When you start thinking about estate planning, the process can feel overwhelming. Your primary goal is simple: to protect your family’s future. For many Texans, a last will and testament seems like the most straightforward option. However, a trust offers a more robust—and private—way to manage your legacy, providing peace of mind during a difficult time.

Unlike a will, which becomes a public court record during the probate process, creating a trust ensures your family's financial affairs remain completely private.

Why Creating a Trust is a Smart Move for Texas Families

The probate process, governed by the Texas Estates Code, can be lengthy and public, often taking months or even years. During that time, the details of your estate become accessible to anyone. This privacy concern is a significant reason many families choose to create a trust. With a trust, the transfer of your assets happens outside of court supervision, offering a seamless and quiet transition for your grieving loved ones.

In plain English, a trust is a legal arrangement where you (the Grantor) transfer assets to a manager (the Trustee) to hold for the people you love (the Beneficiaries). But it's so much more than a legal definition. It's a tool that provides unmatched control over your legacy, ensuring your wishes are carried out with precision and care.

The Core Benefits for Your Family

A trust provides several key advantages that a will simply can't match. These benefits all center on control, efficiency, and protection for the people you care about most.

- Avoiding Probate: Assets held in a trust pass directly to your beneficiaries without going through the court system. This saves considerable time, money, and stress for your family. The Texas Probate Process can be complex, and a trust helps bypass it entirely.

- Maintaining Control: You can set specific conditions for how and when your beneficiaries receive their inheritance. This is ideal for protecting assets for young children, managing funds for a loved one with special needs, or safeguarding an inheritance from creditors.

- Ensuring Privacy: Your estate's value and distribution details remain a private family matter, shielded from public record and prying eyes.

Let's look at a realistic scenario. Imagine a Dallas family with two young adult children. By placing their home and investments into a revocable living trust, the parents ensure that if something happens to them, their kids won't have to endure a drawn-out, public probate battle. Instead, the person they named as the successor trustee can step in immediately to manage and distribute the assets according to their exact instructions. There is no waiting for court approval, no public filings—just a smooth transition guided by their parents' wishes.

Will vs. Living Trust At A Glance For Texans

To see just how different these two tools are, a side-by-side comparison can be really helpful.

| Feature | Last Will and Testament | Revocable Living Trust |

|---|---|---|

| Probate | Required. Goes through the Texas court system as outlined in the Texas Estates Code. | Avoids probate. Assets transfer privately. |

| Privacy | Becomes a public record once filed in court. | Remains private. Details are not public. |

| Control | Distributes assets outright upon your death. | You can set ongoing conditions for distributions. |

| Cost | Lower upfront cost, but probate can be expensive. | Higher upfront cost, but avoids probate expenses. |

| Incapacity | Does not manage assets if you become incapacitated. Requires a separate Guardianship proceeding. | A successor trustee can manage assets for you. |

| Asset Transfer | Takes effect only after your death. | You must transfer (fund) assets into it while alive. |

This table makes it clear that while a will is a fundamental part of any plan, a living trust offers a level of control and privacy that a will can't provide on its own.

Understanding why you should set up a trust is the first step toward securing your family’s financial future and providing them with a clear, compassionate path forward during what will already be a difficult time.

Choosing The Right Type Of Trust In Texas

Once you've decided a trust is the right move for your family, the next big question is: which kind? This isn't about getting lost in dense legal jargon; it's about matching the tool to the job. Think of it like building a house—you have to get the foundation right before you start picking out paint colors.

In Texas, trusts boil down to two fundamental categories: revocable and irrevocable. The difference hangs on one simple question: can you change your mind later?

The Flexible Foundation: Revocable Living Trusts

For most Texas families, the revocable living trust is the go-to choice. It's flexible. While you're alive and have your wits about you, you can change it, add property, remove property, or even scrap the whole thing. You are in complete control.

I like to think of it as a toolbox. With a revocable trust, you can open that toolbox whenever you want, swap out tools, add new ones, or take something out to use. It’s your toolbox, and you have full access. This adaptability is exactly why so many people start here—it's designed to evolve with your life's changes, like a new marriage, the birth of a grandchild, or a major shift in your assets.

Revocable living trusts have become a cornerstone of modern estate planning for a reason. In fact, 52% of millionaires use them to sidestep the probate process, which can eat up 3-7% of an estate's value and drag on for up to two years in messy disputes. The demand for these services is clear, with the global trust market projected to hit $11,830 million by 2025, showing just how valuable they are for wealth preservation worldwide. You can learn more about the growth of trust services and their impact on families.

The Permanent Fortress: Irrevocable Trusts

An irrevocable trust, on the other hand, is a different animal entirely. Once you create it and move assets into it, it’s generally set in stone. You typically can't make changes without getting the beneficiaries to agree. It’s like putting your valuables in a high-security vault and handing the key to someone else. Once that door is locked, you can't just walk in and take things out.

So why would anyone choose something so rigid? Because an irrevocable trust offers powerful benefits that a revocable one simply can't, especially when it comes to asset protection and tax planning.

- Creditor Protection: Since you no longer legally "own" the assets inside the trust, they are generally shielded from your personal creditors or lawsuits.

- Estate Tax Reduction: By moving assets out of your name, you can shrink the size of your taxable estate.

- Medicaid Planning: This can be an indispensable tool for long-term care planning, helping to preserve your life's savings while qualifying for government benefits.

For Texas families, this choice is a big one. A revocable trust gives you control, but an irrevocable trust provides a level of protection that can be absolutely critical for high-net-worth individuals or anyone worried about future long-term care costs.

Specialized Trusts For Unique Family Needs

Beyond these two broad categories, Texas law allows for all sorts of specialized trusts built to handle specific family situations. These are tailored solutions designed for life's unique challenges, offering peace of mind where it matters most.

- Special Needs Trusts (SNTs): If you have a child or loved one with a disability who relies on government benefits like Medicaid or SSI, an SNT is non-negotiable. It lets you set aside funds for their care and quality of life without kicking them off these critical programs.

- Spendthrift Trusts: This trust is perfect for protecting a beneficiary's inheritance from their own poor judgment or from creditors. The trustee you appoint manages the money and makes distributions according to your rules, ensuring the funds are used wisely and don't disappear overnight.

- Charitable Trusts: For those passionate about giving back, a charitable trust lets you support a cause you love while also getting some potential tax perks. You can structure it to benefit a charity right away or after you and your other beneficiaries are gone.

Each of these specialized tools provides a way to care for your loved ones with precision and foresight. By exploring the different types of trusts available in Texas, you can find the perfect fit to protect your family’s unique legacy.

Defining The Key Roles In Your Texas Trust

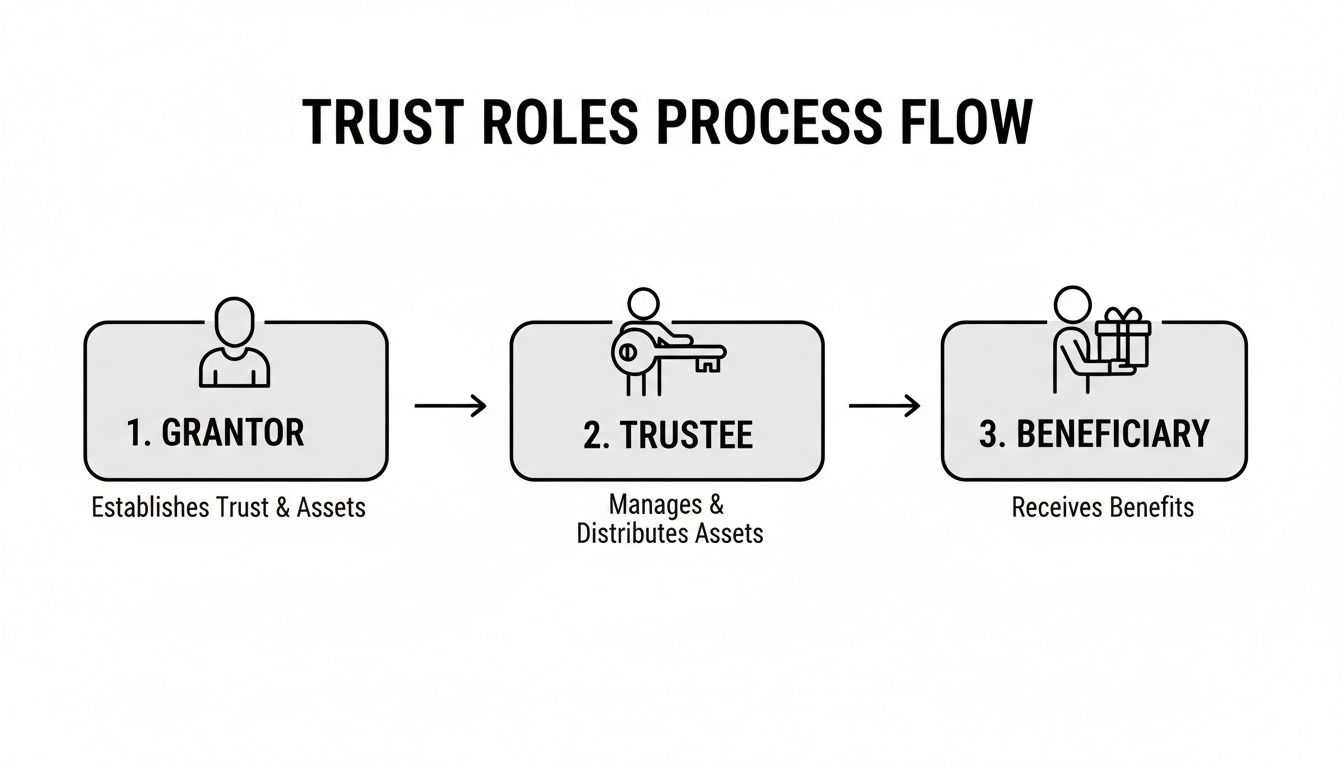

Once you’ve settled on the right type of trust for your family, it’s time to bring it to life by assigning the key players. Think of it like casting a play—each role is absolutely essential for the story to unfold exactly as you’ve written it. In the world of Texas trusts, there are three non-negotiable roles to fill: the Grantor, the Trustee, and the Beneficiary. Making these calls requires some serious, heartfelt consideration, because these are the people you’ll be entrusting to carry out your most important wishes.

The Grantor: The Visionary

This is the easiest role to define because, in almost every case, it’s you.

The Grantor (you might also hear the terms Settlor or Trustor) is the person who creates the trust and puts their property into it. If you're setting up a revocable living trust, you’ll actually wear all three hats at the beginning: you create it (Grantor), you manage it (initial Trustee), and you benefit from it during your life (initial Beneficiary). This setup is designed to give you complete control over your assets while you are alive and well.

Your job as the Grantor is to be the architect of your legacy. You decide what property goes into the trust, who gets to benefit from it, and under what specific conditions. This is where you can get incredibly detailed, ensuring your assets are used in a way that truly reflects your values and protects the people you love.

The Trustee: The Manager

The Trustee is the person or institution you pick to manage the trust's assets according to the rulebook you’ve created. This is, without a doubt, one of the most critical decisions you will make.

The Trustee has a fiduciary duty—a legal obligation of the highest order—to act only in the best interests of the beneficiaries. This isn’t a small favor you’re asking; it's a massive responsibility that demands integrity, good financial sense, and a rock-solid commitment to following your directions to the letter.

While you're alive, you'll probably serve as your own trustee. The really tough decision is naming a successor trustee—the person who steps in to manage things when you can no longer do so, either due to incapacity or after your passing. You have two main routes to go here, each with its own pros and cons.

| Trustee Type | Pros | Cons |

|---|---|---|

| Family Member or Friend | Knows your family dynamics and what you would have wanted. Usually doesn't charge a fee. | Might not have the financial savvy, could be pressured by other family members, or find the job just plain overwhelming. |

| Corporate Trustee (Bank or Trust Company) | Brings professional, impartial management. They're experts in investments, taxes, and legal compliance. | They charge fees for their services and won't have that personal connection to your family. |

For many families in Texas, a trusted adult child or a close sibling feels like a natural fit. But if your estate is complicated, involves a family business, or if you anticipate family conflict, a professional corporate trustee can be the neutral, experienced hand that keeps everything fair and prevents disputes that could lead to Probate Litigation.

The Beneficiaries: The Heirs

The Beneficiaries are the people, charities, or even beloved pets that the trust was created for. They are the ones who will ultimately receive the assets or income from the trust. You can name primary beneficiaries, who inherit first, and also contingent beneficiaries, who would step in if the primary ones are no longer living.

This is where a trust really shows its power. You can be as specific as you want with your instructions for how and when money is handed out.

Let’s look at a common scenario. Imagine a Houston couple creating a trust for their two children. One child is a responsible saver, but the other has always struggled with money.

- For their financially savvy child, they might direct the trustee to distribute their entire share in a lump sum when they turn 30.

- For the other child, they could add a spendthrift provision. This tells the trustee to hand out a set amount each month and pay for major expenses like rent or medical bills directly. This protects the inheritance from being spent too quickly or being taken by creditors.

These are the kinds of detailed instructions, spelled out in your trust document, that provide real peace of mind. You know your legacy will be a blessing, not a burden, to the people you care about most. If you're thinking about setting one up, understanding the nuances of Wills & Trusts is the perfect place to start.

Funding And Finalizing Your Texas Trust

You’ve drafted the trust document, and that’s a massive step. But let’s be clear: a trust without any assets is like an empty vault. It looks official, but it protects nothing. Now comes the most crucial part of the process: funding the trust.

Funding is simply the process of transferring the ownership of your assets into the name of your trust. This is the moment your paperwork transforms from a stack of paper into a powerful legal tool that actually works.

Frankly, this is where most DIY estate plans fall flat. It's not enough to just list your home or your bank account in the trust document. You have to legally change the titles and ownership records to show the trust—not you, the individual—is the new owner. If you miss this step, the trust is effectively useless, and your assets will get dragged right back into the probate court you were trying so hard to avoid.

Retitling Your Assets The Right Way

Funding your trust involves some administrative legwork, but it's a methodical process. Every type of asset has its own specific procedure for being moved into the trust's name.

Here’s a step-by-step guide for common assets we see Texas families move into their trusts:

- Your Home and Other Real Estate: This is often the most valuable asset you'll fund. To do it right, you need to sign a new deed transferring the property from your individual name to yourself as the trustee of your trust. If you need a deeper dive on this, our firm has a guide on how to change a deed on a house in Texas.

- Bank Accounts: For your checking, savings, and money market accounts, you'll need to work directly with your bank. The goal is to change the account ownership from your personal name to the name of the trust. This usually means filling out new signature cards and giving the bank a copy of your Certificate of Trust.

- Non-Retirement Investment Accounts: Just like with your bank accounts, you’ll need to contact your brokerage firm. They have a process for retitling your taxable investment accounts into the name of the trust.

- Business Interests: If you own an LLC, a partnership, or a small business, you can assign your ownership interest to the trust. This requires specific legal documents to ensure the transition is clean and legally sound.

This flowchart gives you a simple visual of the key players you've already named in your trust document.

As the visual shows, the Grantor (that's you) gives the Trustee the power to manage assets for your Beneficiaries. The act of funding is what legally connects your assets to this structure, making it all work.

Handling Retirement Accounts And Life Insurance

It's absolutely critical to understand that some assets, like your 401(k)s, IRAs, and life insurance policies, are handled differently. As a general rule, you do not change the ownership of these accounts to your trust.

Instead, you work with the account custodian to update the beneficiary designations. You can often name your trust as the primary or contingent beneficiary. This strategy allows the detailed rules you’ve laid out in your trust to control how those funds are eventually distributed, giving you far more control and protection than a direct payout to an individual ever could.

Making It Legally Binding In Texas

Once the trust is drafted and you have a clear plan for funding it, the last step is making it official. Under the Texas Estates Code (specifically Title 3), a trust document must be signed to be valid.

But there’s one more detail that makes all the difference. While Texas law doesn’t strictly require a trust to be notarized to be legally effective, it is an essential best practice. A notary’s seal proves your identity and confirms you signed the document willingly. This simple step is your best defense against future challenges to the trust's validity.

Think about it this way: imagine a disgruntled relative later claims you weren't of sound mind when you signed the trust. A notarized signature, witnessed by an impartial public official, provides powerful evidence that you executed the document with clear intent. It can shut down potential legal battles before they even start, ensuring your legacy is protected exactly as you envisioned.

Advanced Trust Strategies and Common Pitfalls to Avoid

Once you've grasped the basics, you'll find that trusts can do much more than just sidestep probate. They are powerful tools for protecting your family's financial future, especially when it comes to life’s biggest “what-ifs.” For many Texas seniors, the most pressing concern is the crushing cost of long-term care and how to prepare for it without wiping out a lifetime of savings. This is where a well-crafted trust isn't just helpful—it's essential.

We often help families explore using specific types of irrevocable trusts for Medicaid planning. The idea is to move assets into this trust well before care is needed. Doing so can preserve your home and savings for your heirs while helping you meet the strict financial limits to qualify for Medicaid benefits to cover nursing home costs. It's a proactive move that brings incredible peace of mind.

Understanding the tax implications is just as critical. With a revocable living trust, you keep complete control, so the IRS just sees the trust’s assets as your own. You'll continue to report any income on your personal tax return, no changes there. An irrevocable trust, on the other hand, is its own separate taxable entity and has to file its own tax return. This is a vital distinction for proper planning and avoiding a surprise tax bill down the road.

The Most Common Mistakes We See

In our years of helping Texas families, we've seen firsthand how small oversights can create huge headaches. Even the best intentions can go awry if the execution isn't precise.

Here are some of the most common pitfalls to steer clear of:

- Failing to Fully Fund the Trust: I can't say this enough—it's the number one mistake. An unfunded or partially funded trust leaves your assets exposed to probate, completely defeating one of the main reasons for creating it.

- Choosing the Wrong Trustee: Naming someone who is disorganized, easily swayed by others, or simply not up for the job can lead to mismanagement and family feuds. It adds a layer of stress to an already difficult time.

- Using a Generic Online Template: A one-size-fits-all document from the internet can't possibly account for your unique family dynamics or the specific nuances of the Texas Estates Code. These templates often create more legal problems than they solve.

Trusts have become a cornerstone of modern estate planning, and for good reason. The global trust and foundations market is expected to hit $184.49 billion in 2025. Here in Texas, the motivation is crystal clear: avoid lengthy court battles that can drag on for 12-18 months and eat up 4-7% of an estate's value. A properly structured trust keeps things private and bypasses that process, saving heirs time, money, and heartache—often cutting costs by up to 50%. Our experience shows that personalized trusts prevent the kind of disputes that impact nearly 30% of probated estates. You can learn more about these global trends in trust and estate planning if you're interested in the bigger picture.

Why Professional Guidance Matters

Navigating the complexities of creating and managing a trust isn't something you should tackle alone. An experienced attorney does more than just draft documents; we become your family's guide. We help you think through the tough decisions, like who to name as trustee or how to structure distributions for a beneficiary with special needs.

We also make sure your trust works in harmony with the other critical parts of your estate plan, like your will and powers of attorney. This integrated approach closes legal loopholes and protects against the challenges that can pop up from a poorly coordinated plan. Ultimately, working with a professional is an investment in your family’s future security and peace.

Key Takeaway: Your Trust is a Plan for Peace of Mind

Navigating the world of estate planning can feel like a heavy lift, but it is an act of love. Creating a trust is more than a legal strategy; it's a profound act of care that gives your family a clear roadmap during a difficult time. A trust provides security, privacy, and control, ensuring your legacy is a blessing, not a burden.

It’s a series of deliberate, thoughtful decisions that, when made correctly, provide real security and peace of mind. For many people, getting guidance from professional financial planning services can make all the difference in ensuring every detail is handled correctly.

Your Most Important Takeaways

If you boil it all down, a successful trust really hinges on just a few core principles. Keep these front and center, and you'll stay focused on what truly matters for your family's future.

- A Trust Gives You Unmatched Control and Privacy: Unlike a will, a trust lets your assets bypass the public and often painfully slow probate process. This keeps your family's financial affairs private and gives you the power to set specific rules for your legacy.

- Your Trustee and Trust Type Choices Are Critical: Picking the right kind of trust (like revocable vs. irrevocable) and naming a capable, trustworthy person to manage it are the two most impactful decisions you'll make in this process.

- An Empty Trust Protects Nothing: A trust is only effective once you actually fund it. This is the crucial step of legally transferring your assets—your home, bank accounts, and investments—into the name of the trust. This is what gives the document its power.

Building a trust isn't just about moving assets around. It’s about giving your loved ones clarity and stability when they need it most. Think of it as your final gift to them—a well-designed plan that cuts down on stress and guarantees they're cared for exactly the way you intended.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.

Answering Your Top Questions About Texas Trusts

Diving into the world of trusts can feel a bit overwhelming, and it's natural for questions to pop up. To cut through the confusion, here are some straightforward answers to the most common questions we hear from families across Texas.

Can I Be The Trustee Of My Own Revocable Living Trust?

Yes, absolutely. In fact, this is the standard way it's done. When you set up a revocable living trust, you'll almost always name yourself as the initial trustee. This setup is popular for a simple reason: it lets you keep 100% control over all the assets you place in the trust for as long as you live.

You aren't just naming yourself, though. You'll also appoint a successor trustee. This is the person or institution you trust to step in and manage things for you if you become incapacitated or after you pass away. It's the key to ensuring a smooth, private transition of control without ever having to involve a court.

How Much Does It Cost To Set Up A Trust In Texas?

The cost of creating a trust isn't one-size-fits-all; it really depends on the complexity of your goals and family situation. A simple trust for a straightforward estate is going to be less of an investment than a highly customized one designed for a blended family, a beneficiary with special needs, or sophisticated tax planning.

But here’s the most important way to think about it: this isn't just an expense, it's an investment in your family's future peace of mind. The upfront cost to get a trust done right is almost always a tiny fraction of the legal fees, court costs, and emotional strain that come with the public Texas probate process.

Does A Trust Protect My Assets From A Lawsuit?

This is a fantastic and critical question, and the answer hinges entirely on which type of trust you have.

For a standard revocable living trust, the answer is generally no. Because you maintain control and can pull assets out anytime you wish, the law still sees those assets as yours. Creditors and lawsuits can typically reach them.

If serious asset protection is your goal, you'd need to explore an irrevocable trust. With this tool, you permanently give up control of the assets by transferring them into the trust. This move is what shields them from your future creditors or legal troubles. It’s a powerful strategy, but it requires a lot of careful thought and expert guidance.

Do I Still Need A Will If I Have A Trust?

Yes, you do. A will remains an absolutely essential piece of your estate plan, even with a rock-solid trust in place. The kind of will you'll have is called a "pour-over" will, and it's your trust's best friend.

This special will does two crucial jobs that a trust can't:

- It acts as a safety net. It "catches" any assets you might have forgotten to formally transfer into your trust and "pours" them in after you're gone.

- It is the only legal document where you can name guardians for your minor children. This is a must-do for any parent.

When you pair a trust with a pour-over will, you get a complete, airtight plan that protects both your property and your people. Getting a handle on how Wills & Trusts work together is the cornerstone of a secure estate plan.

If you’re facing probate in Texas, our team can help guide you through every step — from filing to final distribution. Schedule your free consultation today.