Skip to content

Skip to content Being named an executor is a profound act of trust, but it often comes with a wave of confusing and demanding responsibilities—especially during an already difficult time. In Texas, one of the most critical parts of this role is accounting for the estate’s finances. We understand that this task can feel overwhelming while you're grieving. This guide is designed to provide clear, step-by-step guidance to help you navigate your duties with confidence and care. This isn't just about bookkeeping; it's a fundamental commitment to transparency and fairness for everyone involved.

Your Core Duty: The Executor's Responsibility to Account

When a loved one names you as the executor of their Wills & Trusts, they're not just asking you to handle their final affairs—they're placing their complete faith in you. This role comes with what the law calls a fiduciary duty. In plain English, this means you must act with the highest degree of loyalty and good faith, always putting the interests of the estate and its beneficiaries first.

A huge piece of that duty is creating a clear, honest, and detailed record of the estate’s finances. It’s best to think of an estate accounting not as a burden, but as your legal shield. It’s the formal report that proves every dollar that came in, every bill that was paid, and exactly what’s left to be distributed to the heirs.

Why Is an Accounting So Important?

Properly handling the executor accounting requirements in Texas protects you from personal liability while making sure everyone is treated fairly. When beneficiaries start asking where the money went—and they often do—a well-prepared accounting provides definitive answers, shutting down misunderstandings before they can escalate into bitter family disputes and probate litigation.

The Texas Estates Code (specifically Titles 2 and 3) lays out specific rules for this process, but they're manageable if you know what to expect. This duty really boils down to a few key steps:

- Creating a Starting Point: The whole process kicks off with a detailed inventory of all estate assets.

- Tracking All Activity: You must meticulously log every single financial transaction, from income received to expenses paid out.

- Communicating with Beneficiaries: Keeping the heirs in the loop is absolutely vital for maintaining trust throughout the Texas probate process.

- Preparing a Final Report: Before you can close the estate, you’ll almost certainly need to prepare a final accounting that neatly summarizes your management of the assets.

Takeaway: The duty to account is about more than just numbers—it's about honoring the trust placed in you. A detailed accounting is your best defense against potential claims and the clearest way to demonstrate you have managed the estate responsibly and ethically.

While the requirements might feel intimidating, especially while you're grieving, they are designed to create an orderly and transparent process. We get the emotional weight of this responsibility. Our goal is to break down each step, giving you the clarity and support you need to handle your duties with confidence.

The Foundational First Step: Creating the Estate Inventory

Every single probate accounting starts with one absolutely critical document: the Inventory, Appraisement, and List of Claims. Think of it as the official starting line for the entire estate. It’s a detailed snapshot of everything the person owned—and owed—on the exact day they passed away.

Getting this document right is the bedrock of a smooth probate process. Without a clear and accurate inventory, everything that follows becomes more complicated, from paying debts to distributing assets to the heirs.

We get it. Cataloging a lifetime of belongings is an emotionally draining job. You’re not just listing items; you’re handling memories. But as the executor, this is one of the most important duties you'll perform, creating the baseline against which every future transaction will be measured.

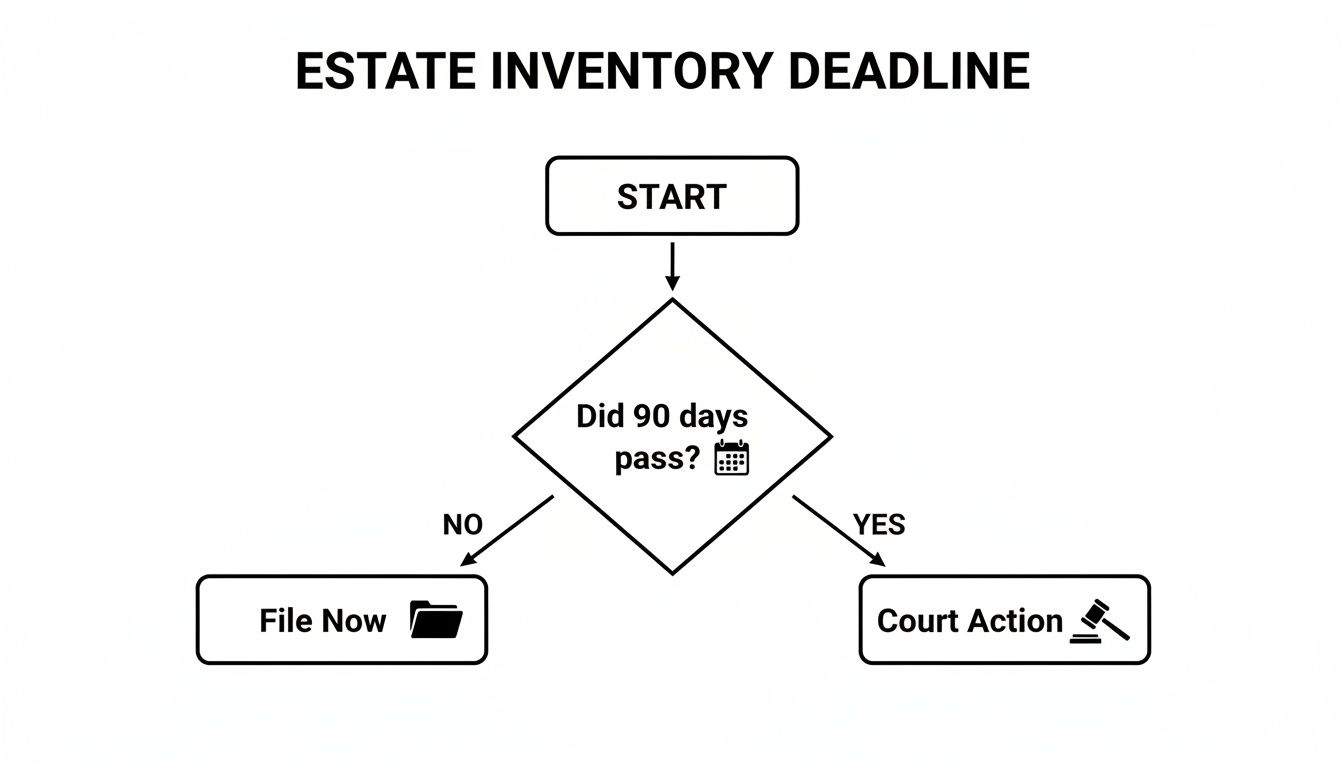

The Strict 90-Day Deadline

Here's something you can't ignore: the clock starts ticking immediately. The Texas Estates Code is crystal clear on this point. Under Section 309.051, you are required to prepare and file the complete Inventory with the probate court within 90 days from the date your Letters Testamentary were issued.

This isn't a suggestion; it's a firm legal deadline.

Missing it can stall the entire probate, and you’ll likely find yourself explaining the delay to a judge. The court takes this deadline seriously because a timely inventory protects everyone involved—you, the creditors, and the beneficiaries—by creating a transparent record from day one.

What Goes Into the Inventory?

So, what exactly needs to be on this list? The short answer is: everything. Your job is to create a thorough catalog of every asset the decedent owned, along with its fair market value on the date of their death. This includes:

- Real Estate: The family home, rental properties, or any other land located in Texas.

- Bank and Financial Accounts: All checking and savings accounts, CDs, money markets, and brokerage accounts.

- Vehicles: Every car, truck, boat, or RV, complete with its make, model, year, and VIN.

- Personal Property: This covers valuable items like jewelry, artwork, antiques, and high-end furniture.

- Other Assets: Things like stocks, bonds, mineral rights, business interests, and life insurance policies that are payable to the estate itself.

Key Insight: This isn't just about making a list. It’s an official valuation. You’ll need to determine the "fair market value" for each asset. For things like real estate, art, or a family business, this will almost certainly mean hiring a professional appraiser.

This detailed inventory sets the stage for every other accounting task you'll handle. For a moderately complex estate, it’s not uncommon to spend 20-35 hours just preparing and verifying the inventory, which is exactly why you can’t afford to wait. You can find more detailed guidance on how to make an itemized inventory for probate in Texas in our dedicated article.

Ultimately, the care and precision you invest in this first step will pay off throughout the entire administration. A clean, accurate, and timely inventory builds trust with the beneficiaries and gives you a clear road map for managing the estate. It makes for a smoother, more transparent process for everyone.

Independent Versus Dependent Administration: How Your Duties Change

In Texas probate, your job as an executor will look dramatically different depending on one single factor: are you an independent executor or a dependent administrator? This isn't just a title—it completely changes your day-to-day responsibilities, the level of court oversight you'll face, and most critically, your accounting requirements.

Think of it this way: an independent administration is like being handed the keys to a car with a map and a destination. The court trusts you to get there on your own. A dependent administration is like having a driving instructor in the passenger seat, requiring you to get permission before you even touch the gas pedal.

The path you're on dictates everything. Understanding which one applies to you is the first and most crucial step.

The Freedom of an Independent Administration

Most estates in Texas are handled through an independent administration, especially when the person who passed away left a will specifically asking for it. This process is designed to be faster and less expensive by granting the executor significant freedom from court interference.

As an independent executor, you won’t have to file routine reports with the court or get a judge's permission every time you need to sell property or pay a bill. It's a much more efficient route.

But don’t mistake freedom for a free-for-all. This autonomy comes with immense responsibility. You still have a strict fiduciary duty to manage the estate’s money with extreme care. Every single dollar must be tracked, because while you don't report to the court, you are absolutely accountable to the beneficiaries.

You can learn more about the specifics of this process in our deep dive on independent administration in Texas.

The Strict Oversight of a Dependent Administration

A dependent administration is the complete opposite. It’s a formal, court-supervised process where you, the administrator, must get a judge’s signature for nearly every action—from paying a simple utility bill to selling the decedent's home.

This path is more time-consuming and often more expensive. It’s typically required when there’s no will, the will doesn’t name an independent executor, or there’s a high potential for family conflict that the court needs to manage. This level of supervision is sometimes also used in Guardianship cases.

The cornerstone of a dependent administration is the annual accounting. Under Texas Estates Code Section 359.001, you are legally required to file a detailed, verified report with the court every 12 months until the estate is finally closed. This isn’t a simple summary; it's an exhaustive financial statement.

Accounting Duties: Independent vs Dependent Administration

| Requirement | Independent Administration | Dependent Administration |

|---|---|---|

| Court Reporting | No routine reports required. Accounting is provided to beneficiaries only upon request after 15 months. | Annual accounting must be filed with the court every 12 months. |

| Record-Keeping | Must keep meticulous records for beneficiaries. | Must keep meticulous records for court review and approval. |

| Transaction Approval | No court approval needed to pay bills, sell assets, or make distributions. | Must get court approval for almost every transaction. |

| Accountability | Accountable directly to beneficiaries. | Accountable directly to the probate court judge. |

| Final Closing | Can close the estate informally once all debts are paid and assets are distributed. | Must file a final account for court approval to officially close the estate. |

This table makes it clear: while both roles demand careful record-keeping, the audience and the frequency of your reporting are worlds apart. One answers to the family, the other answers to the judge.

No matter which type of administration you're in, some deadlines are non-negotiable from the very beginning.

As this visual shows, the 90-day clock for filing the initial Inventory, Appraisement, and List of Claims is a critical first step. Missing this deadline triggers immediate court action, setting a tough precedent for the rest of the probate.

In a dependent administration, your annual accounting is a serious undertaking. It must include:

- A complete list of all estate property you're managing.

- A detailed history of every transaction, showing all money received and all money paid out.

- The current status of all creditor claims—which were approved, which were rejected, and which are pending.

- The exact cash balance on hand and where those funds are held (e.g., which bank).

- A statement on the estate's tax status, including property and income taxes.

Key Insight: Whether your path is independent or dependent, the core duty is identical: meticulous record-keeping. The only real difference is who you have to show your work to—the court or the beneficiaries. Mismanage those records in either scenario, and you could be held personally liable for any shortfalls.

Knowing which type of administration you’re in is step one. It defines your roadmap for the entire probate journey and sets the rules for how you’ll account for every penny.

When a Beneficiary Can Demand an Accounting

When you’re an executor in an independent administration, the court largely takes a hands-off approach. It's a system built on trust—trust in you to manage the estate responsibly. But that freedom doesn't mean you're operating without oversight. The real check and balance comes from the beneficiaries, who hold a powerful legal right to know what's happening with the money.

Understanding when a beneficiary can formally demand an accounting is one of the most critical parts of your job. These timelines aren't just arbitrary rules; they're guardrails designed to manage expectations and keep communication clear. Get this right, and you can sidestep the kind of misunderstandings that tear families apart during an already difficult time.

The 15-Month Waiting Period

So, when can a beneficiary put you on the spot? Not on day one. The Texas Estates Code gives you a runway to get your work done before you have to produce a full, formal accounting. Beneficiaries can't just demand a detailed report on a whim.

The law is clear: Texas Estates Code Section 404.001 states that an "interested person" (which includes beneficiaries) can demand an accounting only after 15 months have passed from the date the will was admitted to probate and you received your Letters Testamentary.

Think of this 15-month window as your breathing room. It’s designed to be fair. It gives you the time you need to tackle the big, upfront tasks—finding and securing assets, filing the inventory, notifying creditors, and paying the estate’s initial bills—without someone looking over your shoulder every five minutes.

The Executor’s 60-Day Response Window

Once that 15-month mark passes, the ball is in the beneficiary's court. They can send you a formal, written demand for an accounting. And the moment you receive that letter, a new clock starts ticking—this one for you.

You have exactly 60 days to provide a complete and accurate accounting to the beneficiary who requested it. This isn't a suggestion; it's a hard deadline. Missing it can land you in serious legal hot water.

In fact, industry data shows that a staggering 40% of estate disputes in Texas boil down to poor communication and delays in providing financial information. If you blow past that 60-day window, the beneficiary can sue to compel the accounting. A judge can then order you to produce it, and you might find yourself paying for the legal fees out of your own pocket. Find out more about what happens when accounting demands are enforced at 1stestateplanning.com.

Key Insight: These deadlines aren’t meant to be threats; they’re tools for structured communication. The 15-month period protects you from premature demands, while the 60-day window protects the beneficiaries' right to information. Sticking to them is the best way to avoid ending up in probate litigation.

When a beneficiary finally makes that demand, think of it as an audit. Your financial stewardship of the estate is being put under a microscope, measured against standards similar to formal auditing and compliance standards. The best defense is a good offense. Keep meticulous records from the very beginning. If you track every dollar in and every dollar out, a demand for an accounting becomes a simple exercise in compiling information you already have, not a mad scramble to justify your actions.

What Every Formal Texas Estate Accounting Must Include

When a court or a beneficiary demands a formal accounting, they’re not asking for a simple summary. This is a detailed, legally formatted report that needs to be verified and sworn to. It's a high-stakes document where ballpark figures and guesswork have no place—absolute precision is the only option.

Fortunately, you don't have to guess what's required. The Texas Estates Code gives you a clear road map. Think of it as telling the financial story of the estate, complete with a beginning, a middle, and an end. Getting these pieces right isn't just about following the rules; it's about fulfilling your legal duty and protecting yourself from personal liability.

1. Property That Came Into Your Hands

The first part of your accounting picks up where the estate’s Inventory, Appraisement, and List of Claims left off. This document establishes the starting point for your financial story. You must list every single piece of property you've taken control of as executor since the administration began.

This means everything you cataloged at the outset—cash in the bank, real estate, cars, stocks, and personal items. It also includes anything that came in after you filed the initial inventory, like a surprise tax refund check or a life insurance payout that was delayed.

2. The Disposition of Property

Once you’ve shown what the estate started with, you have to explain what happened to it. This section details the disposition of any property that is no longer part of the estate. In plain terms, this means accounting for any asset that was sold, distributed, or otherwise disposed of.

It covers a lot of ground:

- Property Sold: If you sold the decedent's house or liquidated a stock portfolio, you need to show the date of the sale and the exact amount you received.

- Property Lost or Destroyed: Sometimes, tragedy strikes. If an uninsured asset was destroyed in a fire or flood, for example, it must be reported here.

- Property Distributed: If the court allowed you to make any early or partial distributions to beneficiaries, those transfers must be accounted for.

This part of the report creates a crystal-clear paper trail, showing everyone exactly why and how an asset left the estate. It's especially critical for building trust when major assets like a family home are involved.

Key Insight: Think of your accounting like a bank statement. You start with an opening balance (the inventory), and then you systematically list every single transaction—both credits and debits—to arrive at your closing balance.

3. All Money Received and Paid Out

This is the heart and soul of your accounting—the detailed ledger of every dollar that flowed in and out of the estate. Sloppy record-keeping here is the number one reason executors get into trouble, sparking ugly disputes and even personal liability.

Having a basic grasp of how financial transactions are tracked can make this process much smoother. If you're new to this, a resource on double-entry bookkeeping can give you a solid foundation for keeping things straight.

Your report must meticulously break down:

- Receipts: Every source of income must be listed. This includes interest earned on bank accounts, stock dividends, rent collected from property, and, of course, the proceeds from any assets you sold.

- Disbursements: Every penny paid out needs to be documented. This includes funeral costs, payments to creditors, attorney’s fees, court filing fees, and even the utility bills for the decedent's home.

Realistic Scenario: Let’s say you're the executor for your mother's estate. You would list the $150,000 you received from selling her stock portfolio as a receipt. Then, you would list each payment as a separate disbursement: the $12,000 funeral bill, a $3,500 payment to her last credit card, and every $250 electric bill you paid to keep the lights on until her house sold. Each one gets its own line item, supported by a receipt or statement.

4. Who Is Entitled to the Estate

This next part is straightforward but absolutely vital. You must list the full names and current addresses of every person legally entitled to receive property from the estate. These are the beneficiaries named in the will or, if there was no will, the heirs determined by state law.

This step serves as a final confirmation for the court, showing that you know exactly who the rightful recipients are before you make the final distributions.

5. Property Remaining in the Estate

Finally, your accounting must wrap up with a detailed list of all property still in your possession. This is your "on hand" balance. It shows what’s left to be distributed to the beneficiaries after all debts, taxes, and administrative expenses have been taken care of.

This isn’t a general summary. You need to be specific. List the exact cash balance in the estate's bank account, describe the vehicle that's left, itemize the jewelry, and identify the real estate. This final piece of the puzzle gives everyone a complete picture of what they will receive, ensuring the Texas probate process can close with total transparency.

A Final Word of Advice for Texas Executors

Stepping into the role of an executor can feel like being handed a complex puzzle without the picture on the box. But once you understand the core duties, it all starts to click into place. Let’s wrap up with the key principles of executor accounting in Texas, so you can move forward with confidence. Remember, these rules aren't meant to trip you up; they're there to protect you, the estate, and every single beneficiary.

Your entire role is built on one thing: trust. Honoring that trust means being completely transparent from day one.

Flawless Record-Keeping Is Your Best Defense

If you take away just one piece of advice, let it be this: keep impeccable records of everything. The moment you get your Letters Testamentary, open a dedicated bank account for the estate. Every dollar that comes in and every penny that goes out must be tracked, with a receipt, invoice, or bank statement to back it up.

This isn’t just a "nice to have"—it's your number one shield against personal liability. When a beneficiary asks a question or a doubt creeps in, a detailed ledger provides clear, indisputable answers. It’s what stops a simple question from snowballing into expensive and stressful probate litigation.

Know Your Role: Independent vs. Dependent

It’s absolutely critical to understand whether you’re serving as an independent executor or a dependent administrator. This distinction will define your entire experience and dictate how much the court looks over your shoulder.

- Independent Executors: You have far more freedom to act without court pre-approval. But with that freedom comes immense responsibility. You are still fully accountable to the beneficiaries, who can demand a formal accounting after 15 months have passed since the probate was opened.

- Dependent Administrators: You are under the court's direct and constant supervision. You’ll have to file a detailed annual accounting for a judge to review and approve, a process that adds another layer of scrutiny.

Getting this wrong is one of the easiest ways to make a major legal mistake. It fundamentally shapes the Texas probate process you'll have to follow.

Takeaway: Your duties as an executor are entirely manageable, especially with professional support. The legal framework isn’t there to intimidate you; it’s a roadmap for a fair and orderly process. With careful organization and the right guidance, you can fulfill your responsibilities confidently and honor the trust placed in you.

Ultimately, you don't have to walk this path alone. The law provides a clear route, and an experienced probate attorney can act as your guide, ensuring you stay on track and protecting both you and the estate every step of the way.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.

Frequently Asked Questions About Executor Accounting in Texas

Stepping into the role of an executor means you're going to have questions. That's a given. We find that having clear, straightforward answers is the best way to build your confidence and help you manage the estate correctly. Here are some of the most common questions we hear from executors about Texas accounting requirements.

Can a Beneficiary Waive the Right to an Accounting?

Yes, a beneficiary can legally waive their right to an accounting. This is typically done by signing a formal legal document, and it happens more often than you might think, especially in families with a high level of trust. Beneficiaries sometimes do this to make the process simpler and keep administrative costs down.

But this isn't a decision anyone should take lightly. A waiver is a binding legal document that frees you from a major fiduciary duty. Before you ever ask a beneficiary to sign a waiver—and before any beneficiary ever signs one—it’s crucial that both of you get advice from your own independent attorneys. Everyone needs to understand exactly what rights they are giving up.

What If I Make an Honest Mistake on an Accounting?

Executors are human, and estate administration is a tough, high-stress job. Honest mistakes are bound to happen. The real test isn’t whether you make a mistake, but how you fix it. Your best friend in this situation is transparency.

If you find an error—maybe a number was transposed, a small expense was overlooked, or a transaction was miscategorized—the right move is to correct it immediately and tell everyone. This usually means filing an amended accounting with the court and sending the corrected version to all the beneficiaries. Being upfront about the error and showing how you fixed it rebuilds trust, shows you’re serious about your duties, and protects you from any claims of trying to hide something.

Do I Need a Lawyer to Prepare an Estate Accounting?

While Texas law doesn't technically force you to hire an attorney for an estate accounting, trying to do it yourself is a huge risk. The rules in the Texas Estates Code are incredibly specific and strict. One small mistake or omission can have massive consequences, and you could find yourself personally on the hook for any financial losses to the estate.

A good probate attorney does far more than just fill out a form. They make sure your accounting is perfectly compliant with the law, that you have all the right supporting documents, and that you are shielded from personal liability. It’s an investment that can save you from incredibly expensive mistakes, smooth out the entire Texas probate process, and give you much-needed peace of mind. A professionally prepared accounting doesn’t just satisfy the judge; it gives beneficiaries the clear, solid answers they deserve.

Key Insight: Hiring a probate attorney to handle your accounting is an act of self-protection. It shields you from personal liability and makes sure the estate is closed out correctly, which is the best way to prevent the kind of disputes that lead to stressful and costly probate litigation.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.