When a loved one passes away, the last thing your family wants is to face a drawn-out, complicated court process. Dealing with grief is hard enough without adding legal burdens. This is exactly why understanding non-probatable assets is so critical for Texas families.

Think of them as a direct path for your legacy. These are assets legally set up to transfer straight to a named person upon death, completely sidestepping the formal Texas probate court system. This thoughtful planning can bring immense relief and clarity to your loved ones during a difficult time.

What Are Non-Probatable Assets in Texas?

When you’re looking at an estate in Texas, it helps to imagine two buckets of property: one for assets that must go through the court-supervised probate process, and another for those that don’t. Non-probatable assets fall into that second bucket. They are designed to avoid court intervention, making the transfer of wealth faster, more private, and less expensive for the family left behind.

The power is in how they’re set up. Before a person passes away, they can use simple legal tools recognized under the Texas Estates Code to essentially attach a “pre-addressed shipping label” to certain assets. This label ensures the property goes straight to its intended recipient without needing a judge’s stamp of approval.

How These Assets Bypass Probate

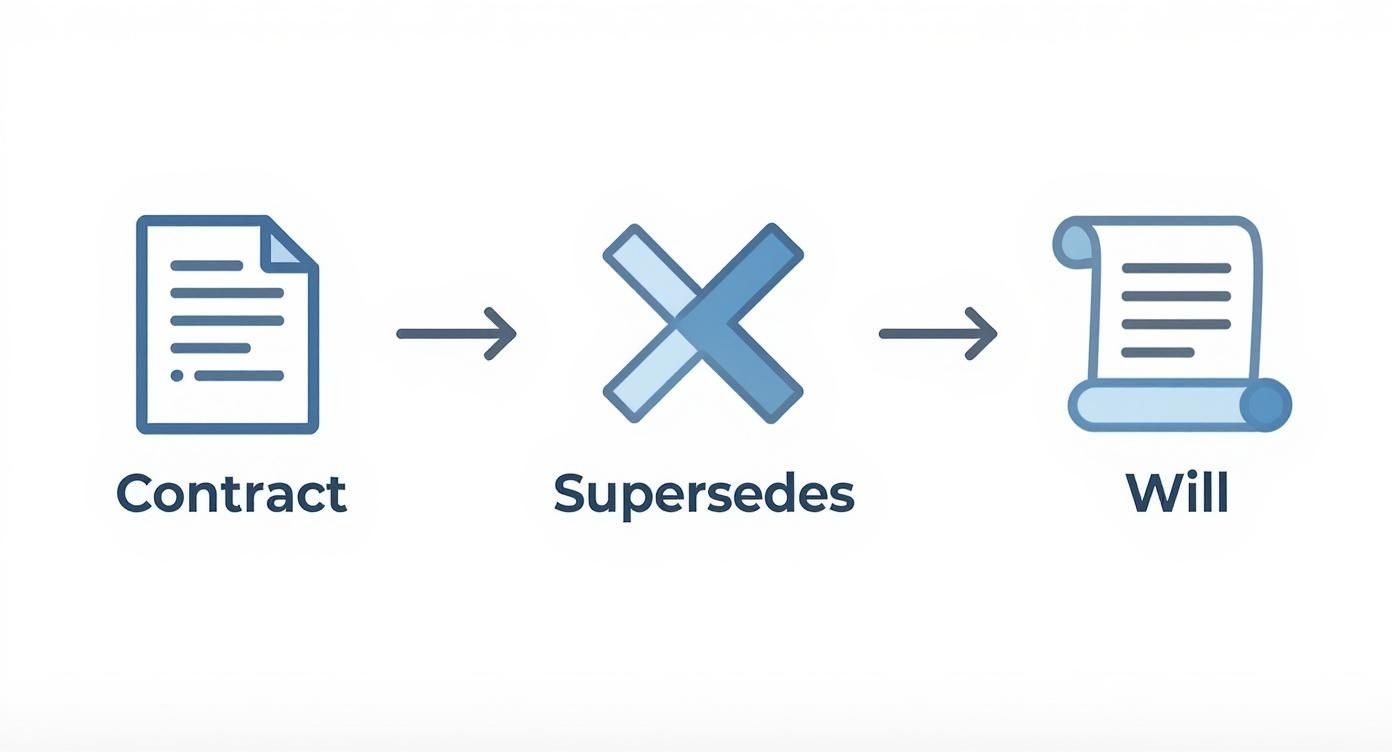

The legal mechanics behind non-probatable assets are refreshingly straightforward and are based on contracts or legal titling that, by law, supersede what is written in a will. The will might say one thing, but the asset’s own instructions take priority.

The most common ways this is done include:

- Beneficiary Designations: Naming a specific person or entity to inherit an account, like a life insurance policy or an IRA. This is a direct instruction to the financial institution.

- Joint Ownership with Right of Survivorship: When one co-owner dies, the property automatically and immediately passes to the surviving co-owner(s) by operation of law.

- Payable-on-Death (POD) or Transfer-on-Death (TOD) Accounts: Designating someone to receive the account balance or security upon your death. It’s as simple as filling out a form at your bank or brokerage.

These tools are a cornerstone of modern estate planning. A huge portion of an average family’s wealth is held in these types of accounts, especially retirement funds. In fact, industry reports show that around 90% of IRA owners have named at least one beneficiary, highlighting just how common this probate-avoidance strategy is. You can learn more about these financial tools in our guide on how IRAs and 401(k)s are handled in Texas.

By understanding and properly using non-probatable assets, you can offer immense peace of mind and clarity to your family. It’s strategic planning that ensures your wishes are carried out efficiently and without unnecessary legal red tape.

Probate vs. Non-Probate Assets at a Glance

This table offers a quick comparison to help you immediately distinguish between assets that typically go through probate and those that do not.

| Asset Category | Typically a Probate Asset? | How It Transfers |

|---|---|---|

| Real Estate (Sole Ownership) | Yes | Through the will and probate court. |

| Bank Account (Sole Ownership) | Yes | Through the will and probate court. |

| Life Insurance Policy | No | Directly to the named beneficiary. |

| Retirement Accounts (IRA, 401k) | No | Directly to the named beneficiary. |

| Joint Bank Account (w/ Survivorship) | No | Automatically to the surviving joint owner. |

| Assets in a Living Trust | No | According to the trust’s instructions. |

| Personal Property (Furniture, etc.) | Yes | Through the will and probate court. |

As you can see, the key difference almost always comes down to whether a beneficiary was named or how the asset was titled. This simple step can be the difference between a smooth transition and a months-long court process.

Common Ways to Avoid Probate in Texas

Texas law gives families several powerful tools to move assets to their loved ones without ever setting foot in a probate court. While each strategy works a little differently, they all share one compassionate goal: making the transfer of your property as simple as possible for those you leave behind.

Getting a handle on these options is the first step toward building an estate plan that brings clarity and peace of mind. Let’s walk through the most common types of non-probatable assets and see how they operate. These are the building blocks that can shield your family from needless delays, costs, and stress when they’re already going through an emotional time.

Key Estate Planning Tools

Here are the primary ways Texans can structure their assets to bypass the probate system:

- Living Trusts: Think of a trust as a legal container you create to hold your assets. You move ownership of your property—like your house or investment accounts—into this container. Because the trust owns the assets, not you personally, there’s nothing for the probate court to oversee when you pass away. Instead, your handpicked successor trustee simply manages and distributes everything according to the rules you already set in the trust document. Our firm can help you explore Wills & Trusts.

- Life Insurance & Retirement Accounts: Policies like life insurance and accounts like 401(k)s and IRAs are contracts. When you fill out that beneficiary form, you’re giving the financial institution a legally binding instruction to pay the money directly to that person. This simple designation completely bypasses your will and the probate court.

- Payable-on-Death (POD) Accounts: This is one of the easiest ways to keep a bank account out of probate. All it takes is filling out a form at your bank to name a beneficiary. When you pass, that person can claim the funds directly with a death certificate and ID, no court order needed.

- Joint Tenancy with Right of Survivorship (JTWROS): When two or more people own property this way (common with real estate and joint bank accounts), the surviving owner automatically absorbs the deceased owner’s share. The transfer is instant and happens by “operation of law,” keeping the asset out of the probate estate entirely.

A Real-World Example of Non-Probatable Assets

Imagine Maria’s father, Robert, wanted to ensure she had immediate access to his checking account to cover funeral expenses after he passed. He went to his bank and filled out a form designating Maria as the Payable-on-Death (POD) beneficiary.

When Robert died, that bank account was not part of his probate estate. Maria simply went to the bank with his death certificate and her own ID. The bank transferred the entire balance directly to her that same day. This one simple step, authorized under the Texas Estates Code (specifically Title 2), saved her time, money, and the anxiety of waiting for a judge’s approval. It’s a perfect illustration of how a non-probatable asset works to support a family in a time of need.

Texas law offers a similar tool for real estate called a Transfer on Death Deed (TODD), which works much like a POD account for your home or land. You can dive deeper into how a TODD affects real estate in our detailed guide. Each of these strategies is a powerful way to make sure your legacy is passed on efficiently and exactly as you intended.

How Beneficiary Designations Legally Bypass a Will

It’s one of the biggest—and most painful—surprises Texas families encounter during probate: a last will and testament does not control every single asset a person owned. This hard truth often surfaces at the worst possible time, compounding the grief of losing a loved one.

The reason boils down to a powerful legal principle: a beneficiary designation is a binding contract that legally supersedes a will. It’s a direct instruction that can’t be overruled by the more general instructions in a will.

When you name a beneficiary on a life insurance policy, an IRA, a 401(k), or a bank account, you’re creating a direct contract with that financial institution. That contract legally obligates the institution to pay the asset directly to the specific person you named upon your death. Think of it as a specific, legally enforceable command for that one asset.

The Contract Always Wins

Your will provides the grand plan for your overall estate, but a beneficiary designation is a specific, contractual order for a particular account. Under the Texas Estates Code, this contractual obligation takes priority. The financial institution must honor its contract with you, no matter what your will might say.

This is a critical point that can completely change the outcome for families. It shows why just having a will isn’t enough; you also have to make sure your beneficiary designations are in sync with your overall estate plan. Without that alignment, your true wishes might not be fulfilled.

A Critical Example: Imagine John’s will clearly states his entire estate should be divided equally between his two children. Years ago, however, he named his ex-wife as the beneficiary on his sizable 401(k) and never updated it after their divorce. When John dies, the 401(k) provider is legally required to pay the entire account balance to his ex-wife. The will’s instructions are irrelevant for that specific asset because the beneficiary contract overrides it.

This exact scenario plays out in Texas probate courts all the time, and it almost always leads to family conflict and heartache. It highlights why regularly reviewing and updating these forms is one of the most important steps in maintaining a solid estate plan.

It’s a simple action that prevents confusion, honors your real intentions, and protects your loved ones from potential disputes or financial hardship. If conflicts do pop up, understanding the basics of Probate Litigation becomes absolutely essential.

A Practical Checklist for Claiming Non-Probatable Assets

When you’re named as a beneficiary for a non-probatable asset, the process of claiming it is a direct line between you and the financial institution. This setup is designed to sidestep court supervision entirely, making it a much faster and more private way to honor a loved one’s final wishes. Still, knowing where to start can feel overwhelming when you’re also navigating grief.

This straightforward, step-by-step guide is designed to cut through the confusion and give you a clear path forward. It breaks the process down into simple, manageable actions, helping you secure your loved one’s assets efficiently and with confidence.

Step 1: Gather Your Essential Documents

Before you make any calls, your first step is to get all the necessary paperwork in order. Being prepared from the start will make every other step feel much smoother and far less stressful.

You will almost always need these three items:

- A certified copy of the death certificate. Most institutions will not accept a photocopy; they need an official, sealed copy. It’s a good idea to order several certified copies from the Texas Bureau of Vital Statistics, as each company will likely require its own original.

- Your government-issued photo ID. This is to verify that you are the person named as the beneficiary.

- Account or policy information. Gather any statements, policy documents, or letters you can find that include the relevant account or policy numbers.

Having these items ready shows the institution you’re organized and helps them process your claim without unnecessary roadblocks.

Step 2: Initiate Contact and Submit the Claim Forms

With your documents in hand, the next step is to reach out to each company holding a non-probatable asset—whether it’s a life insurance company, a bank, or a retirement plan administrator. Let them know the account holder has passed away and that you are the named beneficiary ready to start the claims process.

The institution will then send you their specific claim forms and a list of any other documents they need. Fill these forms out carefully and completely. Double-check details like social security numbers and addresses to avoid simple errors that can cause frustrating delays. Once completed, submit the forms along with the certified death certificate and anything else they requested.

This process is a core part of administering an estate. For assets that do need to go through the court system, our firm has put together a comprehensive guide to the Texas Probate Process that can walk you through every stage.

Key Insight When Beneficiary Designations Go Wrong

Setting up non-probatable assets is a powerful way to protect your family from the costs and delays of court. But these tools are only as good as the paperwork behind them. When beneficiary designations are outdated or flawed, the very assets you intended to keep out of court can get pulled right back into a complicated legal mess.

An outdated form can unintentionally disinherit a loved one or send a significant asset to the wrong person, completely defeating the purpose of your careful planning.

Common Pitfalls That Force Assets into Probate

We have seen simple oversights invalidate a beneficiary designation, forcing an asset that should have been simple to transfer straight into the probate system. Each of these situations creates emotional and financial distress for the family left behind.

- The Beneficiary Has Predeceased: If you named your spouse as your sole beneficiary and they pass away before you, that designation becomes void. Without a contingent (backup) beneficiary named, the asset has nowhere to go. Legally, it defaults back to your estate and must go through probate.

- A Minor is Named as Beneficiary: While you can name a minor, financial institutions cannot legally hand over large sums of money directly to a child. This often forces the family into court to establish a formal, court-supervised Guardianship, which can be a lengthy and expensive process.

- An Ex-Spouse Was Never Removed: This is a tragically common mistake. If you named your spouse on a 401(k) or life insurance policy and later divorced but forgot to update the form, that ex-spouse is still the legal beneficiary. Under the terms of the contract, they will receive the asset—regardless of what your will says.

A Cautionary Example: Consider a life insurance policy where an ex-spouse is still named as the primary beneficiary. Even if a will, written years after the divorce, leaves everything to the children, the insurance company is legally bound by the beneficiary form. You can explore how life insurance proceeds and probate intersect in Texas to understand these powerful contractual obligations better.

These cautionary tales are exactly why working with an experienced attorney is so critical. Proper estate planning involves more than just drafting documents; it includes regularly reviewing and updating all your non-probatable asset designations to ensure they still align with your life and your wishes. This simple diligence is what prevents these devastating problems from blindsiding your family.

When to Call a Texas Probate Attorney for Help

While most non-probatable assets are designed to transfer smoothly, life doesn’t always follow the script. Certain red flags should immediately tell you it’s time to bring in a legal professional. Trying to navigate these situations on your own can be a risk, but an experienced attorney can provide clarity and protect your rights.

It’s smart to pick up the phone and call a probate lawyer if you run into any of these common roadblocks:

- Disputes Between Beneficiaries: If siblings, step-parents, or other relatives start arguing over who is entitled to an asset, you need legal help fast. An attorney can step in to interpret the documents and prevent a disagreement from exploding into expensive and emotionally draining Probate Litigation.

- Unclear or Outdated Designations: You discover an ex-spouse is still listed on a life insurance policy or find a beneficiary form that’s so vague it’s impossible to interpret. These issues require careful legal navigation to resolve correctly.

- Uncooperative Institutions: Is a bank giving you the runaround? Is an insurance company creating unnecessary delays or outright refusing to release the funds? An attorney can cut through the red tape and advocate forcefully on your behalf.

- Complex or High-Value Estates: When you’re dealing with significant wealth, the stakes are higher. A lawyer provides more than just guidance; they offer crucial strategies for high net worth estate planning to protect assets from taxes, creditors, and legal challenges.

If you feel uncertain or overwhelmed, that’s your cue to reach out. A single consultation can provide the clarity and confidence you need to manage the estate correctly and honor your duties as an executor or heir.

Key Insight: The Takeaway

The core principle behind non-probatable assets is proactive planning. By using tools like beneficiary designations, joint ownership, and trusts, you create a direct and legally binding path for your assets to reach your loved ones. This not only bypasses the time and expense of the Texas probate process but also provides your family with much-needed certainty and peace of mind during a time of loss. Regularly reviewing these designations is just as important as creating them, as it ensures your plan remains aligned with your wishes throughout your life.

Frequently Asked Questions About Texas Non-Probatable Assets

Even with a solid plan, it’s natural to have questions about how non-probatable assets really work in Texas. Below are straightforward answers to the questions we hear most often from families trying to navigate this process with care and confidence.

Can a Will Override a Beneficiary Designation?

No, it cannot. This is one of the most important concepts in estate planning. A beneficiary designation on an account like a 401(k) or a life insurance policy is treated as a direct legal contract.

Under the Texas Estates Code (Title 2, Subtitle C), this contract takes priority over anything written in a will. The financial institution is legally bound to pay the money to the person named as the beneficiary, no matter what the will says. It is a separate, binding instruction that probate court does not oversee.

Do Non-Probatable Assets Help Avoid Estate Taxes?

This is a common point of confusion. While non-probatable assets are excellent for avoiding the probate process, they do not automatically sidestep estate taxes.

The value of these assets is still included when calculating the total value of the decedent’s estate for federal estate tax purposes. However, the good news is that the federal estate tax exemption is very high (over $13 million per person in 2024), so the vast majority of Texas estates do not owe any federal estate tax.

How Long Does It Take to Receive the Funds?

The timeline can differ between institutions, but it is almost always dramatically faster than probate.

Once you submit the required claim forms and a certified copy of the death certificate, receiving the payout from a POD account or a life insurance policy often takes just a few weeks. This provides families with access to needed funds far sooner than the months—or even years—the formal Texas probate process can take.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.