Planning for your future can feel overwhelming, especially when you’re trying to protect your family. Understanding the difference between a durable vs medical power of attorney is simpler than it seems and is a crucial step in that process. Think of it this way: one document gives someone you trust control over your finances, while the other gives them a say in your healthcare.

In Texas, these are two entirely separate legal tools, and for a complete estate plan that protects your loved ones from court intervention, you absolutely need both.

Understanding Your Key Estate Planning Tools

When Texas families start putting their affairs in order, they often encounter two documents that sound confusingly similar: the Durable Power of Attorney (DPOA) and the Medical Power of Attorney (MPOA). While both grant decision-making authority to a trusted person (your “agent”), they operate in completely different spheres of your life.

Thinking about a time when you can’t speak for yourself is tough. We understand that this process can be emotional. However, creating these documents is an act of love—it shields your family from confusion, bitter conflicts, and expensive court battles during an already difficult time.

The main goal here is to ensure your wishes are followed without a judge ever needing to get involved. If you don’t have these documents in place, your loved ones would likely face a stressful and public Guardianship process just to get the authority to manage your affairs.

Comparing the Two Documents at a Glance

To make their distinct roles crystal clear, here’s a straightforward breakdown of what each document handles. For a more detailed look, you can learn more about what a power of attorney is and how it works under Texas law in our detailed guide.

| Feature | Durable Power of Attorney (Financial) | Medical Power of Attorney (Healthcare) |

|---|---|---|

| Primary Focus | Manages your financial and legal affairs. | Governs your medical and healthcare decisions. |

| Agent’s Authority | Pays bills, manages bank accounts, sells property. | Consents to medical treatments, makes end-of-life choices. |

| When It’s Used | Can be effective immediately or only upon your incapacity. | Only becomes effective when you cannot make medical decisions. |

| Governing Law | Primarily governed by Title 2 of the Texas Estates Code. | Primarily governed by the Texas Health and Safety Code. |

Grasping this fundamental separation is the first step toward building a solid estate plan that fully protects you and empowers the people you trust most.

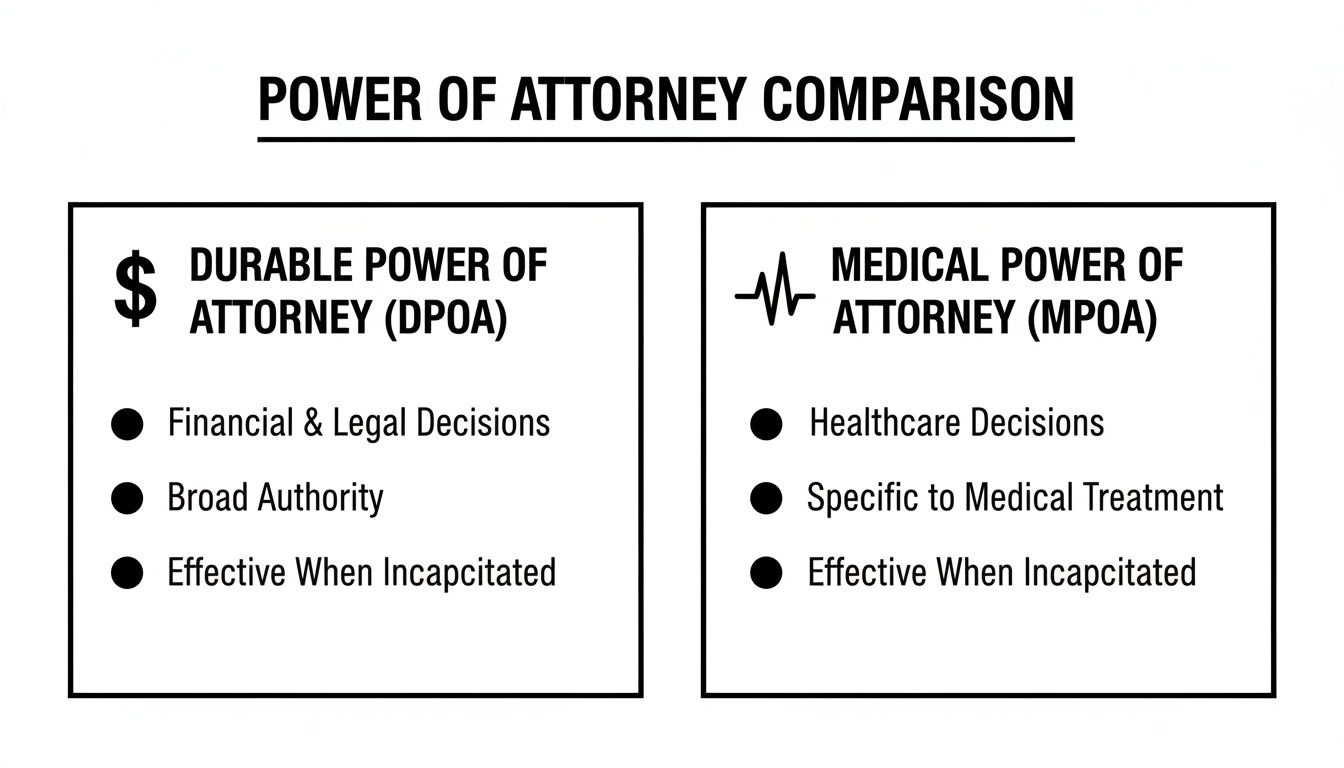

Comparing Financial vs. Healthcare Authority in Texas

In Texas, the law draws a hard line between managing your money and making decisions about your health. This isn’t an accident; it’s a deliberate legal design to protect you. That’s why we have two entirely separate documents: the Durable Power of Attorney (DPOA) for financial matters and the Medical Power of Attorney (MPOA) for healthcare.

Getting a handle on their distinct roles is the absolute key to crafting an estate plan that truly protects every corner of your life. Think of it like this: your DPOA agent is your financial stand-in, while your MPOA agent is your healthcare advocate. They operate in parallel but completely separate lanes, making sure decisions are made by the person best suited for that specific job.

The Durable Power of Attorney for Financial Decisions

A Durable Power of Attorney is a powerful legal tool you sign to grant a trusted person—your “agent”—broad authority over your financial and legal life. This isn’t just about letting someone access your checking account to pay a light bill. It’s a comprehensive document that allows your agent to handle nearly any financial task you could do yourself.

Under the Texas Estates Code, Title 2, a properly drafted DPOA can authorize your agent to:

- Pay your mortgage, utilities, and other recurring bills.

- Manage your investment portfolio and retirement accounts.

- Buy or sell real estate on your behalf.

- File your tax returns and deal with the IRS.

- Keep your small business running.

The most critical feature here is the word “durable.” This single provision ensures the document remains legally effective even if you later become incapacitated from an illness or an accident. Without it, the power of attorney would automatically become void the moment you could no longer make your own decisions—making it utterly useless right when your family needs it most.

The Medical Power of Attorney for Healthcare Decisions

Now, let’s switch gears. A Medical Power of Attorney is laser-focused on one thing: your health. This document empowers your chosen agent to make medical decisions for you, but—and this is a big difference—only when a physician certifies in writing that you are unable to make them for yourself. Its entire purpose is to ensure someone who knows your values and wishes can speak for you when you can’t.

Your MPOA agent’s authority is strictly medical and includes the power to:

- Consent to or refuse medical treatments, surgeries, and medications.

- Choose your doctors, hospitals, and long-term care facilities.

- Access your protected medical records.

- Make difficult end-of-life decisions, like those involving life support, but always in line with your stated wishes.

The scope is where these two documents really diverge. A DPOA lets an agent handle your money, while an MPOA is purely for medical choices. This avoids a nightmare scenario where your medical agent can approve a procedure, but no one has the legal authority to access the funds to pay for it. You can learn more about how a durable power of attorney for health care works from our dedicated guide.

Key Insight

This separation of powers is completely intentional. Your best friend might be a financial whiz who is perfect for your DPOA, while your sibling who is a nurse is the obvious choice for your MPOA. Texas law lets you appoint the best person for each job, preventing any one agent from having absolute control over every aspect of your life.

How Activation Triggers and Legal Limits Differ

One of the biggest distinctions between a durable and medical power of attorney is how and when each document actually springs into action. While you create both to protect yourself during incapacity, they don’t just turn on like a light switch in the same way. Understanding these activation triggers is critical to making sure your wishes are honored without delay when it matters most.

A Durable Power of Attorney (DPOA) for finances gives you a choice. You can decide if it becomes effective the moment you sign it, or if it only “springs” into effect upon a specific event—usually, a doctor’s written declaration that you are incapacitated. This flexibility is a huge advantage.

On the other hand, a Medical Power of Attorney (MPOA) is almost always a springing document here in Texas. It only activates when your attending physician certifies in writing that you lack the capacity to make your own healthcare decisions. This is a built-in safeguard to protect your medical autonomy for as long as possible.

When Does Each Document Take Effect?

The timing of when your agent can step in is a core difference between a DPOA and MPOA. An immediate DPOA allows an agent to help out seamlessly, which is invaluable when you consider that a court-supervised guardianship can take months to set up.

And it’s not just an issue for the elderly. Unexpected events like car accidents can happen to anyone, which is why experts emphasize that every adult needs a healthcare POA. You can read the full analysis on the importance of these documents for every adult.

- Durable Power of Attorney (DPOA): You can set this up to be effective immediately. This lets your agent help with financial matters for convenience, even while you’re perfectly capable. Alternatively, a “springing” DPOA only becomes active upon your incapacity, as defined in the document itself.

- Medical Power of Attorney (MPOA): In Texas, this document lies dormant until a physician determines you can no longer make or communicate your healthcare choices. Your agent simply cannot act until this medical certification happens.

This chart offers a clear, side-by-side look at how a financial DPOA and a healthcare MPOA stack up.

As the comparison shows, while both documents empower an agent you trust, their domains—money versus medicine—and their activation triggers are fundamentally different.

Understanding the Legal Boundaries of Your Agent

Handing someone power of attorney doesn’t give them a blank check or unlimited authority. The Texas Estates Code puts firm legal limits in place to protect you from abuse or overreach. Your agent is a fiduciary, which is a legal term meaning they have a strict duty to act in your best interest, manage your affairs with care, and avoid any conflicts of interest.

Think of your agent as stepping into your shoes, but only to carry out your known wishes or what they reasonably believe you would want. They are absolutely not allowed to use their position for personal gain. This fiduciary duty is the legal backbone of both the DPOA and MPOA, and an agent who violates it can face serious civil and even criminal penalties. For families who suspect a breach of this duty, understanding your options in probate litigation is crucial.

Durable vs Medical Power of Attorney: A Head-to-Head Comparison

This table provides a clear, at-a-glance comparison of the key features, authority, activation, and legal requirements for Durable and Medical Powers of Attorney in Texas.

| Feature | Durable Power of Attorney (Financial) | Medical Power of Attorney (Healthcare) |

|---|---|---|

| Change Your Will | An agent cannot create, amend, or revoke your Last Will and Testament. | Your healthcare agent has no authority over your will or estate plan. |

| Make Healthcare Decisions | The DPOA agent cannot make medical decisions unless you have also named them as your MPOA agent. | This is the agent’s primary role, but they cannot make financial decisions. |

| Alter Beneficiaries | An agent is prohibited from changing beneficiaries on your life insurance or retirement accounts. | This is outside the scope of the MPOA; the agent has no such power. |

| Act Selfishly | The agent must always act in your best interest, not their own. Using your assets for their benefit is illegal. | Decisions must align with your known values and wishes, not the agent’s personal beliefs. |

These legal guardrails are there for your protection. While you are placing immense trust in the agents you choose, Texas law makes sure that trust is backed by strict legal accountability. Creating these documents is a critical step in building a complete estate plan that may also include Wills & Trusts to give you and your family total protection.

Real-World Scenarios for Texas Families

Legal documents can feel abstract. Their true value only clicks when you see them play out in real life. The difference between a durable vs medical power of attorney isn’t just a technicality—it’s a critical distinction that can make or break a family during a crisis.

These stories show how each document works and highlight the chaos that can erupt when they’re missing.

Scenario One: The Durable Power of Attorney in Action

Meet Sarah, a retired teacher in Houston. Her father, David, is 78 and in the early stages of dementia. He’s still sharp on good days, but he’s getting more forgetful. Bills get misplaced, and he nearly forgot to pay his property taxes last year.

Years ago, David wisely created a Durable Power of Attorney (DPOA) and named Sarah as his agent. Because he made it effective immediately, Sarah had the legal authority she needed to step in and help manage his finances without getting a court involved.

How the DPOA Helped:

- Paying for Care: Sarah was able to access David’s retirement account to pay for his in-home caregiver and put down a deposit at an assisted living facility.

- Managing Bills: She logged into his bank accounts to set up automatic payments for his mortgage and utilities, preventing late fees and the risk of foreclosure.

- Handling Property: When David needed to sell his home to fund his long-term care, Sarah worked with a realtor, signed all the closing documents, and managed the sale proceeds on his behalf.

Without that DPOA, Sarah’s life would have been a nightmare. She would have been forced to petition a court to establish a guardianship—a public, expensive, and emotionally draining process. It would have meant hiring attorneys, attending hearings, and providing constant accountings to a judge just to get permission to pay her father’s bills with his own money.

The DPOA let her act quickly and privately, ensuring David’s needs were met without missing a beat.

Scenario Two: A Crisis Requiring a Medical Power of Attorney

Now let’s look at Maria and Carlos, a married couple in their 40s from Dallas. One evening, Carlos is in a serious car accident. He’s rushed to the hospital, unconscious and unable to communicate. The doctors tell Maria he needs emergency surgery for internal bleeding—a decision that has to be made right now.

Fortunately, Carlos had prepared a Medical Power of Attorney (MPOA), naming Maria as his healthcare agent.

Once the attending physician certified that Carlos was incapacitated, Maria’s authority as his agent kicked in. She was legally empowered to step into his shoes and make medical decisions for him.

How the MPOA Helped:

- Authorizing Treatment: Maria was able to consent to the life-saving surgery on Carlos’s behalf without any delay.

- Communicating Wishes: Weeks later, when faced with a tough choice about a high-risk procedure, Maria remembered conversations she and Carlos had about his fear of being kept on life support. She used that knowledge to guide her decisions, confident she was honoring his values.

- Accessing Records: The MPOA gave her the legal right to speak with doctors, review medical charts, and get a second opinion, making sure she was fully informed.

If Carlos hadn’t created an MPOA, the hospital would have been in a tough spot. They might have sought consent from Maria as his next of kin, but if other family members disagreed, the hospital could have demanded a court order for non-emergency care. This could have triggered a guardianship proceeding just to appoint someone to make medical decisions—a devastating delay in a time-sensitive crisis.

The MPOA ensured Carlos’s care was guided by the person who knew him best, not a judge. The Texas Probate Process can be complicated enough; avoiding court intervention for medical decisions is a huge relief for families.

How to Create Legally Valid Documents in Texas

Knowing you need a Durable Power of Attorney (DPOA) and a Medical Power of Attorney (MPOA) is one thing. Creating legally sound documents that will actually work when your family needs them most is another challenge entirely. In Texas, this means paying close attention to state-specific rules to make sure your wishes are legally enforceable.

Grabbing a generic form you found online is a huge risk. These one-size-fits-all documents often fail to comply with the Texas Estates Code, which can render them invalid right when they’re critically needed. It’s far safer to use either the official Texas statutory forms or have an attorney draft custom documents tailored to your unique family and financial situation.

Formal Signing Requirements in Texas

Texas law is very specific about how these documents must be signed and witnessed. If you don’t follow these rules to the letter, you give someone grounds to challenge their validity later on, leading to the exact court intervention you were trying to avoid.

For both a DPOA and MPOA, the signing process has strict requirements:

- You (the Principal): You must sign the document in the physical presence of a notary public.

- Notary Public: The notary has to acknowledge your signature, verifying your identity and that you signed willingly. For a DPOA, this is the only requirement.

- Witnesses (for MPOA): A Medical Power of Attorney has a higher bar. It must be signed by two qualified adult witnesses in your presence. These witnesses absolutely cannot be your agent, a relative, an heir to your estate, or an employee of your healthcare facility.

These formalities aren’t just red tape. They are crucial safeguards designed to prevent fraud and coercion, ensuring the documents truly reflect your intentions.

Common and Costly Mistakes to Avoid

When you’re creating these powerful legal tools, certain mistakes can have devastating consequences for your family. Being aware of these pitfalls can help you put together a plan that is both effective and secure.

One of the most frequent errors we see is choosing the wrong agent. This isn’t just about trust; it’s about picking someone who is responsible, organized, and capable of handling stress. Naming an agent with a history of financial trouble or who doesn’t get along with other family members is a recipe for chaos.

Another critical mistake is forgetting to name alternate agents. If your primary agent is unable or unwilling to serve when the time comes and you have no backup, your family may be forced into a Guardianship proceeding—the very outcome you were trying to prevent.

These documents are not “set it and forget it.” Life changes, and your estate plan should, too. Reviewing your DPOA and MPOA every few years ensures they still align with your wishes and that your chosen agents are still the right people for the job. To see how these documents fit into a broader healthcare strategy, you can learn more about combining a living will and power of attorney.

Takeaway

Having both a DPOA for finances and an MPOA for health isn’t just wise—it’s essential for a complete plan. These documents are your voice when you cannot speak for yourself, keeping critical decisions in the hands of the people you trust and out of a courtroom. It’s about preserving family harmony and making sure your wishes are respected without a judge having to get involved.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.

Frequently Asked Questions About Powers of Attorney

Even after families in Texas get a handle on the differences between a durable vs. medical power of attorney, a lot of practical questions come up. These are the documents that will be used in a real crisis, so it’s natural to wonder how they actually work. We’ve gathered some of the most common questions we hear from clients to give you a clearer picture and help you feel more confident about your plan.

Can I Name the Same Person for Both Roles?

Yes, you absolutely can. Many people choose one trusted person—very often a spouse or an adult child—to serve as the agent for both their Durable (financial) and Medical Power of Attorney. This can make decision-making much smoother during an emergency, since one person has a complete view of your financial and healthcare situation.

But that doesn’t mean it’s the right choice for everyone. You need to think hard about whether the person best suited to manage your finances is also the right person to make tough healthcare calls. Sometimes, the most financially savvy person in your life is not the one who is emotionally equipped to handle end-of-life choices. The law gives you the flexibility to appoint the best person for each distinct job.

What Happens if I Don’t Have These Documents in Texas?

This is a critical point that many people miss: if you become incapacitated without a Durable Power of Attorney and a Medical Power of Attorney, your family can’t just step in and take over. They will be forced to go to court and petition for a guardianship.

A guardianship is a formal, court-supervised process where a judge appoints someone to manage your personal and financial affairs. It’s a path you want to avoid at all costs. Guardianship proceedings are:

- Public: Your private medical and financial life becomes part of the public court record.

- Expensive: The process racks up significant court costs and attorney’s fees, all of which are paid from your assets.

- Time-Consuming: It can take months to get a guardian appointed, leaving your affairs—and your family—in limbo during a critical time.

- Stressful: The court process often creates conflict among family members who might disagree on who should be in charge or what decisions should be made.

Putting powers of attorney in place now is the single best way to avoid this burdensome court process and keep control within your family. A guardianship should always be seen as the last resort.

How Often Should I Review My Power of Attorney Documents?

Your powers of attorney are not “set it and forget it” documents. Life changes, relationships shift, and your estate plan needs to evolve right along with them. As a rule of thumb, we recommend reviewing these documents every 3 to 5 years, or any time a major life event happens. A regular review ensures your documents remain effective and truly reflect your current wishes. An outdated document can cause as many problems as having no document at all.

Think about pulling out your documents for a review if any of these things occur:

- You get married, divorced, or become widowed.

- Your chosen agent passes away, becomes incapacitated, or moves far away.

- Your relationship with your agent changes for the better—or worse.

- There are major changes to your financial situation.

- Texas updates its laws governing powers of attorney.

Keeping your documents current ensures the people you trust most are empowered to act for you when you need them. It’s a simple step that provides lasting peace of mind for you and your loved ones, and it works hand-in-hand with other essential documents like your Wills & Trusts.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.