Strong. Assets are generally shielded from creditors. |

| Estate Tax Benefits | No. Assets are still part of your taxable estate. | Yes. Can remove assets from your taxable estate. |

| Primary Goal | Probate avoidance and disability planning. | Asset protection, tax planning, and Medicaid planning. |

For most Texas families, the revocable living trust provides the ideal solution for ensuring a smooth, private, and efficient transfer of wealth to the next generation without the burdens of the probate court.

The Critical Step of Funding Your Trust

Creating a trust document is a fantastic first step, but it’s only half the journey. One of the most common and heartbreaking mistakes we see is when families sign the papers, file them away, and assume the job is done. It’s not.

Think of your trust like a secure, empty box you’ve built to hold your most valuable possessions. That box can only protect what you actually put inside it. The process of moving your assets into that box is called funding the trust, and it is without a doubt the most important action you can take to make sure your trust works the way it’s supposed to.

So, back to our original question: does a trust avoid probate? The answer is only yes if it has been fully funded. This means you have to formally transfer legal ownership of your assets from your own name into the name of the trust.

How to Properly Fund Your Trust

Funding isn’t just about making a list of assets in the trust document. It means actually changing legal titles and updating official records. The specific steps you’ll take depend entirely on the type of asset.

- Real Estate: For your home or any other property, this requires signing and filing a new deed that transfers ownership from “John and Jane Doe” to “The John and Jane Doe Revocable Living Trust.” This is a crucial step detailed in Title 2 of the Texas Estates Code.

- Bank Accounts: You’ll need to go to your bank and work with them to formally change the title on your checking, savings, and money market accounts to the trust’s name.

- Investment Accounts: Just like with bank accounts, any non-retirement brokerage accounts have to be re-titled into the name of the trust.

- Business Interests: If you own a piece of a partnership, LLC, or corporation, that ownership needs to be legally assigned to the trust using the proper documents.

This chart offers a simple visual breakdown of the two main types of trusts you might use in your plan.

The biggest takeaway here is that both types of trusts need meticulous funding to work, but they serve very different goals—one is about flexibility, the other is about long-term asset protection.

A Cautionary Tale: The Unfunded Trust

Let me share a true story we’ve seen happen more than once. A wonderful couple from San Antonio, we’ll call them Mark and Susan, spent the time and money to create a revocable living trust. They signed the documents, tucked them away in a safe, and felt a huge sense of relief, believing their estate was protected.

A few years later, Mark passed away suddenly. It was a tragedy. When Susan met with an attorney to sort things out, she made a devastating discovery: they had never actually transferred the deed to their family home into the trust. The house was still titled in their individual names, “Mark and Susan.”

Because the trust didn’t technically own the home, it became a probate asset. Susan had to go through the very public, lengthy, and expensive court process they had worked so hard to avoid. It added a mountain of stress during an already awful time.

The Importance of Organization and Professional Guidance

Properly funding a trust demands attention to detail and good record-keeping. As you move through the funding process, organizing important legal documents is key to ensuring a smooth transfer and preventing a critical oversight like the one Mark and Susan experienced.

The process can feel overwhelming, but you don’t have to go it alone. Working with an experienced Texas estate planning attorney isn’t just a good idea; it’s essential. A good lawyer doesn’t just draft the trust—they guide you through every single step of the funding process, from re-titling deeds to coordinating with your financial institutions. That hands-on help is what turns your trust from a piece of paper into a fully functioning tool that will actually protect your family and keep your legacy out of probate court.

When Your Trust Needs a Supporting Cast

A living trust is the heavyweight champion of probate avoidance in Texas. It’s powerful, effective, and can handle the bulk of your assets with privacy and efficiency. But even the star player needs a team. A trust doesn’t operate in a vacuum; to create a truly bulletproof estate plan, it needs to work in harmony with a few other essential tools.

Think of it this way: your trust is the main strategy, but certain assets are designed to follow their own special set of rules, bypassing both probate and your trust. Understanding how to coordinate all these moving parts is the key to making sure nothing falls through the cracks.

Assets That Already Have a “Skip Probate” Button

Some of your most significant assets come with a built-in feature to avoid probate: beneficiary designations. These are contracts that allow you to name a person who will receive the asset directly upon your death, no court required.

These are the most common ones:

- Retirement Accounts: Your 401(k)s, IRAs, 403(b)s, and other qualified plans all have beneficiary forms. When you pass away, the funds go straight to the person you named.

- Life Insurance Policies: The death benefit is paid directly to the beneficiaries listed in the policy. It’s a simple contract between you and the insurance company.

- Annuities: Just like life insurance, annuities have named beneficiaries who are contractually entitled to the remaining value.

- Payable-on-Death (POD) & Transfer-on-Death (TOD) Accounts: You can add these designations to most bank and brokerage accounts, turning them into assets that transfer automatically to a specific person.

Trying to move these assets into your trust while you’re alive can trigger disastrous tax penalties and completely undo their purpose. The best practice is to leave them in your name but to be absolutely religious about reviewing your beneficiary designations. Make sure they line up with your current wishes and don’t conflict with the goals of your trust.

The Pour-Over Will: Your Ultimate Safety Net

Life happens. Even with the best intentions, it’s remarkably easy to leave an asset out of your trust. Maybe you bought a piece of property and forgot to title it correctly, opened a new bank account on a whim, or inherited something unexpectedly. This is exactly why a pour-over will is non-negotiable.

A pour-over will is a special type of will that acts as your plan’s safety net. Its only job is to “catch” any assets that weren’t properly funded into your trust and “pour” them in after you die.

Now, it’s true that any assets passing through the pour-over will have to go through probate. But it’s a much simpler, more streamlined version. The will gives the court a single, clear instruction: move this asset into the trust. Once there, your private trust instructions take over. It’s the perfect backup plan to ensure that a minor oversight doesn’t derail your entire estate plan, which could lead to complex issues like Probate Litigation.

Why Every Plan Needs Both

Avoiding probate isn’t just a concern for the wealthy. Families with modest estates often fear the high costs of probate eating into their legacy, while high-net-worth families are more concerned about keeping their financial affairs private. The living trust is a solution that serves both groups.

In fact, one study showed that trusts are used by 77% of millionaires, but they are just as effective for any Texas family looking to protect assets like their home or retirement accounts. You can discover more about how families use trusts to avoid probate.

Here’s how the pieces fit together: Your trust is the core of the strategy, managing most of your assets privately. Your beneficiary designations handle specific accounts efficiently. And the pour-over will stands by as the ultimate failsafe. Together, they create a comprehensive system that shields your family from the costs, delays, and public scrutiny of probate court.

To learn more about how these essential documents work together, you can explore our guides on Wills & Trusts and see how a well-coordinated plan provides true peace of mind.

Takeaway

A properly funded living trust is the most powerful tool for Texas families who want to avoid probate. It allows your assets to be transferred to your loved ones privately, quickly, and cost-effectively, bypassing the court system entirely. However, a trust is not a standalone document. For complete protection, it must be paired with a pour-over will to catch any overlooked assets and regular reviews of beneficiary designations on retirement accounts and life insurance policies. This comprehensive approach provides true peace of mind and ensures your final wishes are carried out exactly as you intended.

Common Questions About Using a Trust to Avoid Probate

As you start thinking about setting up a trust, it’s only natural to have a few more questions pop up. Protecting your family’s future is a big deal, and you deserve to feel completely confident in your decisions. We hear these same questions from Texas families all the time, so let’s get you some clear, straightforward answers.

If I Have a Trust, Do I Still Need a Will in Texas?

Yes, absolutely. This is one of the most common misconceptions we see. Even with a perfectly funded trust, you still need a special kind of will called a pour-over will.

Think of it as a safety net. Its only job is to “catch” any assets you might have forgotten to put into your trust and then “pour” them in after you pass away. Without it, that forgotten bank account or piece of property gets stuck in the probate system, distributed according to state law—which may not be what you wanted at all. It’s a critical backup that makes sure your entire plan works the way you designed it.

How Much Does It Cost to Set Up a Living Trust?

While the upfront cost of creating a living trust is higher than a simple will, you have to look at the bigger picture. Probate can be shockingly expensive, often eating up 5-10% of an estate’s total value in court costs, attorney’s fees, and other administrative bills.

Setting up a trust now is a proactive investment. It can save your family a massive amount of money, not to mention the stress and time they would have spent dealing with the courts. You’re investing in peace of mind and preserving the legacy you worked so hard to build.

Can I Be the Trustee of My Own Revocable Living Trust?

Yes, and that’s how most people do it. When you create a revocable living trust, you almost always name yourself as the initial trustee. This is key because it means you keep full control over everything. You can still buy, sell, manage, and use your property exactly as you did before.

The trust document will also name a successor trustee. This is the trusted person or institution you’ve chosen to step in and manage the trust for your beneficiaries when you no longer can. This process for appointing trustees and successor trustees is outlined in Title 3 of the Texas Estates Code, ensuring a clear line of succession.

What Happens to My Debts if I Have a Trust?

A trust doesn’t make your debts vanish. Under the Texas Estates Code, your estate is still on the hook for settling any valid debts and final expenses after you’re gone.

Your successor trustee has a legal duty to use trust assets to pay off any legitimate creditors before distributing what’s left to your beneficiaries. This is a standard and necessary part of administering a trust, ensuring all your financial obligations are handled correctly. Planning with an experienced attorney ensures this process is managed efficiently and in full compliance with Texas law.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.