At its core, the difference between an irrevocable and a revocable trust boils down to one word: control. Making this choice for your family can feel overwhelming, but our goal is to offer clear, compassionate guidance. A revocable trust is your flexible friend, letting you make changes whenever life calls for it. An irrevocable trust is the opposite—it’s permanent, built to offer maximum asset protection for your legacy. Your decision depends on whether you value adaptability more than long-term, locked-down security.

Understanding Your Core Estate Planning Choices

When you start diving into estate planning in Texas, the terms “revocable” and “irrevocable” pop up everywhere, and they can sound intimidating. But the concept is straightforward. A trust is simply a legal arrangement where you (the grantor) hand over assets to a third party (the trustee) to manage for your loved ones (the beneficiaries). Think of it as creating a detailed rulebook for your property, ensuring your wishes are followed long after you’re gone, all while navigating the Texas Estates Code with care.

The real distinction between these two powerful tools comes down to how much control you’re willing to give up. A revocable trust, often called a “living trust,” is like a personal financial toolbox. You can add assets, remove them, switch out beneficiaries, or even dismantle the whole thing if your life circumstances shift.

It’s this flexibility that makes it so popular for Texas families. It’s a fantastic option for those who want to sidestep the headaches of the Texas Probate Process but still need the freedom to adjust their plans over time. To get a wider view on how this fits into your overall legacy, it’s helpful to explore some general estate planning considerations.

An irrevocable trust, on the other hand, is more like a secure vault. Once you place assets inside and set the rules, you can’t just make changes on a whim. This permanent nature is precisely its greatest strength, as it unlocks powerful benefits that a revocable trust simply can’t offer, especially for protecting assets or planning for long-term care.

Quick Comparison: Revocable vs. Irrevocable Trusts

To help you see the fundamental differences at a glance, this table breaks down how each trust operates in key areas. It’s a high-level overview of flexibility, protection, and tax implications, explained in plain English.

| Feature | Revocable Trust | Irrevocable Trust |

|---|---|---|

| Ability to Modify | Can be changed or canceled by you at any time. | Generally cannot be changed or canceled once created. |

| Asset Control | You retain full control over your assets. | You give up control of the assets to the trustee. |

| Probate Avoidance | Yes, assets in the trust bypass the public probate process. | Yes, assets in the trust also bypass probate. |

| Creditor Protection | No, assets are still considered yours and are vulnerable. | Yes, assets are generally protected from creditors. |

| Estate Tax Reduction | No, assets are included in your taxable estate. | Yes, assets are removed from your taxable estate. |

This quick comparison sets the stage. Now, let’s dig deeper into how each of these trusts really works and figure out which one might be the right fit for your family’s unique goals and circumstances.

Revocable Trusts: A Flexible Tool for Texas Families

A revocable living trust is often the cornerstone of modern estate planning, and for good reason—it’s all about adaptability. For many Texas families, this tool offers a practical way to manage assets, provide for loved ones, and maintain complete control over their financial lives, all with the peace of mind that comes from a well-laid plan.

Unlike its permanent counterpart in the irrevocable trust vs revocable trust debate, a revocable trust allows you, the grantor, to wear multiple hats. You can create it, manage it as the trustee, and even be a beneficiary. This means your relationship with your assets doesn’t really change; you can still buy, sell, or mortgage property just as you did before.

The primary motivation for most people creating a revocable trust is to avoid probate. By transferring your assets into the trust, you ensure they can pass directly to your heirs without getting tangled up in the public, often lengthy, and potentially expensive Texas probate process. This privacy and efficiency can be a great comfort to grieving families.

The Power of Control and Simplicity

With a revocable trust, you hold all the cards. You retain the power to amend its terms, change beneficiaries, or even dissolve it entirely if your circumstances change. A divorce, a new grandchild, or a significant change in assets can all be accommodated with a simple update. This flexibility is invaluable for families whose lives are still evolving.

However, this control comes with a trade-off. Because you still legally own and control the assets, they are not shielded from creditors or lawsuits. They are also considered part of your estate for tax purposes, meaning a revocable trust won’t deliver the same tax-reduction benefits as an irrevocable one. If you’re looking for more details, our firm has further explained the key benefits of a revocable living trust for Texas residents.

A Realistic Scenario: The Martinez Family

Let’s look at a common example. Consider a couple in San Antonio, Maria and David Martinez, who own their home and have a sizable investment portfolio. Their main goal is to ensure their two adult children inherit these assets quickly and without the stress of court proceedings after they’re gone.

- Step 1: Creating the Trust. They work with an attorney to create a revocable living trust document that outlines their wishes.

- Step 2: Funding the Trust. They then “fund” it by retitling their home and investment accounts in the name of the trust. This is a critical step.

- During Their Lifetime: Maria and David continue to live in their home, manage their investments, and can sell or change assets anytime. Day-to-day, absolutely nothing changes for them.

- After They Pass: Their designated successor trustee—their eldest daughter—steps in. Following the trust’s instructions, she can distribute the assets directly to herself and her sibling, completely bypassing the probate courts.

This straightforward process saves the family time, money, and the emotional strain of a public court case during a period of grief.

Takeaway

A revocable trust is not about surrendering control; it’s about reorganizing it. It provides a private and efficient roadmap for your assets to follow after your death, ensuring your wishes are carried out exactly as you planned. While it doesn’t offer the robust asset protection of an irrevocable trust, its simplicity and adaptability make it an essential tool for countless Texas families focused on smooth and private wealth transfer.

Irrevocable Trusts: Permanent Protection for Your Legacy

For Texas families and professionals who need the absolute highest level of asset protection, the irrevocable trust is a powerful, permanent solution. While a revocable trust offers flexibility you can change on a whim, an irrevocable trust is more like a vault—it’s built to safeguard your legacy from future unknowns. Giving up direct control can feel like a huge leap, but that’s the very step that unlocks its greatest strengths.

The concept behind an irrevocable trust is simple: once you move assets into it, you don’t personally own them anymore. This separation is everything. The assets are now owned by the trust itself and managed by an independent trustee you choose. It’s this structure that creates such a formidable shield against potential creditors, lawsuits, and other financial threats.

Unlocking Key Protections

By legally severing your ownership of the assets, an irrevocable trust achieves several critical goals that a revocable trust simply can’t. This makes it a vital tool when discussing irrevocable trust vs revocable options, especially for high-net-worth individuals or those in high-liability professions.

Here’s what it accomplishes in plain English:

- Creditor Protection: Since the assets are no longer yours, they are generally untouchable by future personal or business creditors.

- Estate Tax Reduction: The assets are officially removed from your taxable estate, which can dramatically lower or even eliminate federal estate taxes for very large estates.

- Medicaid Planning: It helps you qualify for long-term care benefits by reducing your countable assets over time.

While estate tax reduction gets a lot of attention, it is important to know that for 2024, the federal estate tax exemption is a substantial $13.61 million per person. The reality is that for the vast majority of Texas families, estate taxes are not a concern. This benefit applies to a very small percentage of the population, but for them, it is crucial.

Trustee Duties Under Texas Law

A common worry is losing control. But the trustee you appoint has a legal obligation, known as a fiduciary duty, to manage the trust’s assets exactly as you instructed. Under the Texas Estates Code, Title 2, they must act prudently, loyally, and always in the best interests of the beneficiaries you’ve named. Our guide on irrevocable trusts vs wills explained digs deeper into this relationship.

A Realistic Scenario: A Texas Business Owner

Let’s look at a real-world example. Imagine an Austin-based surgeon, Dr. Evans. She wants to guarantee her children inherit a significant portion of her wealth, but she’s rightfully concerned about potential malpractice lawsuits down the road.

- Step 1: Establishing the Trust. She works with an estate planning attorney to create an Irrevocable Life Insurance Trust (ILIT).

- Step 2: Funding and Management. She then transfers funds to the trust, and the independent trustee uses that money to buy a substantial life insurance policy.

What’s the result? The policy and its future payout are now owned by the trust, not Dr. Evans. They are completely shielded from any future legal claims against her and will pass to her children income-tax-free, outside of her taxable estate. This one strategic move ensures her family’s financial security, no matter what happens in her professional life.

Takeaway

An irrevocable trust isn’t about losing your assets. It’s about reassigning ownership to a secure legal entity that you created. You write the rulebook, and the trustee is legally bound to follow it for the benefit of your heirs.

Comparing Your Options: Control, Taxes, and Protection

Choosing between a revocable and an irrevocable trust boils down to a fundamental trade-off: do you want flexibility or do you want protection? There’s no one-size-fits-all answer. The right choice depends entirely on your family’s unique circumstances and what you hope to accomplish in the long run. We understand this can be a difficult decision, and we’re here to provide clarity.

To make an informed decision in the irrevocable trust vs revocable debate, you have to look past the basic definitions. Let’s break down how each trust performs in the three areas that matter most: control, tax implications, and asset protection.

Control and Flexibility

The most immediate difference you’ll feel is the level of control you keep over your assets. With a revocable trust, you are firmly in the driver’s seat. You can change the trust document, add or remove beneficiaries, sell property held by the trust, or even dissolve it entirely whenever you want. Life is unpredictable, and this adaptability allows your estate plan to evolve right along with you.

An irrevocable trust is built on the principle of permanence. Once you transfer assets into it, you give up direct control. You can’t just change the terms or take the assets back on a whim. This loss of control is precisely what gives the trust its powerful protective benefits.

Tax Implications

How each trust is treated by the IRS is another major fork in the road. For tax purposes, assets in a revocable trust are still considered yours. This means you’ll continue to report any income they generate on your personal tax returns. More importantly, those assets remain part of your estate for federal estate tax calculations when you die.

An irrevocable trust, on the other hand, is a separate legal and tax entity. When you move assets into it, you are effectively removing them from your taxable estate. For high-net-worth individuals, this strategy can create significant tax savings, preserving a larger legacy for their heirs. It’s a critical tool for anyone looking into how to minimize estate taxes in Texas and secure their family’s future.

Creditor and Asset Protection

This is where the distinction becomes most stark, especially for professionals in high-liability fields or business owners. A revocable trust offers zero asset protection from creditors or lawsuits. Because you maintain full control, the law sees the assets as your own, leaving them completely vulnerable to legal judgments.

An irrevocable trust provides a robust shield. Since the assets are no longer legally yours, they are generally protected from future personal creditors, business debts, and lawsuits. This protection is invaluable for anyone whose personal or professional life carries a higher risk of litigation.

Detailed Comparison: Revocable vs. Irrevocable Trusts

Here’s a comprehensive breakdown comparing the two trust types across the most critical decision-making criteria for Texas families.

| Decision Criteria | Revocable Trust (Living Trust) | Irrevocable Trust |

|---|---|---|

| Flexibility to Change Terms | High. You can amend, change beneficiaries, or dissolve it at any time. | Low. Terms are permanent once established. Changes are difficult and rare. |

| Control Over Assets | Full. You retain complete control as the grantor and often as the trustee. | None. You relinquish control to an independent trustee. |

| Probate Avoidance | Yes. Assets held in the trust bypass the probate process entirely. | Yes. Assets held in the trust bypass the probate process entirely. |

| Asset Protection | None. Assets are vulnerable to your creditors and lawsuits. | High. Assets are generally shielded from your personal creditors. |

| Estate Tax Reduction | No. Assets remain part of your taxable estate. | Yes. Assets are removed from your taxable estate, reducing potential taxes. |

| Medicaid Planning | No. Assets count toward your eligibility limits. | Yes. Can be used to protect assets for long-term care eligibility (with a look-back period). |

| Income Tax Reporting | Reported on your personal tax return (Form 1040). | Reported on a separate trust tax return (Form 1041). |

| Best For | Individuals wanting to avoid probate while maintaining control over their assets. | Individuals seeking maximum asset protection and estate tax reduction. |

This table highlights the core trade-offs. The path you choose depends on whether your priority is maintaining control today or securing protection for tomorrow.

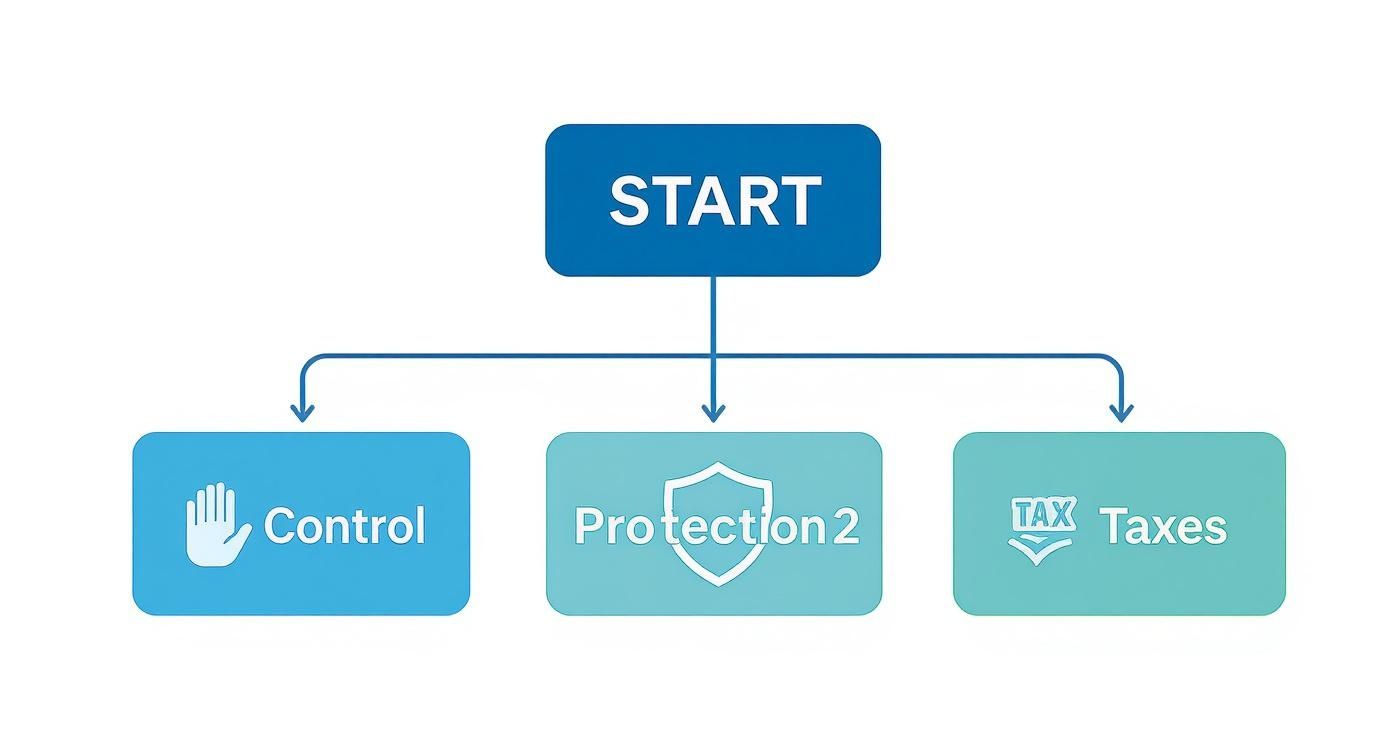

How to Choose the Right Trust for Your Situation

Choosing between a revocable and an irrevocable trust isn’t about picking the “best” one—it’s about matching the tool to your specific life goals. This is a personal decision that hinges on what you want to accomplish with your assets, both now and for future generations.

For many families in Texas, the main objective is straightforward: keep their estate out of the public and often drawn-out Texas Probate Process. If that’s your primary goal, and you want to keep total control over your property with the ability to change your mind at any time, a revocable trust is almost always the right call. It gets the job done efficiently while leaving you firmly in charge.

On the other hand, if your needs are more complex, an irrevocable trust becomes an essential strategy. This is the path for professionals in high-liability fields, anyone planning for future long-term care needs, or high-net-worth families looking to minimize estate taxes.

Key Questions to Ask Yourself

To cut through the noise in the irrevocable trust vs revocable debate, ask yourself these direct questions. Your answers will immediately point you in the right direction.

- Is maintaining 100% control over my assets my top priority? If yes, a revocable trust is your answer.

- Am I concerned about shielding my assets from future lawsuits or creditors? The protection of an irrevocable trust is a huge advantage here.

- Is reducing my family’s potential estate tax burden a major goal? An irrevocable trust is the only tool that can do this.

- Do I foresee needing to qualify for long-term care benefits like Medicaid? An irrevocable trust is a cornerstone of this kind of planning.

- Do I need the freedom to change beneficiaries or update terms as my family’s circumstances change? The flexibility of a revocable trust is what you need.

This decision tree visualizes how your main objective—be it control, protection, or tax savings—steers the choice.

As the flowchart shows, it really comes down to what you’re trying to solve. If you prioritize control, the path leads to a revocable trust. If asset protection or tax planning is paramount, an irrevocable trust becomes the necessary instrument.

Takeaway

The decision between a revocable and irrevocable trust isn’t a legal puzzle; it’s a reflection of your life’s priorities. One prioritizes your control during your lifetime, while the other prioritizes the permanent protection of your legacy for the future. Thinking through these questions will set you up for a productive conversation with an experienced estate planning attorney who can help you make the best choice for your family.

Final Thoughts for Texas Families

When it comes to your family’s future, choosing a trust is a serious decision. The whole irrevocable trust vs revocable debate boils down to one simple trade-off: do you need flexibility, or do you need permanent protection? One isn’t better than the other; the right choice is the one that fits your life, your goals, and your family’s unique situation with compassion and foresight.

For most Texas families, a revocable trust is the perfect tool. Its main job is to help you sidestep the headaches and costs of the Texas Probate Process. You stay in the driver’s seat, free to change your mind, update beneficiaries, or even undo the whole thing as your life changes.

On the other hand, an irrevocable trust is built for powerful, long-term security. It’s the right move for people who need to shield assets from creditors, plan for Medicaid eligibility down the road, or manage a large estate tax bill. The catch? You have to give up control. But in exchange, you get a powerful fortress around your legacy.

Your Personal Estate Planning Compass

So how do you decide? It all comes down to what you value most. If you can’t imagine giving up control and want the freedom to adapt your plan, a revocable trust is your answer. But if your top priority is locking down your assets against future threats, then an irrevocable trust offers the heavy-duty defense you’re looking for. This isn’t just about legal documents; it’s about building a foundation for your family’s security.

With a clear understanding of these differences, you can move forward with confidence. The next step is to talk through your specific situation with a legal professional who can translate your goals into a solid plan, whether that means setting up Wills & Trusts or establishing a Guardianship for a vulnerable loved one.

Every family has a unique story, and every story calls for a unique plan. We’re here to listen to yours and provide the guidance needed to protect everything you’ve worked so hard to build.

Takeaway

Estate planning isn’t a one-size-fits-all deal. Your decision between a revocable and irrevocable trust should be a direct reflection of your priorities—a balance between today’s need for control and tomorrow’s need for protection.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.

Common Questions About Texas Trusts

Diving into the world of estate planning always brings up a few questions. When it comes to picking between a revocable and an irrevocable trust, most Texas families run into the same practical concerns. Here are some straightforward, plain-English answers to the questions we hear most often.

Can I Have Both a Revocable and an Irrevocable Trust?

Yes, absolutely. A solid estate plan isn’t about picking one tool from the toolbox; it’s about using the right combination to get the job done. You are not limited to just one type of trust.

Think of it this way: Many people use a revocable trust as the main engine of their estate plan—it’s flexible, avoids probate for most assets, and keeps them in control. Then, they might set up a separate irrevocable trust for a very specific purpose, like shielding a family business, holding a large life insurance policy, or protecting assets for a child with special needs. This hybrid approach gives you flexibility for your everyday assets and ironclad protection for your legacy assets.

What Happens if I Put My Home in a Revocable Trust?

This is one of the most common and effective strategies for making sure your home bypasses the probate process. From a day-to-day perspective, you won’t notice a thing.

- You stay in control: You can still live in your home, sell it, or refinance it just like you always have. Nothing changes about your control.

- Property tax benefits are safe: In Texas, moving your home into a revocable trust generally does not affect your homestead exemption.

- A seamless transfer later: When you pass away, the home goes directly to the beneficiaries you named in the trust, no court dates required.

The trust simply becomes the new titleholder on paper. For your loved ones, this small step now makes a world of difference during a tough time later.

How Do I Fund a Trust in Texas?

“Funding” is just the legal term for moving your assets into your trust’s name. It’s the most critical step in the entire process. An unfunded trust offers zero benefits—it’s like having a car with no engine. Here is a step-by-step overview of what to expect:

- Step 1: Real Estate. An attorney prepares and files a new deed with the county clerk, officially transferring the property from your name to the trust’s name.

- Step 2: Bank Accounts. You’ll work with your bank to retitle your checking and savings accounts into the name of the trust.

- Step 3: Investment Accounts. The same process applies to your brokerage and other investment accounts—the ownership needs to be formally updated.

- Step 4: Life Insurance & Other Assets. You can choose to name the trust as the beneficiary of your policy, which can be a powerful move for managing the payout. Other assets like vehicles or business interests may also need to be transferred.

Because getting the titling right is so crucial under the Texas Estates Code, this is not a DIY project. Working with an experienced attorney ensures every single asset is funded correctly, activating the full power and protection of your estate plan.

Takeaway

A trust is just a piece of paper until you “fund” it by legally transferring your assets into its name. This is the crucial step that makes the entire plan work, ensuring your wishes are carried out and your loved ones are protected.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.