Skip to content

Skip to content Yes, beneficiaries can sometimes access funds before probate is complete in Texas, but it depends almost entirely on how the account or asset was set up before death. If the estate may qualify for a small estate affidavit, that option is available only when the estate is under $75,000 excluding the homestead and exempt property, and the debts do not exceed the estate's value.

When a loved one dies, families usually aren't thinking about legal categories. They're thinking about the funeral home, the mortgage due next week, the electric bill, and whether they can get into Dad's bank account to keep everything afloat. That's a hard place to be, especially when grief and paperwork arrive at the same time.

The practical answer is that some money may be available quickly, and some may not be available until a court gives someone authority to act. The difference usually comes down to one question: Was the asset designed to pass outside probate, or was it owned only in the deceased person's name? That single detail often determines whether a beneficiary can receive funds right away or has to wait.

The Urgent Question After a Loss

A common situation looks like this. A parent passes away. Their adult children know there's money in the bank, but they also know bills are still coming. The funeral needs to be paid. The surviving spouse needs groceries and gas. Someone is calling about the mortgage. Then the family hears a phrase that feels like another locked door: probate.

That stress is real, and it's one of the first things families raise when they start learning about the Texas Probate Process. They want a clear answer to a very human question: can we get access to any of this money now, or do we have to wait until the whole probate case is over?

What families usually need to know first

The first point is reassuring. Probate doesn't block every asset. Some funds can move to a beneficiary without waiting for the entire estate administration to finish. Other funds are frozen for good reason, usually because the bank or financial institution needs proof of who has legal authority.

Practical rule: Start by identifying how each asset was titled, not by assuming everything is part of probate.

Families often discover they have a mix of assets:

- Direct-transfer assets: Insurance proceeds, retirement funds, or accounts with a named beneficiary.

- Court-controlled assets: Accounts owned only by the deceased person with no beneficiary designation.

- Gray-area situations: A bank account that might help with immediate expenses, but the paperwork doesn't clearly show a payable-on-death designation.

That last category creates the most anxiety. It's also where many online articles stop too soon. They explain the easy case, but not the harder one where the family needs emergency cash and the account wasn't set up cleanly.

What actually helps

The most productive first steps are simple:

- Collect the death certificate.

- Make a list of each account and policy.

- Ask each institution whether a beneficiary is listed.

- Find out whether the asset is probate or nonprobate.

- Avoid taking money without clear authority.

If you're asking, “Can Beneficiaries Access Funds Before Probate Is Complete in Texas?” you're really asking which of those paths applies to your family right now.

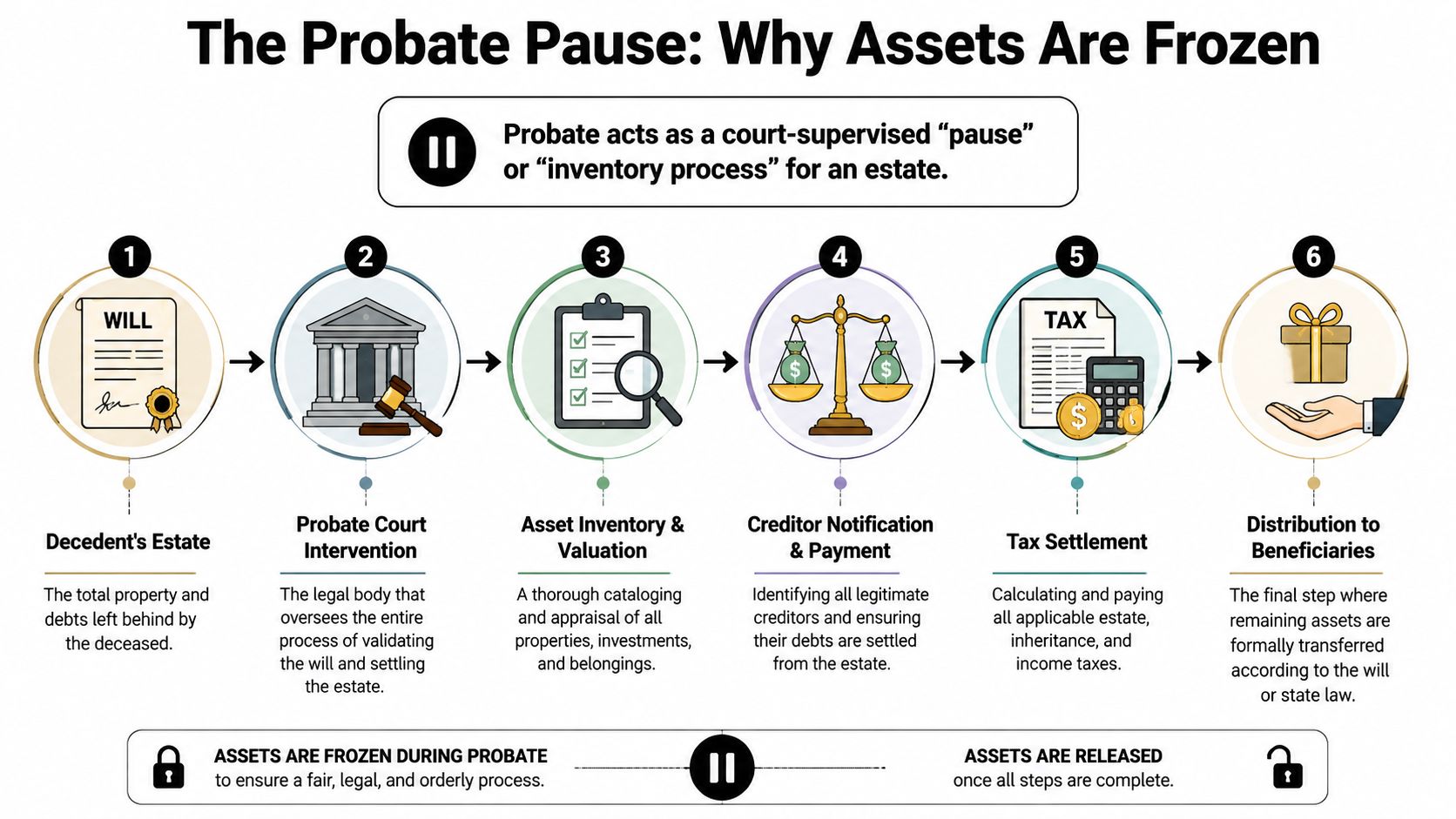

Why Probate Puts a Temporary Hold on Assets

Probate is easiest to understand as a court-supervised pause. It is the legal process used to identify the decedent's property, confirm who has authority to act, pay valid debts, and then distribute what remains under the will or, if there is no will, under Texas inheritance law. That basic framework appears throughout Title 2 of the Texas Estates Code, which governs estates of decedents.

Why banks and other institutions wait

A bank usually won't let a family member walk in and withdraw money from an account that was owned only by the deceased. From the bank's point of view, that money might need to be used to pay debts, there may be multiple heirs, or the person asking for access may not have authority yet.

That isn't the bank being difficult. It's the bank trying to avoid releasing funds to the wrong person.

Under Texas probate practice, the dividing line is clear. Assets with beneficiary designations are commonly treated as nonprobate transfers, while sole-owned assets are generally blocked until legal authority is established. The Texas State Law Library notes that a bank can transfer funds directly to the listed beneficiary, but if the asset is not structured that way, the family may have to wait until the court appoints an executor or administrator, as explained in the Texas State Law Library probate guidance before probate.

Plain-English probate terms

A few terms help make this easier:

- Probate estate: The property that must go through the court process before it can be distributed.

- Executor: The person named in a will to handle the estate, once the court approves that role.

- Administrator: The person the court appoints when there is no executor able to serve, often in an estate without a will.

- Letters Testamentary or Letters of Administration: Court papers that prove the person has authority to act for the estate.

Probate is not punishment. It is a control system that protects heirs, creditors, and the person handling the estate.

Why the pause can protect the family

That temporary hold serves several purposes:

- It protects the correct heirs: The court process helps prevent one relative from taking control before ownership is clear.

- It protects creditors: Estate debts generally must be addressed before final distributions.

- It protects the executor: A court appointment gives the executor legal authority to gather and manage estate property.

Title 3 of the Texas Estates Code also matters because it includes procedures for smaller or simpler estates, which can sometimes reduce delay. But when an asset is part of the probate estate, the basic rule still applies. Someone usually needs court authority before the money can be moved.

Immediate Access Pathways That Bypass Probate

The fastest access usually comes from assets that were set up to transfer automatically at death. These are often called nonprobate assets. They don't wait for the full probate case because the transfer mechanism was built in ahead of time.

Texas guidance reflects a consistent pattern. Beneficiary-designated assets pass outside probate, while sole-owned assets without that structure usually remain blocked until someone has court authority. If you want a plain-language overview of that distinction, this explanation of non-probate assets in Texas is a useful starting point.

Payable-on-death and transfer-on-death accounts

A payable-on-death account, often shortened to POD, is one of the most straightforward examples. The owner names a beneficiary with the bank. After death, the bank can transfer the funds directly to that beneficiary once the bank's documentation requirements are satisfied.

The same basic idea applies to transfer-on-death arrangements used for some investment accounts.

What usually works in practice:

- Bring the death certificate: The financial institution will usually need it.

- Bring identification: The named beneficiary must prove identity.

- Ask for the bank's claim process: Each institution has its own forms and review steps.

Insurance, retirement funds, and similar beneficiary assets

Texas Law Help explains that assets such as insurance proceeds, retirement funds, and bank accounts with payable-on-death beneficiaries can pass directly to named beneficiaries, bypassing the probate process. The same resource also explains that a small estate affidavit is available only if the estate is under $75,000 excluding the homestead and exempt property, and the estate's debts do not exceed the estate's value, as described in Texas Law Help's estate handling guide.

This is why families are often surprised to learn that one asset is available quickly while another remains tied up. Two accounts at the same bank can follow completely different rules depending on the paperwork signed before death.

Survivorship accounts and trust assets

Some accounts are owned jointly with a survivorship feature. In that setup, the surviving owner may continue to have access because the account passes by ownership structure rather than through the probate estate.

Trust assets work differently, but the practical effect can be similar. If the property is held in a trust, the trustee may have authority to manage and distribute it under the trust terms without waiting for probate of the decedent's estate.

The title on the account often matters more than the value in the account.

What doesn't bypass probate

Families sometimes assume the following will be enough, but often they won't be:

- A will by itself: A will does not automatically make accessible a sole-owned bank account the day after death.

- Being the oldest child: Family status is not the same as legal authority.

- Having access to online banking: Using a deceased person's credentials can create serious problems.

If the account was owned solely by the deceased and no beneficiary was named, direct access is usually delayed until the estate has the proper legal authority in place.

For planning purposes, this is also why many families review beneficiary forms, account ownership, and Wills & Trusts together instead of treating them as separate topics.

Simplified Court Options for Smaller Estates

Not every estate needs full probate administration. Texas law provides some simpler options for certain situations, especially when the estate is modest or uncomplicated. These procedures appear in Title 3 of the Texas Estates Code and can be helpful when assets weren't set up to pass automatically.

Small estate affidavit

A small estate affidavit is often the first option families ask about. It can help when the estate is small enough and meets the legal requirements. The most important threshold is fixed: the estate must be under $75,000 excluding the homestead and exempt property, and the estate's debts cannot exceed the estate's value.

That sounds simple, but eligibility is narrower than many people expect. Families should review the details carefully before assuming this route will work. This guide to the Texas small estate affidavit form gives a practical look at what the process involves.

Muniment of title

A muniment of title is another simplified probate tool. In plain English, it allows the court to recognize a will as a document of title transfer without requiring a full administration in the right circumstances. It is often discussed when the estate is relatively simple and the main need is to transfer property rather than manage a broad pool of debts and ongoing administration.

A muniment of title is not a substitute for every probate case. But in the right estate, it can avoid some of the time and cost of a more involved administration.

Comparing Texas's Simplified Probate Procedures

| Procedure | Best For | Key Requirement | Typical Timeline |

|---|---|---|---|

| Small Estate Affidavit | Smaller estates needing a simplified court path to collect certain assets | Estate must be under $75,000 excluding homestead and exempt property, and debts must not exceed estate value | Often shorter than full administration, but timing depends on court review and bank acceptance |

| Muniment of Title | Estates where the primary need is recognizing a will for transfer purposes rather than full administration | Appropriate only in specific circumstances under Texas probate law, often where broad administration is unnecessary | Often more streamlined than full probate when it fits the estate |

A simplified procedure is still a legal procedure. It only works when the estate fits the rules.

Which shortcut fits which problem

A small estate affidavit is often considered when the family needs access to assets and there is no fully structured nonprobate transfer. A muniment of title is more often useful when the estate's problem is title transfer, not day-to-day cash management.

That distinction matters. If your immediate problem is an unpaid funeral bill or utility shutoff notice, the question isn't just “Can we avoid probate?” The core question is which legal tool matches this particular asset and this particular need?

The Executor's Responsibility and Risks of Early Payouts

The executor often becomes the person everyone calls when money is tight. A son wants help with funeral costs. A surviving spouse needs cash for the mortgage. Another family member insists Dad would have wanted the children paid right away.

That pressure is real, but an executor cannot treat estate funds like a family checking account.

Why caution matters

Under Texas probate law, the executor's job includes identifying estate assets, protecting them, addressing valid debts, and making distributions that can stand up to later scrutiny. Paying too soon can create personal liability for the executor, even when the executor was only trying to help the family through a hard month.

Texas probate guidance explains that debts should be addressed before distributions are made, and creditors generally have a four-month claims window in Texas. Early payouts can become a serious problem if a creditor appears later or if one heir receives money before the executor understands the full picture, as discussed in this analysis of when funds can be distributed after probate in Texas.

Families often read caution as delay. From the executor's side, caution is often the safest course.

Where early distributions become dangerous

The highest-risk cases are the ones that look manageable at first. There is cash in an account. The family has immediate bills. No one expects a fight. Then a medical bill surfaces, a tax issue appears, or one sibling questions why another received money first.

I regularly tell families to separate two questions. First, is this asset part of the probate estate at all? Second, if it is, does the executor have enough authority and enough information to release funds safely? Those are different questions, and mixing them up causes trouble.

For accounts that may pass outside probate or may be released under a bank's internal procedures, this guide on how Texas banks may release funds without probate helps explain why a bank's answer is often more restrictive than the family expects.

A practical way to assess the risk looks like this:

- Lower risk: Money passes by beneficiary designation and never becomes part of the estate for the executor to divide.

- Moderate risk: The executor has authority, but the estate's debts, reimbursement issues, or family expectations are still unclear.

- Higher risk: The executor distributes estate funds before checking for creditor claims, equal treatment among beneficiaries, and any chance of a dispute.

For readers who want a short video explanation of the probate process and timing, this overview may help frame the issue:

When family pressure turns into legal exposure

Uneven early payments are a common source of conflict. If one child gets an advance for "emergency expenses" and another child gets nothing, the executor may later need receipts, written agreements, and a clear legal reason for the difference.

The other risk is reimbursement. If the executor pays out too much and a valid debt must be paid later, the executor may have to ask beneficiaries to return money. That is hard to do in any family. In some cases, the executor ends up covering the shortfall personally.

That is why legal advice early in the process can save money and relationships later. A probate lawyer can help the executor decide whether a requested payout is a reasonable interim step or a move that creates unnecessary exposure. If the disagreement has already turned into a conflict over fairness, authority, or missing funds, that issue can overlap with Probate Litigation.

A Real-World Scenario The Thompson Family

Mrs. Thompson dies on a Thursday. By Friday, her daughter is asking a question I hear often: “There is money in Mom's accounts, so why can't we use it for the funeral and the mortgage?”

The answer depends on how each asset was set up before death, not on how urgent the need feels.

In the Thompson family, one checking account names the daughter as a payable-on-death beneficiary. A separate savings account is in Mrs. Thompson's name alone, with no beneficiary designation. The house is also still titled in Mrs. Thompson's sole name.

That mix changes everything.

What the family can get quickly

The daughter can usually claim the POD checking account directly through the bank after providing the death certificate and the bank's claim paperwork. That money does not have to wait for the full probate process because the account already names who receives it.

For this family, that creates immediate breathing room. Funeral expenses can be paid. A utility cutoff can be avoided. The family gets time to make careful decisions instead of acting out of panic.

Where the pressure builds

The savings account is different. No one gets access to it because they are a child, spouse, or named beneficiary under a will. If the bank sees an account titled only in the decedent's name with no beneficiary, it will usually freeze the account until someone has legal authority to act.

Families find this frustrating for a good reason. They can see the money on a statement, but they still cannot use it for immediate bills.

The house raises a separate issue. A house does not transfer the same way a POD bank account does, and the executor has to determine whether probate, an affidavit, or another transfer method applies before promising anyone that the property can be sold or retitled quickly.

Why this example matters

The Thompson family's problem is not unusual. It is the pattern I want families to look for early. One asset may be available within days. Another may be tied up for weeks or longer. That split often decides whether the family can cover urgent expenses without borrowing.

It also affects the executor's risk. If the daughter receives POD funds in her own right, that is one thing. If an executor starts handing out money from the estate-owned savings account before authority is clear, that creates a different legal problem.

A practical first step is to sort each asset into its own category:

- Checking account with POD beneficiary: Usually claimed directly from the bank by the named beneficiary.

- Savings account in sole name: Usually requires probate authority or a qualifying simplified procedure before release.

- House in sole name: Requires a separate title and probate analysis before transfer.

Families often expect the estate to move as one unit. It does not. In Texas probate, access usually happens asset by asset.

Key Insights and When to Call an Attorney

The answer to “Can Beneficiaries Access Funds Before Probate Is Complete in Texas?” is yes in some cases, no in others, and sometimes not yet. The deciding factor is usually not the family relationship. It is the legal structure of the asset.

Key Insight

Here are the points that matter most:

- Asset titling controls timing: A beneficiary designation, survivorship feature, or trust structure can allow access without waiting for the full probate case.

- Sole-owned accounts are different: If the account was only in the deceased person's name and has no beneficiary, the bank will usually require court authority.

- Small estates may have a shortcut: Texas provides a small estate affidavit for qualifying estates under $75,000 excluding the homestead and exempt property, if debts do not exceed estate value.

- Executors have to think defensively: Early distributions can create problems if debts, creditor claims, or heir disputes emerge later.

- Mixed estates are the norm: Many families have one asset that moves quickly and another that stays tied up.

When legal help becomes especially important

Some situations deserve immediate legal review:

- There is no clear beneficiary designation.

- The family needs money urgently for funeral, housing, utilities, or medical costs.

- The estate may qualify for a simplified procedure, but you aren't sure.

- Heirs disagree about who should receive what.

- The executor is being pressured to distribute funds early.

- The estate includes a house, business interests, or out-of-state heirs.

- A minor or incapacitated person may need protection, which can raise related Guardianship issues.

A lawyer can help identify which assets bypass probate, which assets require court action, and whether a cautious partial distribution is realistic or too risky. The Law Office of Bryan Fagan, PLLC handles probate administration, small estate matters, heirship issues, and estate-related disputes for Texas families who need that kind of guidance.

If you're dealing with this right now, don't assume every delay means something is wrong. In many estates, the question is not whether funds exist. It's whether the law allows access today, after court appointment, or only after debts and administration are handled.

If you're facing probate in Texas, our team can help guide you through every step, from filing to final distribution. Schedule your free consultation today.